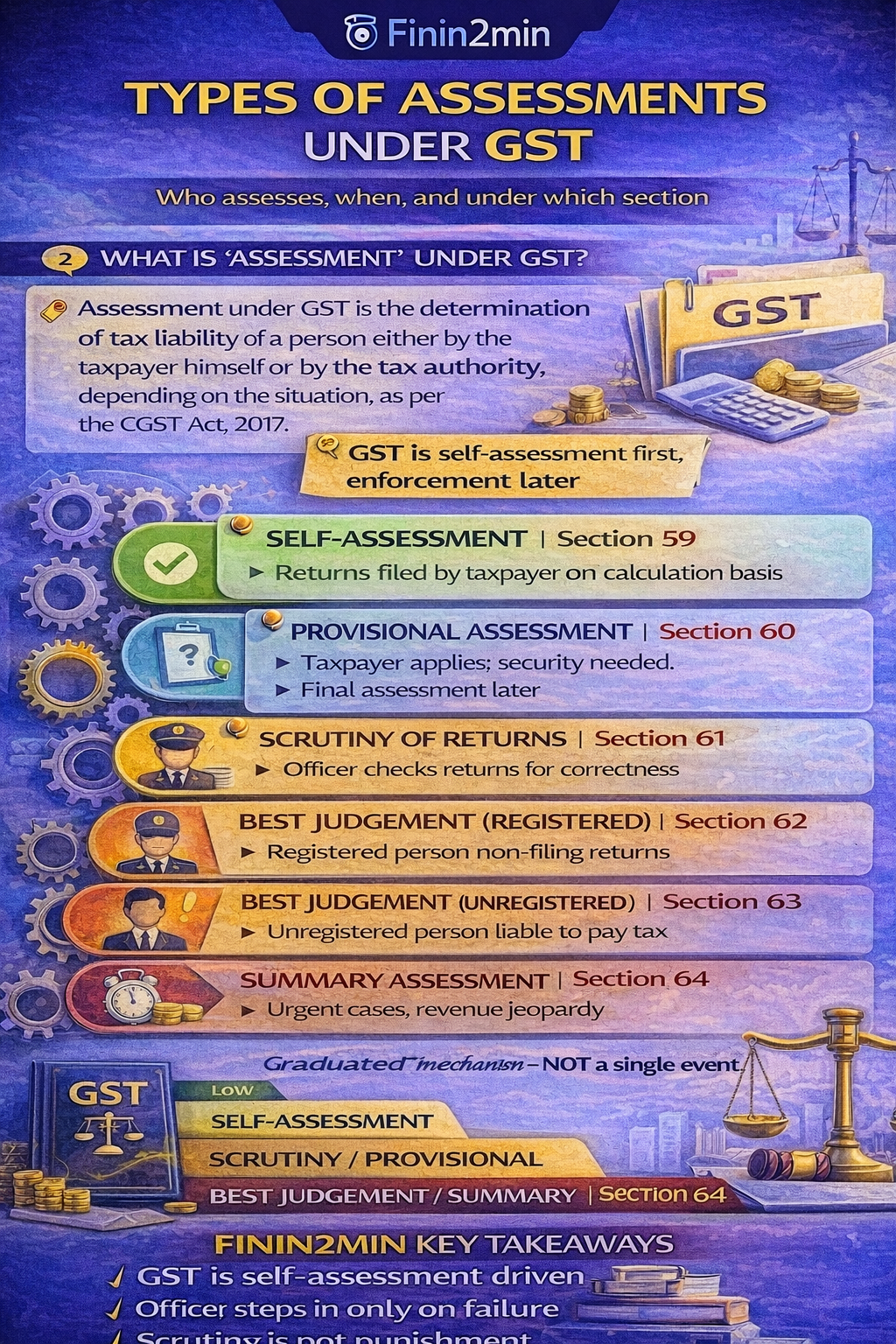

Assessment under GST is the determination of tax liability of a person either by the taxpayer himself or by the tax authority, depending on the situation, as per the CGST Act, 2017.

📌 GST is self-assessment first, enforcement later.

2️⃣ Snapshot: All Types of GST Assessments

Type of Assessment

Section

Who Determines Tax

When It Applies

Self-Assessment

59

Taxpayer

Regular compliance

Provisional Assessment

60

Taxpayer + Officer

Rate/value uncertainty

Scrutiny of Returns

61

Tax Officer

Return mismatches

Best Judgement (Registered)

62

Tax Officer

Non-filing of returns

Best Judgement (Unregistered)

63

Tax Officer

Taxable but unregistered

Summary Assessment

64

Tax Officer (with approval)

Urgent revenue risk

3️⃣ Self-Assessment — Section 59 (Default Rule)

Aspect

Details

Nature

Trust-based

Returns involved

GSTR-1, GSTR-3B, Annual Return

Officer involvement

❌ None

ITC & tax calculation

Done by taxpayer

Illustrative Example

Particulars

Amount (₹)

Taxable outward supply

10,00,000

GST @ 18%

1,80,000

ITC available

1,20,000

Net GST payable

60,000

📌 Most GST liabilities arise here.

4️⃣ Provisional Assessment — Section 60

Trigger

When correct value or tax rate is unclear

Who applies

Taxpayer

Officer’s role

Permits provisional payment

Security required

Bond + security

Outcome

Final assessment later + adjustment

Example

Situation

Action

New product — tax rate unclear (12% or 18%)

Apply for provisional assessment

Provisional tax paid

@12%

Final rate decided

18%

Adjustment

Differential tax + interest

📌 Used sparingly, but very important in classification disputes.

5️⃣ Scrutiny Assessment — Section 61

Purpose

To verify correctness of returns

Initiated by

Proper Officer

Scope

Data mismatch, ITC excess, tax short-paid

Result

Explanation accepted or further proceedings

Common Scrutiny Triggers

Issue

Example

ITC mismatch

GSTR-3B > GSTR-2B

Turnover mismatch

GSTR-1 vs GSTR-3B

Rate mismatch

Wrong HSN rate

📌 Scrutiny ≠ demand. It is a pre-enforcement check.

6️⃣ Best Judgement Assessment — Sections 62 & 63

A. Section 62 — Registered Person

Applies to

Registered taxpayer

Default

Non-filing of returns

Basis

Past returns, available data

Objective

Enforce compliance

Example: Returns not filed for 6 months → Officer estimates tax → Assessment order issued.

B. Section 63 — Unregistered Person

Applies to

Liable but unregistered person

Basis

Market data, inspections, records

Consequence

Tax + penalty exposure

Example: Business crosses threshold but no GST registration → Officer assesses tax.

GST assessment is a graduated mechanism — not a single event. If returns are accurate and reconciled, most taxpayers never face officer-driven assessment.

This content is for general information and educational purposes only. It does not constitute legal, tax, accounting, or professional advice. Views expressed are based on prevailing laws and interpretations at the time of publication. Readers should consult their professional advisors before taking any action.

Article related to –

types of assessment under GST self assessment provisional scrutiny GST best judgement assessment GST summary assessment section 64 GST GST assessment sections explained GST audit vs assessment