Markets • Macro • Commodities • Policy • Corporates • Global Indices Close • Finin2min

CLOSING DATA — SNAPSHOT (EOD 22 Jan 2026)

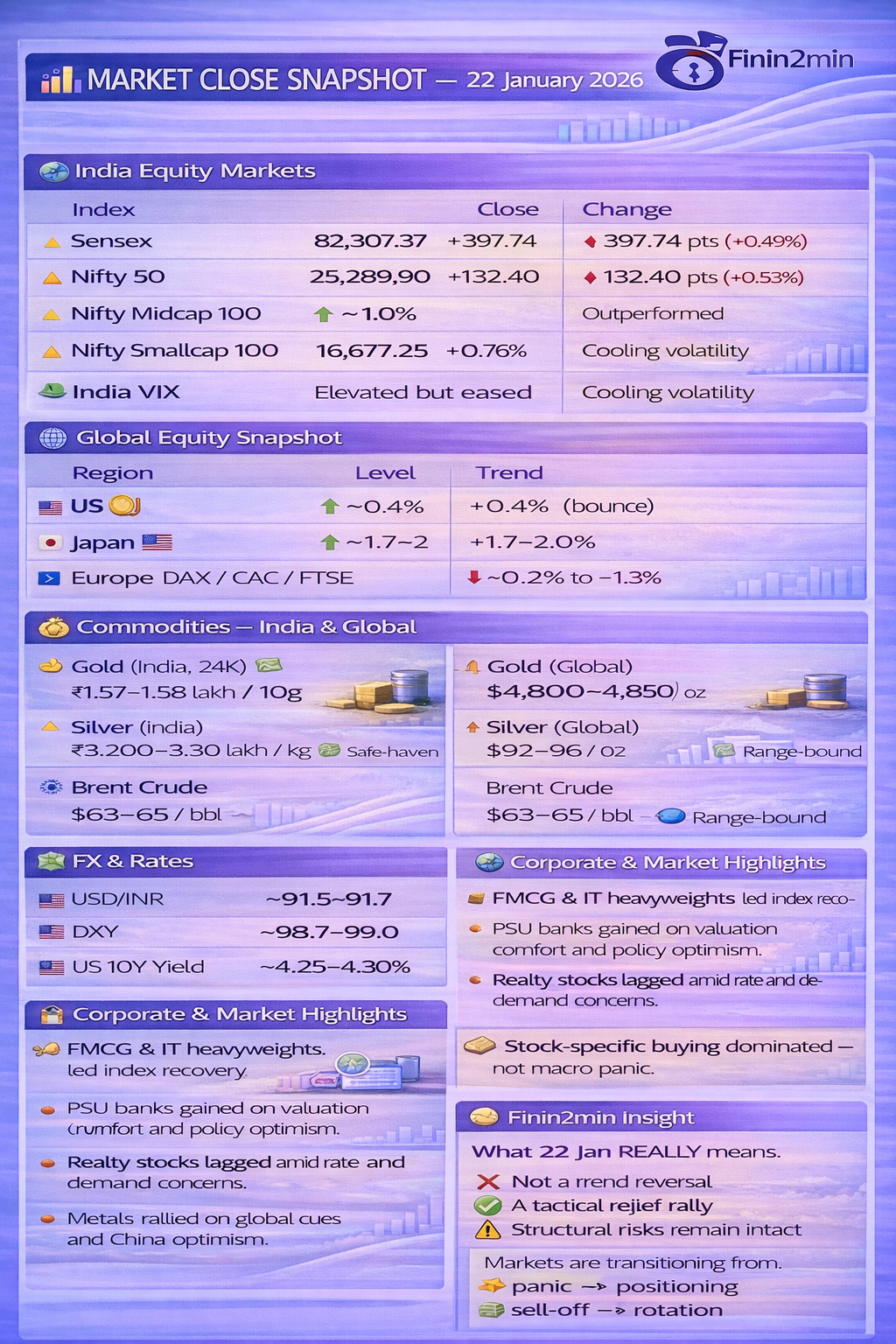

🇮🇳 India Equity Markets

| Index | Close | Change |

|---|---|---|

| Sensex | 82,307.37 | +397.74 pts (+0.49%) |

| Nifty 50 | 25,289.90 | +132.40 pts (+0.53%) |

| Nifty Midcap 100 | ↑ ~1.0% | Outperformed |

| Nifty Smallcap 100 | 16,677.25 | +0.76% |

| India VIX | Elevated but eased | Cooling volatility |

✅ Market framing:

👉 Relief rally — indices up ~0.5%, mid/smallcaps up ~0.8–1%.

👉 Market snapped a 3-day losing streak on improved global cues.

🌍 Global Equity Snapshot

| Region | Index | Trend |

|---|---|---|

| 🇺🇸 US | S&P 500 | ↑ ~0.4% (bounce) |

| 🇯🇵 Japan | Nikkei 225 | ↑ ~1.7–2.0% |

| 🇪🇺 Europe | DAX / CAC / FTSE | ↓ ~0.2% to –1.3% |

| 🌏 Asia ex-Japan | Mixed | Stabilisation |

👉 Global tone: stabilisation, not risk-off.

🪙 Commodities — India & Global

| Asset | Level | Trend |

|---|---|---|

| Gold (India, 24K) | ₹1.57–1.58 lakh / 10g | ↑ |

| Silver (India) | ₹3.20–3.30 lakh / kg | ↑ |

| Gold (Global) | $4,800–4,850 / oz | ↑ Safe-haven |

| Silver (Global) | $92–96 / oz | ↑ Strong |

| Brent Crude | $63–65 / bbl | → Range-bound |

✅ Key insight:

- Gold & silver reflect geopolitical hedging.

- Oil remains capped despite risk premiums.

- Gold structurally supported by strong investor and central‑bank demand (Goldman raised forecast)

💱 FX & Rates

| Indicator | Level |

|---|---|

| USD/INR | ~91.5–91.7 |

| DXY | ~98.7–99.0 |

| US 10Y Yield | ~4.25–4.30% |

👉 INR remains structurally weak despite equity bounce.

📈 Sectoral Performance — India

🟢 Outperformers (1–2%+ gains)

- FMCG

- IT

- Metals

- PSU Banks

- Pharma

🔴 Laggards

- Realty

- Consumer Durables

✅ Key takeaway:

👉 Broad-based rebound with selective laggards — not a defensive-only rally.

🏢 Corporate & Market Highlights

- FMCG & IT heavyweights led index recovery.

- PSU banks gained on valuation comfort and policy optimism.

- Realty stocks lagged amid rate and demand concerns.

- Metals rallied on global cues and China optimism.

👉 Stock-specific buying dominated — not macro panic.

🌍 Macro & Global Context

Key Drivers

- Improved global risk sentiment.

- Stabilisation in US equities.

- Easing volatility after earlier sell-off.

- Persistent INR weakness.

Weekly Macro Backdrop

- Risk-off regime still intact.

- FPI flows remain cautious.

- Gold remains hedge asset.

- Policy & geopolitics > earnings.

🧠 Finin2min Insight

What 22 Jan REALLY means:

❌ Not a trend reversal

✅ A tactical relief rally

⚠️ Structural risks remain intact

Markets are transitioning from:

👉 panic → positioning

👉 sell-off → rotation

✅ Finin2min Bottom Line

📌 22 Jan was a relief bounce, not a risk-on comeback.

- India equities rebounded ~0.5%, led by FMCG, IT and PSU banks.

- Midcaps and smallcaps confirmed risk appetite returning.

- Gold and silver stayed elevated, signalling persistent macro hedging.

- INR weakness and bond yields suggest underlying stress remains.

👉 2026 markets are being driven by policy, geopolitics and capital flows — not earnings.

Today was a relief rally in a fragile regime.

Global politics eased temporarily, lifting equities, but persistent FPI outflows and elevated gold prices suggest markets are still in risk‑aware mode.

➡️ Near‑term bias: Range‑bound with upside attempts

➡️ Structural signal: Defensive hedges still in play

➡️ Trend verdict: Correction paused — not over

Strategy: Selectivity > beta.

Market data and developments are based on live updates, news coverage, and financial sources as of the end of today’s session. Finin2min content is for market insight and discussion only. Not investment advice.