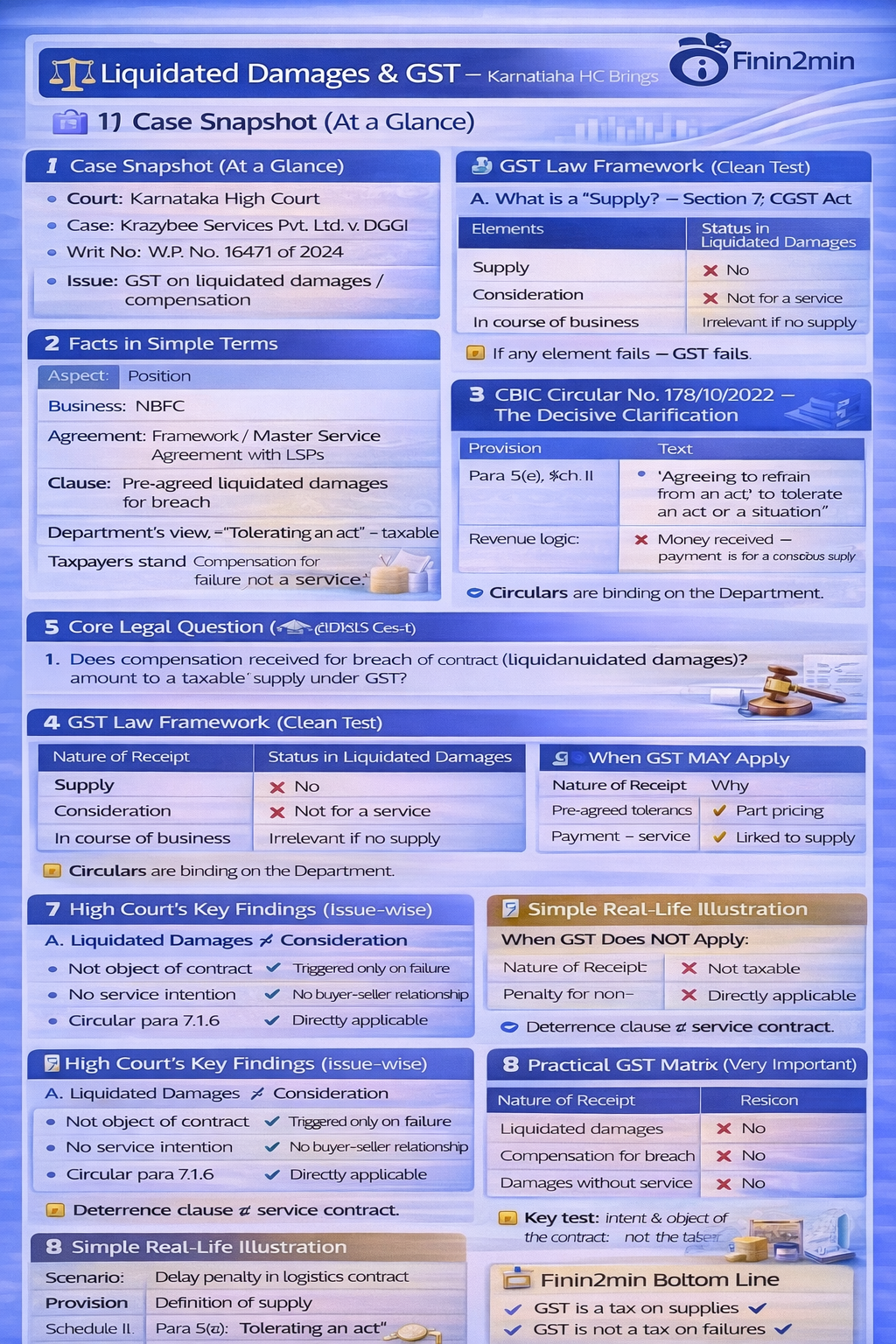

Does compensation received for breach of contract (liquidated damages) amount to a taxable “supply” under GST?

4️⃣ GST Law Framework (Clean Test)

A. What Is a “Supply”? — Section 7, CGST Act

Mandatory Elements

Status in Liquidated Damages

Supply

❌ No

Consideration

❌ Not for a service

In course of business

Irrelevant if no supply

📌 If any element fails → GST fails.

B. Department’s Usual Argument — Schedule II, Para 5(e)

Provision

Text

Para 5(e), Sch. II

“Agreeing to refrain from an act, or to tolerate an act or a situation”

Revenue logic: Money received → tolerance → taxable service.

Court’s answer: ❌ Incorrect when payment arises due to breach.

5️⃣ CBIC Circular No. 178/10/2022 — The Decisive Clarification

Circular Para

What It Clarifies

7.1 – 7.1.6

Distinguishes object of contract vs consequence of failure

Key principle

GST applies only if payment is for a conscious supply

Liquidated damages

Compensation, not consideration

📌 Circulars are binding on the Department.

6️⃣ Contract Law Backbone (Why LD Is Compensation)

Provision

Relevance

Section 73, Contract Act

Compensation for loss due to breach

Section 74, Contract Act

Pre-agreed damages (liquidated damages)

Nature

Restorative, not remunerative

📌 LD aims to make good the loss, not to reward tolerance.

7️⃣ High Court’s Key Findings (Issue-wise)

A. Liquidated Damages ≠ Consideration

Observation

Reason

Not object of contract

Triggered only on failure

No service intention

No buyer–seller relationship

Circular para 7.1.6

Directly applicable

B. No “Tolerating an Act” Arrangement

Department’s Claim

Court’s Rejection

Pre-agreed tolerance

Clause deters breach

Payment = service

Payment = failure consequence

📌 Deterrence clause ≠ service contract.

C. Circular Binding on Officers

Principle

Impact

CBIC clarification issued

Must be followed

Selective reliance

Not permissible

8️⃣ Practical GST Matrix (Very Important)

When GST Does NOT Apply

Nature of Receipt

GST

Liquidated damages

❌

Compensation for breach

❌

Penalty for non-performance

❌

Damages without service

❌

When GST MAY Apply

Nature of Receipt

Why

Early termination fee

Part of pricing

Cancellation charges

Linked to supply

Late payment charges

Facility consciously provided

📌 Key test: intent & object of the contract — not the label.

9️⃣ Simple Real-Life Illustration

Scenario

GST Result

Delay penalty in logistics contract

❌ Not taxable

Was delay “hired” as a service?

❌ No

Was contract meant to fail?

❌ No

👉 Failure ≠ Supply

🔟 Statutory Provisions Referenced

Provision

Why It Matters

Section 7, CGST Act

Definition of supply

Schedule II, Para 5(e)

“Tolerating an act”

Sections 73–74, Contract Act

Legal basis of LD

Rule 142, CGST Rules

Voluntary payment procedure

CBIC Circular 178/10/2022

Taxability clarification

🔚 Finin2min Bottom Line

Principle

Final Take

GST is a tax on supplies

✔

GST is not a tax on failures

✔

Compensation ≠ consideration

✔

Intent matters more than wording

✔

Final Finin2min Verdict

Liquidated damages are compensatory, not taxable. Unless money is paid for a conscious supply, GST has no role to play. GST taxes performance — not breach.

⚠️ Disclaimer

For information only. This summary is based on prevailing statutory provisions and judicial precedents. Applicability depends on facts, timing, and documentation. Professional advice recommended.

Article related to – GST on compensation Is liquidated damages taxable under GST Schedule II Para 5(e) GST Tolerating an act GST CBIC Circular 178/10/2022 explained GST on breach of contract