A Finin2min Compliance Playbook (India)

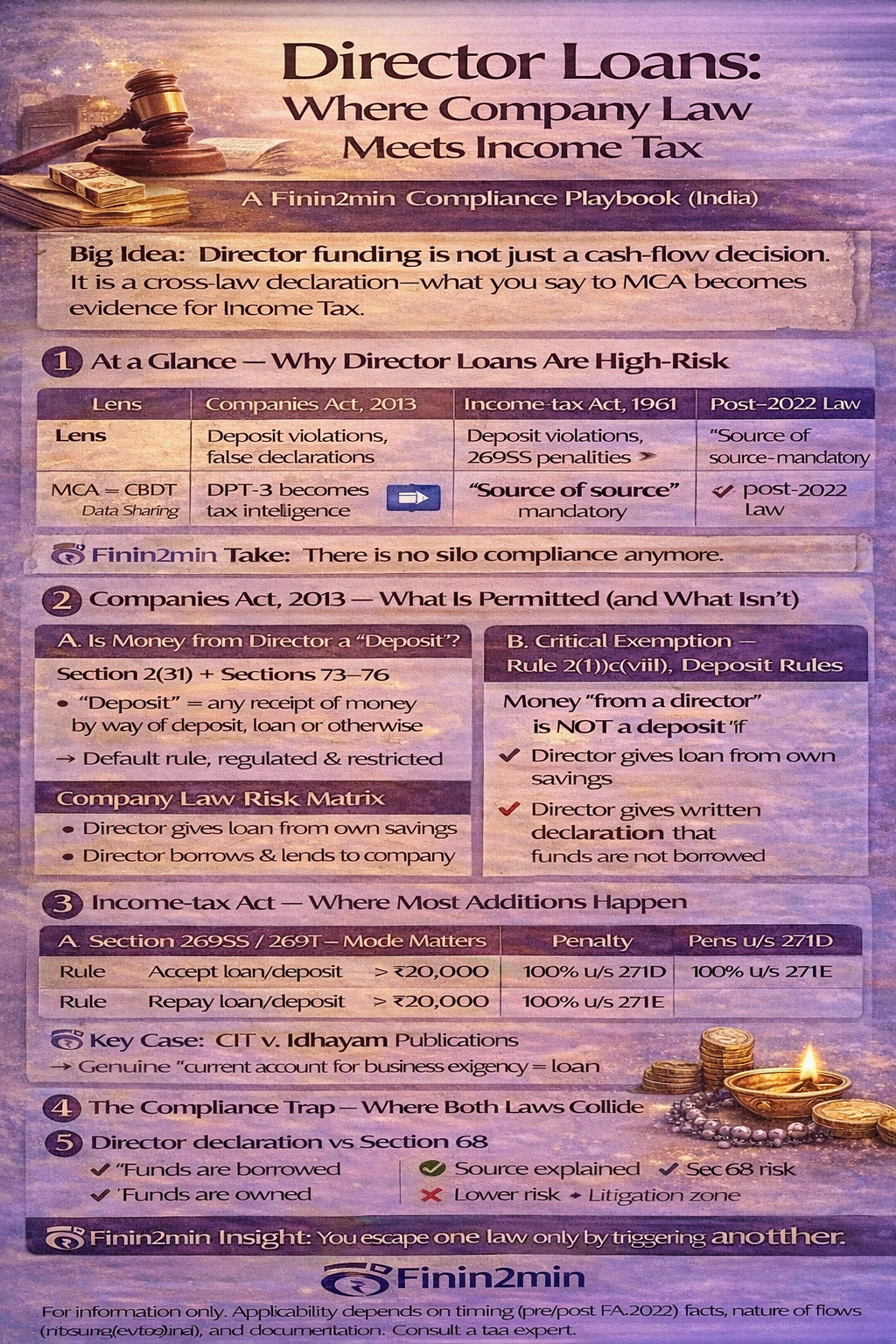

Big Idea:

Director funding is not just a cash-flow decision.

It is a cross-law declaration—what you say to MCA becomes evidence for Income Tax.

1️⃣ At a Glance — Why Director Loans Are High-Risk

| Lens | Risk Trigger |

|---|---|

| Companies Act, 2013 | Deposit violations, false declarations |

| Income-tax Act, 1961 | Section 68 additions, 269SS penalties |

| MCA ↔ CBDT Data Sharing | DPT-3 becomes tax intelligence |

| Post-2022 Law | “Source of source” mandatory |

Finin2min Take:

There is no silo compliance anymore.

2️⃣ Companies Act, 2013 — What Is Permitted (and What Isn’t)

A. Is Money from Director a “Deposit”?

Section 2(31) + Sections 73–76

“Deposit” = any receipt of money by way of deposit, loan, or otherwise

→ Default rule: regulated & restricted

B. Critical Exemption — Rule 2(1)(c)(viii), Deposit Rules

Money from a director is NOT a deposit if:

✔ Director was a director at time of receipt

✔ Director gives written declaration that funds are not borrowed

⚠️ This declaration is the compliance fulcrum

📌 Company Law Risk Matrix

| Scenario | Outcome |

|---|---|

| Director gives loan from own savings | ✅ Exempt deposit |

| Director borrows & lends to company | ❌ Deposit violation |

| False declaration | ❌ ₹1 Cr+ penalty + prosecution |

3️⃣ Income-tax Act — Where Most Additions Happen

A. Section 269SS / 269T — Mode Matters

| Rule | Threshold | Penalty |

|---|---|---|

| Accept loan/deposit | > ₹20,000 | 100% u/s 271D |

| Repay loan/deposit | > ₹20,000 | 100% u/s 271E |

✔ Only banking channels allowed

✔ Journal entries = litigation zone

📚 Key Case: CIT v. Idhayam Publications

→ Genuine current account for business exigency ≠ loan

B. Section 68 — The Real Weapon

Unexplained cash credits

3 Tests:

- Identity

- Creditworthiness

- Genuineness

🔥 Post-Finance Act 2022 (w.e.f. AY 2023-24)

For loans & borrowings, explanation fails unless:

Director ALSO explains source of his funds

This pierces the corporate veil.

4️⃣ The Compliance Trap — Where Both Laws Collide

⚠️ Director Declaration vs Section 68

| Director says… | Company Law Impact | Tax Impact |

|---|---|---|

| “Funds are borrowed” | ❌ Deposit violation | ✔ Source explained |

| “Funds are owned” | ✔ MCA compliant | ❌ Section 68 risk |

Finin2min Insight:

You escape one law only by triggering another unless documents align.

5️⃣ Form DPT-3 — The Silent Evidence File

What DPT-3 Discloses:

- Director loans (amount, date, interest)

- Outstanding balances

- Auditor certification

📡 MCA ↔ CBDT MoU = automated scrutiny

📊 DPT-3 Classification → Tax Consequence

| DPT-3 Disclosure | Company Law | Income Tax |

|---|---|---|

| Loan from Director | ✔ Exempt deposit | Sec 68 + 269SS |

| Share application | ✔ (60 days) | Sec 68 |

| Trade advance | ✔ (<365 days) | Lower risk |

| Not disclosed | ❌ Violation | Adverse inference |

6️⃣ “Current Account” Defence — Powerful but Dangerous

Supporting Case

📚 CIT v. Idhayam Publications

✔ Survival funds ≠ loan for 269SS

But…

- Companies Act does not recognise “director current account”

- Schedule III forces classification as borrowings

- DPT-3 disclosure can override tax defence

🧠 Rule:

You cannot say “current account” to AO and “loan” to RoC.

7️⃣ Deemed Dividend Risk — Section 2(22)(e)

When money flows from company → director

| Condition |

|---|

| Closely held company |

| Director >10% shareholder |

| Loan / advance |

| Accumulated profits |

| ➡ Taxed as dividend |

📚 Tarulata Shyam v. CIT

Character at time of payment matters—even if repaid.

8️⃣ Interest on Director Loans — Double Scrutiny

| Law | Provision | Risk |

|---|---|---|

| Companies Act | Sec 188 | RPT approvals |

| Income Tax | Sec 40A(2) | Excessive interest disallowed |

✔ Higher rate justified for unsecured loans

❌ Shareholder approval ≠ tax allowability

9️⃣ Best-Practice Compliance Playbook (Finin2min)

✅ Before Accepting Funds

- Review director’s personal balance sheet

- Avoid cash unless unavoidable

- Ensure bank trail

📄 Mandatory Documents

- Director “owned funds” declaration

- Board resolution citing Rule 2(1)(c)(viii)

- Loan agreement (tenure, interest)

- Timely DPT-3 filing

- Alignment with Form 3CD

🔟 Final Takeaway — Unified Compliance Theory

A director loan cannot be:

• a current account for tax

• a loan for MCA

• a trade advance for GST

Choose one character. Defend it everywhere.

⚠️ Disclaimer

For information only. This summary is based on prevailing statutory provisions and judicial precedents. Applicability depends on facts, timing (pre/post Finance Act 2022), and documentation. Professional advice recommended.

Article related to –

Director loan Companies Act Income Tax

Director loan Section 68 implications

DPT-3 director loan tax risk

Rule 2(1)(c)(viii) director declaration

Director loan source of source

Director funding private limited company

Section 269SS director loan

Director loan compliance India

Cash credit director loan tax

MCA DPT-3 income tax scrutiny