Madras HC flags non-consideration of CBIC circulars; remands demand for fresh review

🔎 The Big Picture (Finin2min Take)

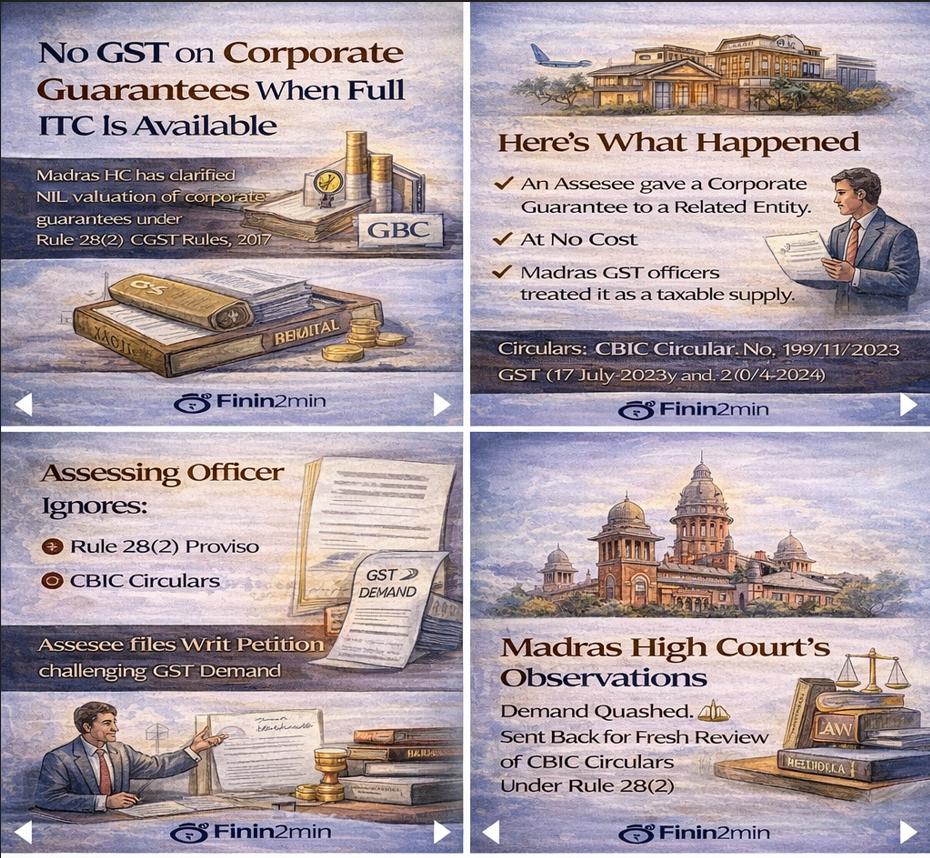

The Madras High Court has delivered an important procedural and valuation reminder for GST authorities:

👉 Where a corporate guarantee is given without consideration and the recipient is eligible for full ITC, the value can be treated as NIL—if CBIC circulars and Rule 28(2) are properly applied.

The ruling does not grant automatic exemption, but it quashes a mechanical demand raised without examining binding CBIC clarifications.

📌 Case Snapshot

Case: Amman Try Trading Company Pvt. Ltd. v. State Tax Officer – V (Roving Squad)

Court: Madras High Court

W.P. No.: 20109 of 2025

Order Date: 6 October 2025

🧾 Facts in Brief

- The taxpayer furnished a corporate guarantee to a related entity.

- No consideration was charged.

- The recipient entity was eligible for full Input Tax Credit (ITC).

- The GST department raised a demand by valuing the guarantee at 1% of the guaranteed amount, treating it as a taxable supply.

⚖️ Core Legal Issue

Can GST be demanded on a corporate guarantee given without consideration, when CBIC circulars clarify that the value can be NIL if the recipient has full ITC?

🧑💼 Taxpayer’s Argument

The petitioner relied on binding CBIC circulars, arguing that:

- Circular No. 199/11/2023-GST (17 July 2023) and

- Circular No. 210/4/2024-GST (26 June 2024)

clarify valuation under Rule 28(2), CGST Rules.

Key contention:

- When a corporate guarantee is provided without consideration, and

- The recipient is eligible for full ITC,

- The value declared in the invoice (even NIL) is deemed to be the open market value.

🧾 Department’s Stand

- GST was demanded at 1% of the guarantee value, relying on Rule 28(2).

- The adjudication order did not deal with or analyse the taxpayer’s reliance on the CBIC circulars.

🏛️ Madras High Court’s Key Observations

1️⃣ CBIC Circulars Are Binding

The Court reiterated that departmental officers are bound by CBIC circulars and must consider them while passing orders.

2️⃣ Failure to Consider Submissions = Procedural Lapse

The impugned order was held vulnerable because:

- Detailed submissions citing CBIC circulars were made, and

- The order failed to examine or address them.

This violated settled principles of administrative law and natural justice.

3️⃣ Rule 28(2) Must Be Read With Its Proviso

The Court highlighted that:

- Rule 28(2) prescribes 1% valuation or actual consideration, whichever is higher, BUT

- The proviso clearly states that where the recipient is eligible for full ITC,

👉 the value declared in the invoice shall be deemed to be the value of supply.

✅ Outcome

- The GST demand order dated 28 April 2025 was quashed.

- The matter was remanded back to the Assessing Officer.

- The authority must reconsider the taxpayer’s submissions and pass a fresh, reasoned order on merits.

⚠️ Importantly, the Court did not itself finally decide taxability, but removed an unsustainable demand passed without due consideration.

📊 What This Judgment Really Means (Finin2min Clarity)

| Aspect | Position |

|---|---|

| Corporate guarantee | Treated as a supply between related parties |

| Default valuation | 1% of guarantee amount |

| Key relief trigger | Recipient eligible for full ITC |

| Effect of CBIC circulars | Invoice value (even NIL) deemed as OMV |

| HC ruling | Demand quashed for non-consideration, matter remanded |

🧠 Practical Takeaways for Businesses

- Corporate guarantees are not automatically GST-free.

- Relief depends on valuation, not existence of supply.

- Full ITC eligibility of recipient is critical.

- Proper documentation and reliance on CBIC circulars is essential.

- Mechanical demands ignoring circulars are legally vulnerable.

🧾 Relevant Legal Provision (Quick Reference)

Rule 28(2), CGST Rules, 2017

Value of corporate guarantee = 1% of guarantee amount or actual consideration, whichever is higher.

Proviso: If the recipient is eligible for full ITC, the invoice value is deemed to be the value of supply.

🔍 Finin2min Bottom Line

This ruling is less about “no GST” and more about “no blind GST”.

Tax officers must apply Rule 28(2) along with CBIC circulars, not in isolation.

For corporate guarantees with full ITC on the other side, valuation—not intention—decides tax exposure.

Disclaimer:

This content is for general information and educational purposes only. It does not constitute legal, tax, accounting, or professional advice. Views expressed are based on prevailing laws and interpretations at the time of publication. Readers should consult their professional advisors before taking any action.

Article related to –

GST on corporate guarantee

Corporate guarantee GST valuation

Rule 28(2) GST explained

Corporate guarantee without consideration GST

GST corporate guarantee full ITC

Nil value corporate guarantee GST

GST valuation between related persons

Corporate guarantee GST circular

Amman Try Trading Company GST case

Madras High Court GST corporate guarantee

GST demand on corporate guarantee quashed

CBIC Circular 199/11/2023 GST

CBIC Circular 210/4/2024 GST

Corporate guarantee GST High Court ruling

GST litigation updates India

GST valuation disputes

GST compliance for group companies

Related party transactions under GST

GST audit risk corporate guarantees

Is GST payable on corporate guarantee without consideration?

When is corporate guarantee taxable under GST?

Full ITC corporate guarantee GST treatment

Rule 28(2) proviso explained with example

Corporate guarantee GST demand legality