Markets • Macro • Commodities • Policy • Corporates • Global Indices Close • Finin2min

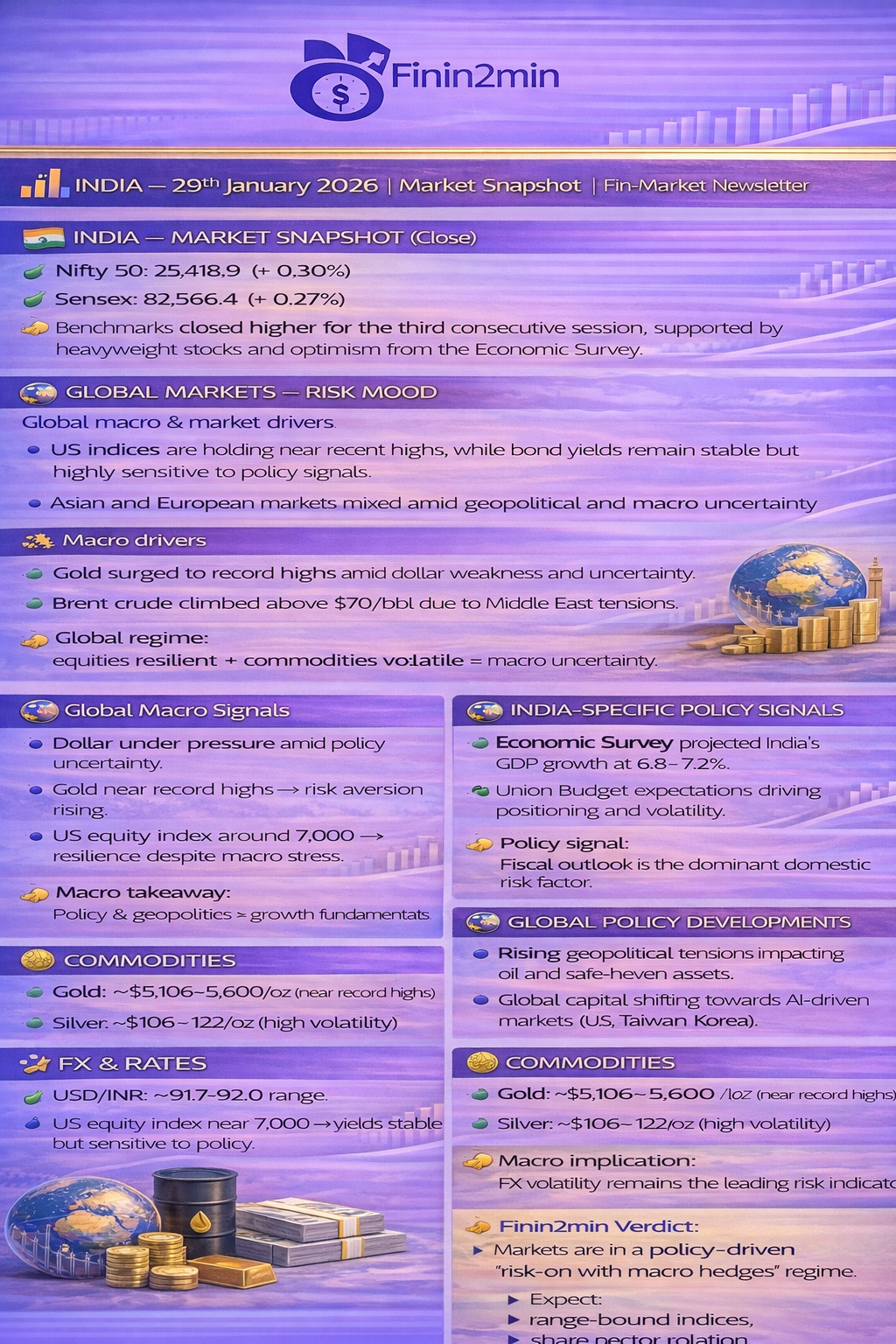

📊 INDIA — MARKET SNAPSHOT (Close)

✅ Nifty 50: 25,418.9 (↑ ~0.30%)

✅ Sensex: 82,566.4 (↑ ~0.27%)

👉 Benchmarks closed higher for the third consecutive session, supported by heavyweight stocks and optimism from the Economic Survey.

📊 Sectoral Breadth (NSE)

🟢 Leaders

- Oil & Gas

- Metals

- Infrastructure / capital goods

🔴 Laggards

- FMCG

- Pharma

👉 Cyclical sectors outperformed defensives, signaling selective risk-on sentiment.

(Aligned with market commentary across Indian media & sector trends)

🌍 GLOBAL MARKETS — RISK MOOD

Equities

- US indices are holding near recent highs, while bond yields remain stable but highly sensitive to policy signals.

- Asian and European markets mixed amid geopolitical and macro uncertainty.

Macro drivers

- Gold surged to record highs amid dollar weakness and uncertainty.

- Brent crude climbed above $70/bbl due to Middle East tensions.

👉 Global regime:

equities resilient + commodities volatile = macro uncertainty.

📉 DERIVATIVES & POSITIONING (India)

India VIX

- India VIX: ~13.3–13.5

👉 Volatility moderate; elevated vs early-Jan lows.

Interpretation:

- Rising index + stable VIX → constructive but hedged risk-on.

📊 NIFTY KEY LEVELS (Options & Technical Consensus)

Resistance zones

- 25,500 → major psychological & options resistance

- 25,800 → breakout zone

Support zones

- 25,000 → strong put base

- 24,700–24,750 → structural support

👉 Market structure:

Range-bound with upside bias.

(Aligned with derivatives outlook and technical commentary)

🧩 F&O POSITIONING — SUMMARY

- Hedging activity elevated near 25,500 strikes

- Put writing near 25,000 suggests downside protection

👉 Institutional positioning:

cautious bullish, not aggressive long.

🧮 FLOWS & MACRO DATA

🇮🇳 FPI / DII FLOWS (Latest Verified)

📅 28 Jan 2026 (official data):

- FPIs: +₹480.3 crore (net buyers)

- DIIs: +₹3,360.6 crore (net buyers)

👉 Liquidity signal:

Domestic institutions dominate market direction.

Structural context:

- DIIs now hold ~18.7% of NSE equities, surpassing FIIs.

🌍 Global Macro Signals

- Dollar under pressure amid policy uncertainty.

- Gold near record highs → risk aversion rising.

- US equity index around 7,000 → resilience despite macro stress.

👉 Macro takeaway:

Policy & geopolitics > growth fundamentals.

🏛 INDIA-SPECIFIC POLICY SIGNALS

- Economic Survey projected India’s GDP growth at 6.8–7.2%.

- Union Budget expectations driving positioning and volatility.

👉 Policy signal:

Fiscal outlook is the dominant domestic risk factor.

🌍 GLOBAL POLICY DEVELOPMENTS

- Rising geopolitical tensions impacting oil and safe-haven assets.

- Global capital shifting towards AI-driven markets (US, Taiwan, Korea).

👉 Policy theme:

Geopolitics + tech capital flows reshaping global asset allocation.

🪙 COMMODITIES (Verified)

- Gold: ~ $5,106–5,600/oz (near record highs)

- Silver: ~ $106-122/oz (high volatility)

- Brent crude: ~ $70–71/bbl

👉 Interpretation:

- Precious metals: safe-haven demand dominates.

- Oil: geopolitical risk premium.

💱 FX & RATES

- USD/INR: ~91.7–92.0 range

- US S&P 500 index near 7,000 → yields stable but sensitive to policy.

👉 Macro implication:

FX volatility remains the leading risk indicator.

📊 SECTORAL ROTATION — INDIA

🟢 Relative strength

- Oil & Gas

- Metals

- Capital goods

🔴 Relative weakness

- FMCG

- Pharma

👉 Rotation signal:

cyclicals outperform defensives → mild risk-on regime.

🏢 CORPORATE HIGHLIGHTS

- Heavyweights like L&T supported indices.

- Commodity-linked stocks outperformed amid oil & metals rally.

- Defensive sectors underperformed.

👉 Corporate theme:

index driven by heavyweights + cyclicals.

🗓 KEY ECONOMIC EVENTS — TODAY

- Economic Survey boosted Indian equity sentiment.

- Oil surged amid geopolitical tensions.

- Gold corrected from record highs amid volatility.

👀 EVENTS TO WATCH

🇮🇳 India

- Union Budget announcement

- FPI flow trend

- Nifty breakout above 25,500

🌍 Global

- Geopolitical developments (Middle East)

- US macro data & Fed signals

- USD and bond yield trend

🧮 FININ2MIN MACRO RISK SCORE (Verified Framework)

| Risk Factor | Score (0–10) |

|---|---|

| Global geopolitics | 7.5 |

| Monetary policy uncertainty | 6.0 |

| Inflation & yields | 5.8 |

| India fiscal risk | 5.5 |

| Liquidity & flows | 4.2 |

👉 Composite Macro Risk Score: 6.2 / 10

➡ Elevated but not systemic.

📊 NEXT-DAY TRADING BIAS (Institutional)

Base Case (60%)

- Range: 25,000 – 25,550

- Bias: mildly bullish / buy-on-dips

- Preferred themes: metals, energy, infra

Bull Case (25%)

- Breakout above 25,500 → 25,800–26,000

Bear Case (15%)

- Breakdown below 25,000 → 24,700

👉 Key trigger:

Budget narrative + global commodity moves.

🧠 FININ2MIN — INSTITUTIONAL CLOSING SUMMARY

✅ India: indices rising, but driven by selective heavyweights and cyclical rotation.

✅ Global: commodities volatility reflects geopolitical and policy uncertainty.

✅ Derivatives: OI structure confirms range-bound market with upside bias.

✅ Flows: domestic institutions remain the stabilising force.

✅ Macro: policy risk dominates near-term pricing.

👉 Finin2min Verdict:

Markets are in a policy-driven “risk-on with macro hedges” regime.

Expect:

- range-bound indices,

- sharp sector rotation,

- volatility spikes around Budget + geopolitics.

Market data and developments are based on live updates, news coverage, and financial sources as of the end of today’s session. Finin2min content is for market insight and discussion only. Not investment advice.