Introduction

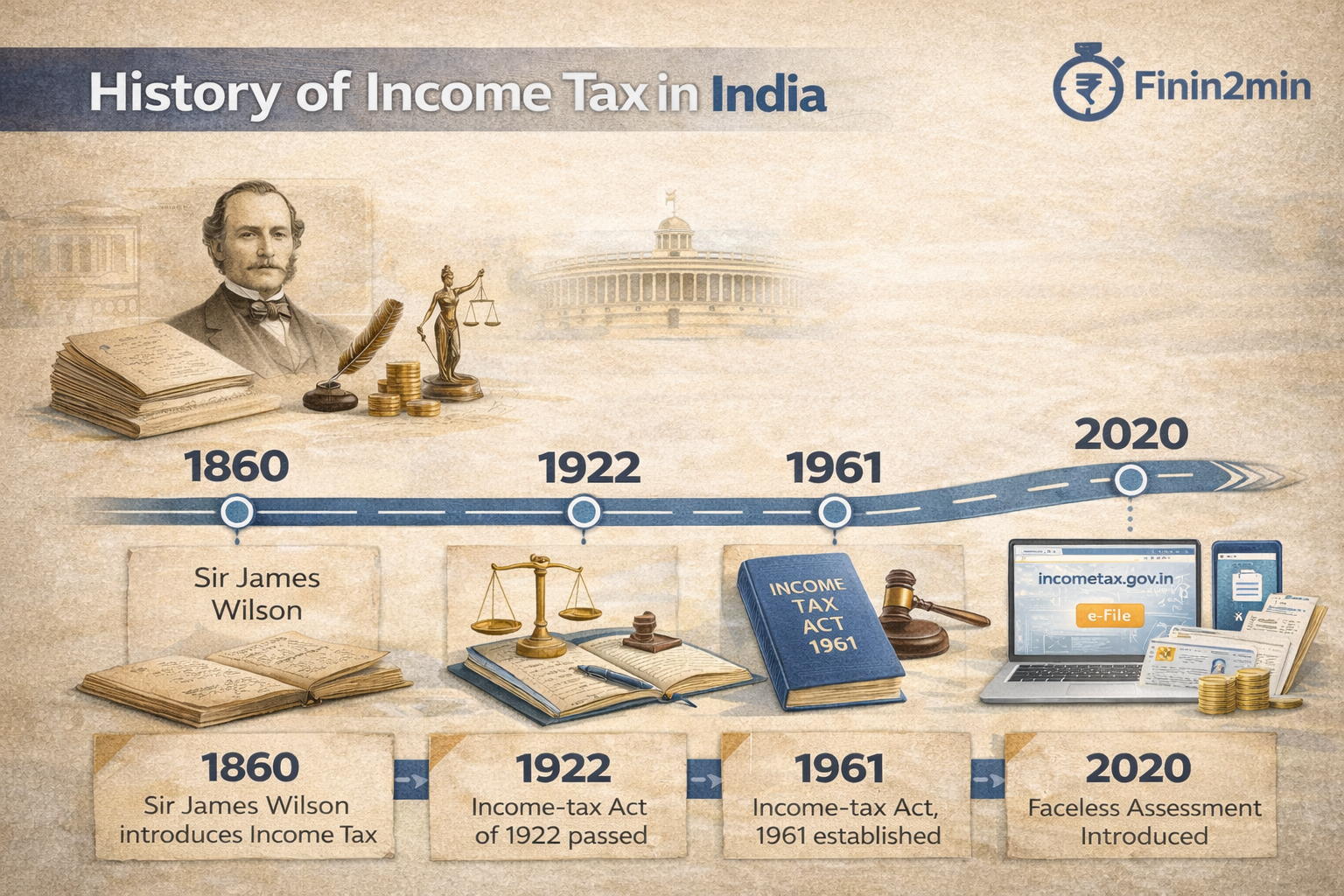

India’s taxation framework has undergone a fascinating journey spanning over 160 years. From Sir James Wilson’s initial tax system in 1860 to the e-filing and faceless assessment era of today, the evolution of Income Tax reflects India’s economic maturity, fiscal reforms, and governance modernization.

Colonial Origins (1860–1947)

- The first Income-tax Act was introduced in 1860 to recover losses after the 1857 Revolt.

- Repealed and re-enacted multiple times, culminating in the Act of 1918 and then Act of 1922, which became the cornerstone of modern taxation.

- British-era taxation targeted trade profits, property income, and salaries.

Post-Independence Reforms

- The Income-tax Act, 1961 replaced the 1922 Act.

- Introduced progressive tax rates and broader coverage of income sources.

- CBDT (Central Board of Direct Taxes) was established to administer policy.

- Early 1990s liberalization further restructured rates and incentives.

Key Milestones

| Year | Reform | Impact |

|---|---|---|

| 1976 | Introduction of PAN concept | Unique taxpayer tracking |

| 1995 | Computerization begins | Faster processing |

| 2006 | Online filing enabled | Accessibility |

| 2019 | Faceless assessment | Transparency |

| 2020 | New tax regime introduced | Optional lower rates |

Digital Transformation

With the launch of incometax.gov.in, e-verification, and AI-based scrutiny, compliance has become simpler. The government’s Vision 2047 aims for near-complete automation of tax administration.

Conclusion

The Indian Income-tax system has transformed from a colonial revenue tool to a sophisticated, citizen-centric framework. Continuous reforms ensure transparency, efficiency, and fairness.

Sources:

Income-tax Act, 1961

CBDT Annual Report 2023