Why insurance reforms must move slower than telecom — and why that’s intentional

“Sabka Bima Sabki Raksha (Amendment of Insurance Laws) Bill, 2025”

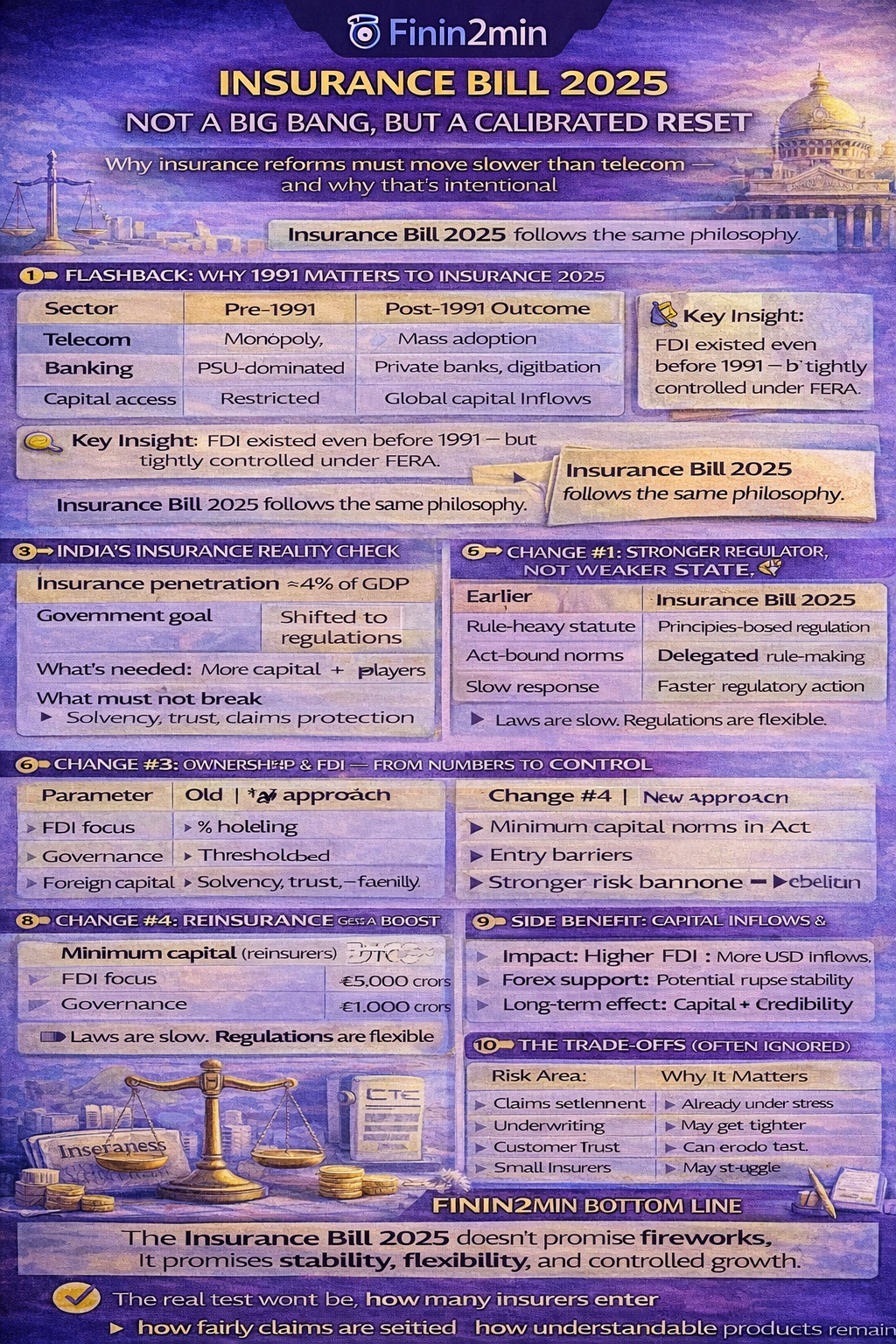

1️⃣ Flashback: Why 1991 Matters to Insurance 2025

What Liberalisation Actually Did

| Sector | Pre-1991 | Post-1991 Outcome |

|---|---|---|

| Telecom | Monopoly, luxury | Mass adoption, price collapse |

| Banking | PSU-dominated | Private banks, digitisation |

| Capital access | Restricted | Global capital inflows |

📌 Key Insight:

FDI existed even before 1991 — but tightly controlled under FERA.

1991 didn’t invent FDI; it standardised & liberalised it.

➡️ Insurance Bill 2025 follows the same philosophy.

2️⃣ Why Insurance Is Different (And Must Be Treated Differently)

| Sector Failure | Consequence |

|---|---|

| Telecom company fails | Customers port numbers |

| Bank fails | Depositors protected |

| Insurance company fails | Policyholders stranded |

📌 Policyholders may have paid premiums for 20–30 years.

Letting insurers fail freely is not politically or socially viable.

➡️ Hence: slow, risk-aware reforms

3️⃣ India’s Insurance Reality Check

| Metric | Status |

|---|---|

| Insurance penetration | ~4% of GDP |

| Government goal | Insurance for all by 2047 |

| What’s needed | More capital + more players + flexibility |

| What must not break | Solvency, trust, claims protection |

4️⃣ Insurance Bill 2025 — The Big Picture

This is not deregulation.

This is re-regulation — smarter, faster, principles-based.

5️⃣ Change #1: Stronger Regulator, Not Weaker State

IRDAI’s Role Is Reinforced

| Earlier Framework | Insurance Bill 2025 |

|---|---|

| Rule-heavy statute | Principles-based regulation |

| Act-bound norms | Delegated rule-making |

| Slow response | Faster regulatory action |

📌 The regulator moves from referee to risk-manager.

6️⃣ Change #2: Government Steps Back from Micro-Management

| Earlier | Now |

|---|---|

| Ownership, capital norms in Act | Shifted to regulations |

| Legislative amendments needed | IRDAI can adapt norms |

| Rigid structure | Market-responsive framework |

📌 Laws are slow. Regulations are flexible.

7️⃣ Change #3: Ownership & FDI — From Numbers to Control

What Actually Changes

| Aspect | Old Approach | New Approach |

|---|---|---|

| FDI focus | % holding | Effective control |

| Governance | Threshold-based | Board & solvency driven |

| Foreign capital | Allowed but constrained | Welcomed with safeguards |

📌 Explains why Bajaj–Allianz JV broke up despite 74% FDI being allowed earlier.

8️⃣ Change #4: Reinsurance Gets a Boost

Why Reinsurance Matters

More insurers → more risk → more reinsurance needed

| Parameter | Earlier | Proposed |

|---|---|---|

| Minimum capital (reinsurers) | ₹5,000 crore | ₹1,000 crore |

| Entry barriers | High | Lowered |

| Industry impact | Limited depth | Stronger risk backbone |

📌 Insurance without reinsurance = fragile system

9️⃣ Side Benefit: Capital Inflows & Currency Stability

| Impact | Explanation |

|---|---|

| Higher FDI | More USD inflows |

| Forex support | Potential rupee stability |

| Long-term effect | Capital + credibility |

📌 Not guaranteed, but directionally positive.

🔟 The Trade-Offs (Often Ignored)

Competition ≠ Consumer Happiness (Always)

| Risk Area | Why It Matters |

|---|---|

| Claims settlement | Already under stress |

| Underwriting | May get tighter |

| Customer trust | Can erode fast |

| Small insurers | May struggle |

📌 Capital cannot fix trust deficits.

11️⃣ Market Structure: Growth vs Consolidation

| Likely Winners | Likely Pressure |

|---|---|

| Large insurers | Regional / niche players |

| Global players | Domestic firms without scale |

| Tech-driven insurers | Commission-driven models |

📌 Market may grow — but also consolidate faster.

12️⃣ What the Bill Is Actually Trying to Balance

| Objective | Guardrail |

|---|---|

| Expand insurance coverage | Protect policyholders |

| Attract foreign capital | Maintain solvency |

| Increase competition | Avoid reckless risk-taking |

| Faster innovation | Regulatory supervision |

➡️ Open doors — but don’t remove seatbelts

13️⃣ Important Legal & Policy Anchors

| Provision / Authority | Why It Matters |

|---|---|

| Insurance Act (amended) | Structural reset |

| IRDAI powers | Principles-based oversight |

| Solvency norms | Policyholder protection |

| FDI policy | Capital + control balance |

🔚 Finin2min Bottom Line

| Myth | Reality |

|---|---|

| “100% FDI = instant boom” | ❌ |

| “This is deregulation” | ❌ |

| “Regulator weakened” | ❌ |

| “Policyholder risk ignored” | ❌ |

✅ This is a calibrated reset, not a gamble

Final Finin2min Verdict

The Insurance Bill 2025 doesn’t promise fireworks.

It promises stability, flexibility, and controlled growth.

The real test won’t be:

- how many insurers enter

But: - how fairly claims are settled

- how understandable products remain

- how well policyholders are protected

Because in insurance, trust is most important.

Disclaimer : This content is for general information and educational purposes only. It does not constitute legal, tax, accounting, or professional advice. Views expressed are based on prevailing laws and interpretations at the time of publication. Readers should consult their professional advisors before taking any action.

Article related to –

Insurance Bill 2025 explained

FDI insurance reforms India

IRDAI powers insurance bill

insurance sector reform analysis

reinsurance capital norms India

policyholder protection insurance India