How to Get Out of Them — Law, Facts & Strategy

Few GST allegations cause as much panic as being branded a “fake invoice case.”

Once this label is attached, matters escalate rapidly—summons, search, arrest risk under Section 69, provisional attachment under Section 83, and even ED references under PMLA.

What is deeply concerning is that a large number of such cases do not involve actual fraud. Instead, they arise due to:

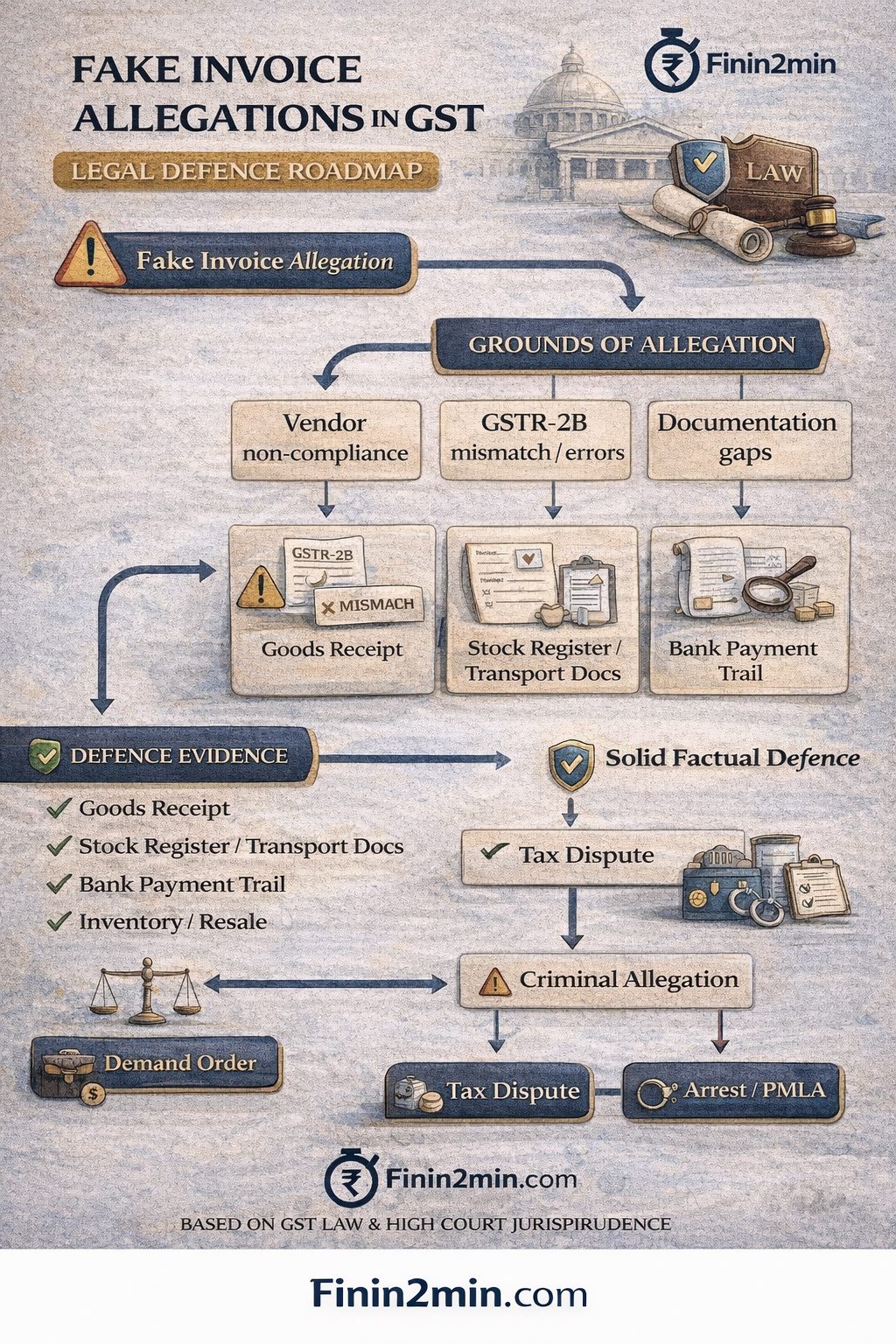

- Vendor non-compliance

- Data mismatches

- Documentation gaps

- Pressure-recorded statements

This article explains how fake invoice allegations arise, what the law actually requires, how courts view such cases, and how businesses can defend themselves effectively.

1️⃣ What Do GST Authorities Mean by “Fake Invoices”?

Legal Meaning (as per CGST Act)

Under GST law, “fake invoicing” generally refers to situations involving:

| Nature of Allegation | Legal Basis |

|---|---|

| Invoice without supply | Section 16 + Section 132 |

| ITC without receipt of goods/services | Section 16(2)(b) |

| Circular trading without economic substance | Section 132 |

| Passing on ITC fraudulently | Section 132(1)(c) |

Important:

There is no statutory definition of “fake invoice”. The term is investigative, not legislative.

⚠️ Problem in practice:

Officers often apply a much broader meaning, equating supplier default or data mismatch with fake supply, which is legally unsustainable.

2️⃣ How Genuine Businesses Get Trapped

i️) Vendor Non-Compliance (Most Common Cause)

Typical scenario:

- Supplier files GSTR-1 late / not at all

- Supplier becomes non-traceable

- ITC does not reflect in GSTR-2B

Departmental leap:

“Supplier is fake → invoices are fake → ITC is fraud.”

🔍 Legal reality:

Courts have repeatedly held that buyer cannot be punished for supplier’s subsequent default, if:

- Goods/services were actually received

- Payment was made through banking channels

ii️) Mechanical Reliance on GSTR-2B

Fact-check:

✔ GSTR-2B is a compliance tool, not a conclusive test of fraud.

Common reasons for 2B mismatch:

- Late GSTR-1 filing

- Amendments in later periods

- Technical portal errors

Law:

Non-reflection in 2B does not automatically establish fake invoicing.

It only triggers verification, not criminal inference.

iii️) Circular Trading Allegations via Data Analytics

GST intelligence relies heavily on network analytics, flagging:

- Low margins

- High turnover

- Related-party transactions

- Repetitive supply chains

⚠️ Risk:

Analytics detect patterns, not proof.

✔ Courts have accepted that actual movement of goods, stock usage, and payments override algorithmic suspicion.

iv️) Documentation Gaps ≠ Fake Transactions

Many cases collapse because the allegation is based on:

- Missing e-way bills

- Weak stock registers

- Poor linkage between invoice & payment

Fact-check:

These are compliance lapses, not proof of non-supply.

Fraud must be proved, not presumed.

v️) Statements Recorded Under Pressure

Statements recorded during:

- Search (Section 67)

- Summons (Section 70)

often become the sole foundation of fake invoice cases.

Judicial position:

- Statements without corroboration cannot sustain criminal liability

- Retraction, if prompt and reasoned, is legally recognised

3️⃣ Why Fake Invoice Allegations Escalate So Quickly

Once the word “fake” enters departmental records:

| Consequence | Legal Provision |

|---|---|

| Arrest risk | Section 69 |

| Provisional attachment | Section 83 |

| ED reference | PMLA (scheduled offence logic) |

Critical point:

GST law does not mandate arrest merely because ITC is disputed.

Yet escalation often happens before adjudication.

4️⃣ What Courts Have Consistently Held (Fact-Checked)

Across High Courts, the following principles are settled:

| Judicial Principle | Status |

|---|---|

| ITC cannot be denied solely due to supplier default | ✅ Settled |

| Actual receipt of goods/services is the core test | ✅ Settled |

| Arrest is not routine in tax disputes | ✅ Settled |

| Documentary evidence > assumptions | ✅ Settled |

Courts insist authorities must verify:

- Transportation records

- Stock movement

- Banking trail

- Consumption or resale

before branding transactions as fake.

5️⃣ How to Defend Fake Invoice Allegations

i️) Build a Factual Defence (Most Critical)

Your defence must demonstrate:

| Evidence | Importance |

|---|---|

| Receipt of goods/services | 🔴 Essential |

| E-way bills / transport docs | 🔴 Essential |

| Stock registers | 🔴 Essential |

| Bank payments | 🔴 Essential |

| Consumption / resale | 🔴 Essential |

Fake invoice cases collapse on facts, not on legal citations.

ii️) Vendor Due Diligence — Your First Shield

Maintain:

- Vendor GST registration proof

- KYC documents

- Contracts / purchase orders

- Periodic compliance checks

✔ Courts treat documented diligence as bonafide conduct.

iii️) Handle Summons & Statements Strategically

Do not:

- Rush into oral explanations

- Sign statements without review

- Accept dictated language

Do:

- Prefer written submissions

- Seek documents before answering

- Retract promptly if recorded under pressure

📌 A bad statement can damage a strong factual case.

iv️) Challenge Arrests & Attachments Early

Courts intervene when:

- No independent satisfaction is recorded

- Arrest is disproportionate

- Business operations are paralysed

✔ Silence strengthens the department’s narrative.

6️⃣ Separate Tax Dispute from Criminal Allegation

⚠️ Critical legal distinction:

| Situation | Legal Meaning |

|---|---|

| ITC disallowed | Tax dispute |

| Tax payable | Civil liability |

| Fake invoice allegation | Criminal charge (Section 132) |

Tax liability ≠ fake invoicing ≠ money laundering

This distinction is central to defending arrest and PMLA exposure.

7️⃣ Preventive Framework (Litigation-Driven)

Businesses should institutionalise:

- 2B-based ITC discipline

- Real-time stock reconciliation

- High-risk vendor reviews

- Document preservation protocols

- Internal GST investigation SOP

✔ Prevention is cheaper than defence.

📊 Summary Chart — Fake Invoice Defence Matrix

| Area | Weak Position | Strong Defence |

|---|---|---|

| ITC | 2B mismatch | Goods receipt + payment |

| Vendor | Non-traceable | Due diligence records |

| Docs | Missing | Corroborated trail |

| Statements | Oral admissions | Written, verified |

| Enforcement | Passive | Early legal challenge |

🔚 Final Thought

Fake invoice allegations are among the most aggressive tools in GST enforcement—but also among the most frequently over-extended.

In practice, many cases are not about fraud, but about:

- Documentation gaps

- Data-driven assumptions

- Pressure-based investigations

A calm, factual, and legally structured response—taken early—can dismantle even the most serious allegations.