Markets • Macro • Commodities • Policy • Corporates • Global Indices Close • Finin2min

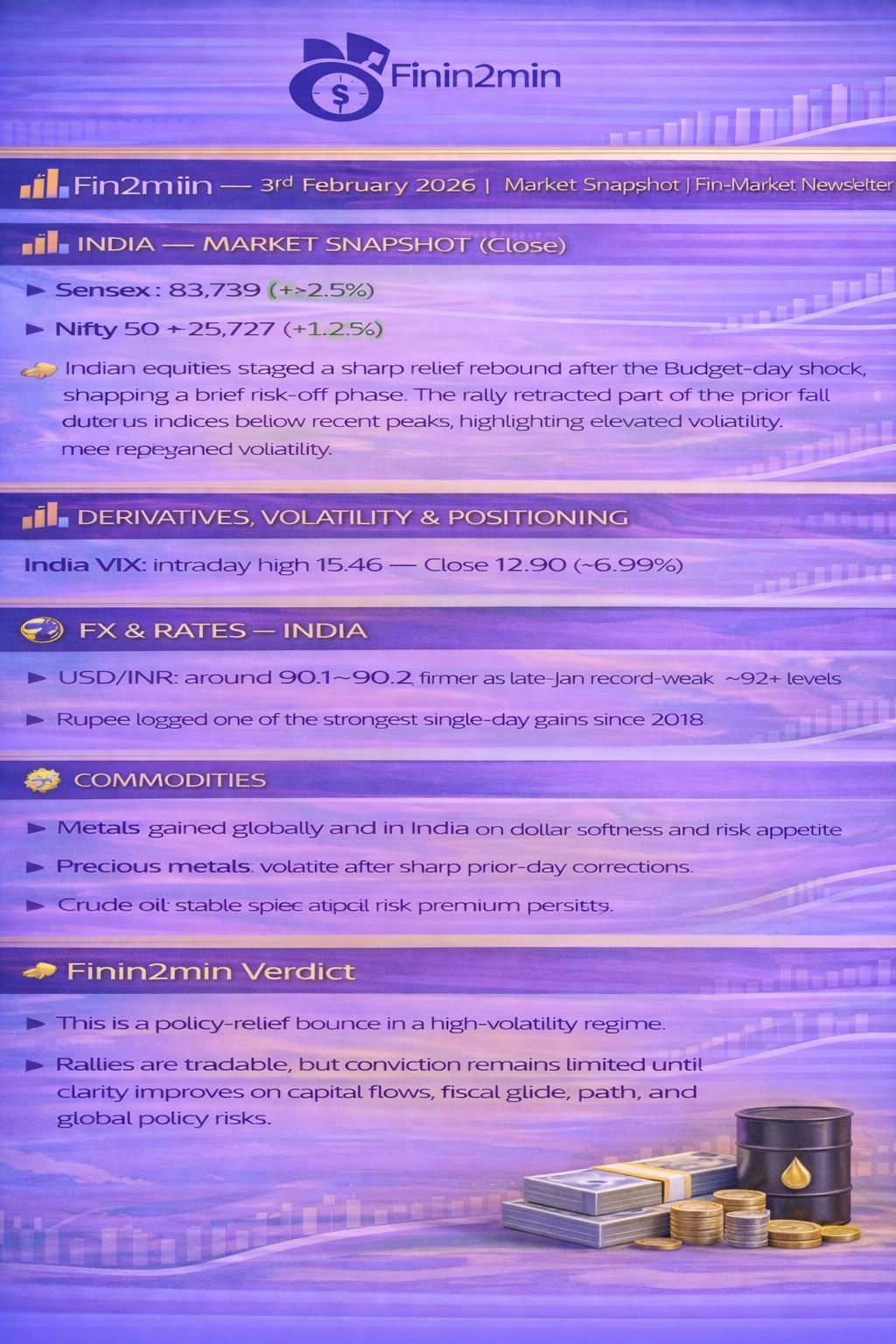

📊 INDIA — MARKET SNAPSHOT (Close)

- Sensex: ~83,739 (+~2.5%)

- Nifty 50: ~25,727 (+~2.5%)

👉 Indian equities staged a sharp relief rebound after the Budget-day shock, snapping a brief risk-off phase. The rally retraced part of the prior fall but indices remain below recent peaks, highlighting elevated volatility.

Character:

Budget-day hangover rebound — strong relief rally with large intraday swings, driven by positioning unwind and selective risk-taking rather than a clean trend reversal.

📊 SECTORAL LEADERS & LAGGARDS — INDIA

Leaders

- Large-cap cyclicals: Energy, ports, metals, defence/PSU names

- Metals gained both globally and in Indian markets, aligning with improved risk appetite

Relative underperformance

- Select defensives and rate-sensitives

👉 Relief rally led by large-cap cyclicals, with midcaps and smallcaps participating but still below recent highs.

📉 DERIVATIVES, VOLATILITY & POSITIONING

- India VIX: Intraday high 15.46 → Close 12.90 (-6.99%)

- Volatility eased from panic levels but remains above pre-Budget comfort zone

Positioning

- Rebound driven by short-covering plus selective fresh long build-up

- Nifty OI and PCR continue to reflect caution rather than full risk-on

👉 Derivatives metrics confirm a relief rally, not a confirmed trend reversal.

💱 FX & RATES — INDIA

- USD/INR: around 90.1–90.2, firmer vs late-Jan record-weak ~92+ levels

- Rupee logged one of the strongest single-day gains since 2018

Narrative

- INR remains in a historically weak zone

- Improvement was modest and partly positioning-driven

- RBI intervention expectations (via dollar sales) underpinned post-Budget stabilisation

🧮 INDIA MACRO — KEY POLICY & ECONOMIC DRIVERS

1️⃣ India–US Trade Deal (Primary Equity Catalyst)

- 18% tariff reduction (from 25%) on Indian goods

- Industrial tariffs to phase down toward 0%

👉 Explicitly drove the ~2.5% equity rally, improving export and FPI sentiment

2️⃣ RBI Dividend Transfer (Major Fiscal Support)

- RBI approved record ₹2.11 lakh crore dividend transfer for FY25

- Provides ₹50,000–60,000 Cr of incremental fiscal space

👉 RBI’s record ₹2.11L Cr dividend transfer provides a fiscal cushion amid a slower consolidation path flagged by rating agencies.

3️⃣ Economic Survey 2026 — Constructive Backdrop

- FY27 GDP growth: 6.8–7.2%

- Manufacturing GVA: +9.13% (Q2 FY26)

- PLI schemes: ₹2 lakh crore investment, ~12.6 lakh jobs

- Agriculture: Horticulture output surpassed foodgrains (362 MT vs 357 MT)

- Banking:

- Gross NPAs 2.2%, Net NPAs 0.5% (lowest in a decade)

- Bank credit growth ~14.5%

👉 Economic Survey’s resilient FY27 outlook and manufacturing/PLI success provided a constructive anchor despite Budget volatility.

4️⃣ Union Budget 2026 — Tax & Market Impact

- STT hike on derivatives: remains the key F&O overhang

- No major CGT relief for FPIs, viewed as a missed opportunity

- ITR revised return deadline: extended to 31 Mar (₹5,000 fee)

- Income tax rebate: income up to ₹12L tax-free

- FPI limits for individuals/PIOs raised to 24% (from 10%) — partial positive offset

👉 Budget STT hikes continue to weigh on derivatives sentiment; higher FPI limits offer some medium-term relief.

5️⃣ SEBI & Liquidity Signals

- SEBI considering additional F&O curbs (weekly expiry limits) post-STT shock

- RBI FY26 dividend budget: Govt has pencilled in ₹3.16L Cr from RBI/PSBs

👉 Regulatory and liquidity signals add to derivatives-driven volatility.

🌍 GLOBAL MARKET CONTEXT

- Global cues remained cautious, not strongly supportive

- US markets recently pressured by tariffs, geopolitics, and higher-for-longer Fed stance

- IMF WEO (Jan): 2026 global growth ~3.3%, AI-led capex offsetting trade headwinds

👉 India’s rally was largely domestic-policy and positioning-led, not global-beta driven.

🪙 COMMODITIES

- Metals: gained globally and in India on dollar softness and risk appetite

- Precious metals: volatile after sharp prior-day corrections

- Crude oil: stable; geopolitical risk premium persists

🌍 GLOBAL EQUITIES (Context)

- FTSE: remains near record highs set at the start of 2026, not a fresh session high

- Other DM equities traded mixed amid macro uncertainty

💰 FLOWS — FPI / DII

- FPIs: structurally cautious after sustained Jan outflows

- DIIs: continued to provide stabilising support

👉 Market remains domestically supported, with foreign participation tentative.

🏢 CORPORATE SPOTLIGHT

- Reliance Industries: ~+3%, major index contributor

- Adani Ports: ~+5%; Q3 FY26 EBITDA +20% YoY (₹5,786 Cr), FY26 guidance raised

- Power Grid: ~+7–8%; FY26 capex ₹32,000 Cr (vs ₹28,000 Cr earlier)

- Defence PSUs (BEL, HAL): continued strength on policy visibility

🗓 KEY EVENTS — TODAY

- Trade-deal driven relief rally

- INR stabilisation post-record weakness

- Metals participation reinforced equity momentum

👀 EVENTS TO WATCH

🇮🇳 India

- RBI liquidity & FX management

- Post-Budget FPI flow trend

- Bond market reaction to borrowing & dividend cushion

🌍 Global

- US inflation data & Fed communication

- Trade/tariff developments

- Dollar and commodity volatility

🧮 FININ2MIN MACRO RISK SCORE (Verified Framework)

📅 3 Feb 2026 | India + Global

| Risk Factor | Score (0–10) | Key Drivers |

|---|---|---|

| 🌍 Global Geopolitics & Trade | 6.8 | US–EU tariff tensions, India–US deal relief, lingering trade uncertainty |

| 🏦 Global Monetary Policy | 6.5 | Fed higher-for-longer stance, policy credibility focus, DM divergence |

| 🇮🇳 India Fiscal / Budget Risk | 6.0 | Slower consolidation path, higher borrowing, partially offset by RBI dividend |

| 💰 Liquidity & Capital Flows | 5.6 | FPI outflows still elevated; DII support + RBI dividend cushion |

| 💱 FX & INR Stability | 6.2 | INR stabilised at 90.1–90.2 but remains historically weak; RBI intervention expected |

| 📉 Market Volatility (VIX / Derivatives) | 5.8 | VIX cooled to 12.90 from 15.46 intraday; OI/PCR still cautious |

| 🪙 Commodities (Metals / Oil) | 5.4 | Metals strength supportive; crude stable with geo-risk premium |

📊 Composite Macro Risk Score: 6.0 / 10

Regime Classification:

⚠️ Elevated Macro Risk — Policy-Driven Volatility (Non-Systemic)

🧠 MACRO RISK INTERPRETATION — FININ2MIN VIEW

- What improved:

- India–US trade deal clarity

- RBI’s record ₹2.11L Cr dividend transfer easing fiscal stress

- INR stabilisation post extreme weakness

- Metals participation supporting risk assets

- What remains a risk:

- FPI flow fragility

- Derivatives overhang (STT + possible SEBI curbs)

- Higher-for-longer global rates

- Elevated policy sensitivity into Feb

📉 Macro Risk Trend (Recent Sessions)

| Date | Composite Score |

|---|---|

| 31 Jan 2026 | 6.2 |

| 2 Feb 2026 | 6.1 |

| 3 Feb 2026 | 6.0 |

👉 Trend: Gradual improvement, but still firmly above “comfort zone”.

📌 Institutional Translation

- Score < 5.5: Clean risk-on / breakout phase

- 5.5 – 6.5: ⚖️ Range-bound, rotation-heavy markets ✅ (current)

- > 7.0: High correction risk

Current probability map (Finin2min):

- 📈 Bull / continuation: 35%

- ⚖️ Range-bound / tactical: 45%

- 📉 Risk-off relapse: 20%

👉 Macro Overlay Verdict

The policy-relief rally lowered near-term macro risk, but the environment remains fragile and event-driven. Until capital flows and FX stabilise structurally, markets are likely to trade tactically, not trend cleanly.

🧠 FININ2MIN — INSTITUTIONAL CLOSING SUMMARY

✅ Sharp relief rally after Budget-day shock, driven by trade deal, RBI dividend cushion and short-covering.

✅ Fiscal consolidation continues but at a slower pace; FPI and INR concerns persist.

✅ Derivatives (VIX, OI, PCR) signal cautious risk-on, not a trend reversal.

✅ Global cues remain mixed; India’s move was policy- and positioning-led.

✅ Metals strength aligned with equity rebound; FX stabilisation remains fragile.

👉 Finin2min Verdict

This is a policy-relief bounce in a high-volatility regime.

Rallies are tradable, but conviction remains limited until clarity improves on capital flows, fiscal glide path, and global policy risks.

Market data and developments are based on live updates, news coverage, and financial sources as of the end of today’s session. Finin2min content is for market insight and discussion only. Not investment advice.