SCN issued before reply deadline is legally unsustainable

1️⃣ Case Snapshot (At a Glance)

| Particular | Details |

|---|---|

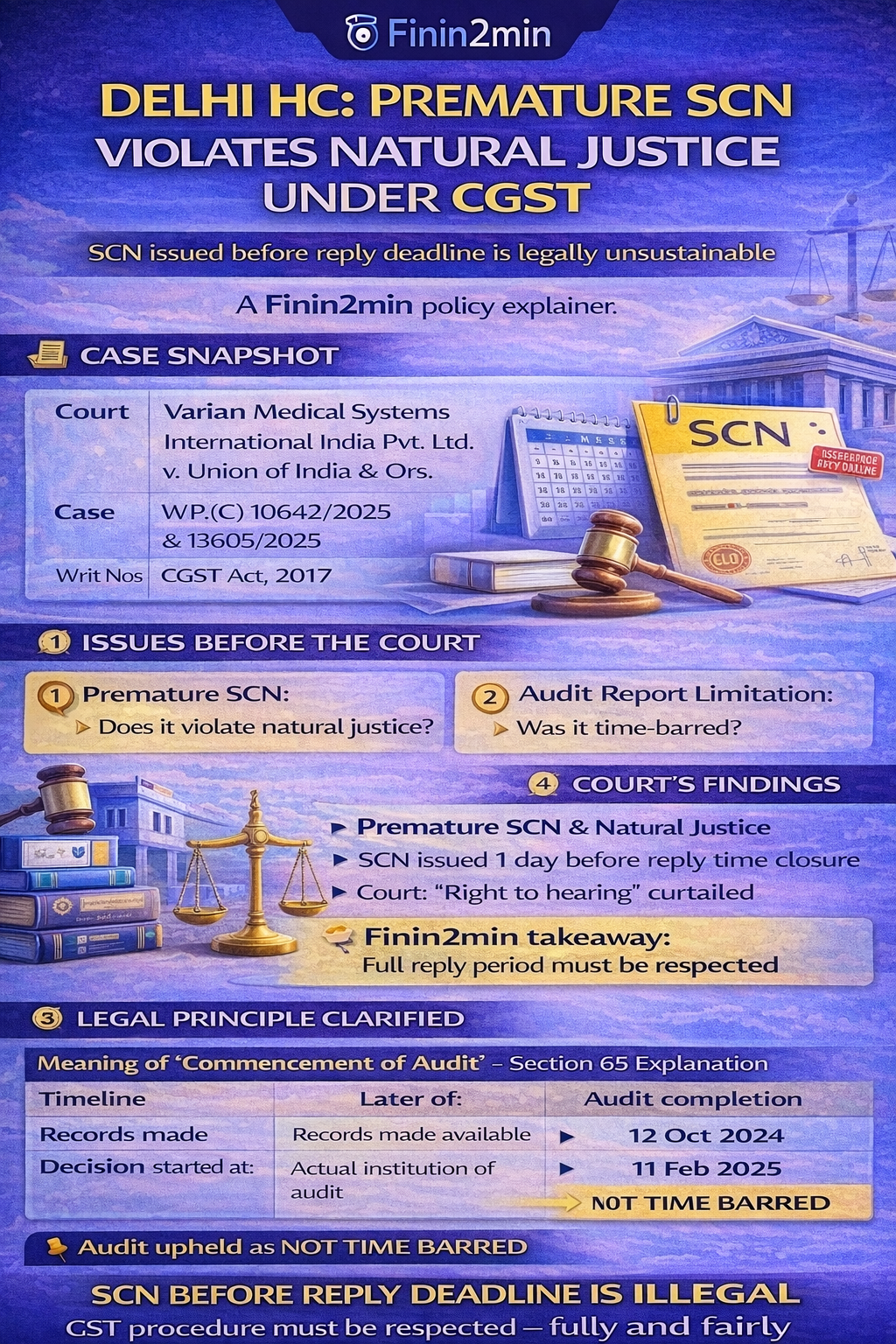

| Court | Delhi High Court |

| Case | Varian Medical Systems International India Pvt. Ltd. v. Union of India & Ors. |

| Writ Nos. | W.P.(C) 10642/2025 & 13605/2025 |

| Law Involved | CGST Act, 2017 |

| Core Issue | Premature issuance of SCN |

| Decision | SCN set aside |

2️⃣ Factual Timeline (Critical Dates)

| Event | Date |

|---|---|

| Audit period | FY 2017–18 to FY 2022–23 |

| Pre-SCN issued | 25 Nov 2024 |

| Time granted to reply | 3 days |

| SCN issued | 27 Nov 2024 |

| Reply window expiry | 28 Nov 2024 |

| Audit report issued | 11 Feb 2025 |

| Audit report communicated | 13 Feb 2025 |

📌 Key fact: SCN issued one day before expiry of reply period.

3️⃣ Issues Before the Court

| Issue No. | Legal Question |

|---|---|

| 1 | Does issuing SCN before expiry of pre-SCN reply period violate natural justice? |

| 2 | Was the audit report time-barred under Section 65 CGST Act? |

4️⃣ Court’s Findings — Issue-wise

Issue 1: Premature SCN & Natural Justice

| Aspect | Court’s Observation |

|---|---|

| Reply time granted | 3 days |

| SCN timing | Issued before expiry |

| Legal principle | Right to meaningful hearing |

| Court’s view | Violation of natural justice |

📌 Finin2min takeaway:

Granting time is meaningless if the authority doesn’t wait for it to expire.

Issue 2: Limitation under Section 65 (Audit)

| Aspect | Court’s Interpretation |

|---|---|

| Audit completion timeline | 3 months from commencement |

| Commencement of audit | Later of: • Records made available OR • Actual institution of audit |

| Petitioner’s final submission | 11 Oct 2024 |

| Audit commencement date | 12 Oct 2024 |

| Audit report date | 11 Feb 2025 |

| Limitation status | Within time |

📌 Audit report upheld as not time-barred.

5️⃣ Legal Principle Clarified (Very Important)

Meaning of “Commencement of Audit” – Section 65 Explanation

| Option | Applicable Date |

|---|---|

| Records made available by taxpayer | ✔ |

| Actual institution of audit | ✔ |

| Relevant date | Whichever is later |

📌 This interpretation protects both taxpayer certainty and departmental timelines.

6️⃣ Final Directions of the Court

| Direction | Outcome |

|---|---|

| SCN dated 27 Nov 2024 | Set aside |

| Matter status | Remanded to pre-SCN stage |

| Fresh reply allowed till | 10 Nov 2025 |

| Department’s liberty | To decide afresh on SCN issuance |

| Limitation exclusion | Writ pendency period excluded |

| Compliance standard | Law + natural justice mandatory |

7️⃣ What the Department Did Wrong (Finin2min Lens)

| Step | Legal Defect |

|---|---|

| Issued pre-SCN | ✔ Correct |

| Granted reply time | ✔ Correct |

| Issued SCN before expiry | ❌ Fatal |

| Opportunity of hearing | ❌ Illusory |

📌 Natural justice is procedural, not cosmetic.

8️⃣ Practical Impact for GST Taxpayers & Professionals

| Area | Implication |

|---|---|

| Pre-SCN stage | Must be meaningfully respected |

| SCN challenge | Strong ground if issued prematurely |

| Audit limitation | Commencement date is fact-driven |

| Writ remedy | Maintainable for procedural breach |

9️⃣ Relevant Statutory Provision (Quick Reference)

Section 65, CGST Act — Key Points

| Sub-section | Essence |

|---|---|

| 65(4) | Audit to be completed within 3 months |

| Proviso | Extension up to 6 months allowed |

| Explanation | Commencement = later of records / audit start |

| 65(6) | Findings to be communicated within 30 days |

| 65(7) | Action under Sections 73 / 74 thereafter |

🔟 Finin2min Bottom Line

| What the HC Made Clear | Why It Matters |

|---|---|

| Reply period must fully run | Procedural fairness |

| SCN before expiry = illegal | SCN collapses |

| Audit timelines strictly construed | Limitation clarity |

| Natural justice is enforceable | Not discretionary |

Final Finin2min Verdict

A Show Cause Notice issued before expiry of the reply period is not just irregular — it is illegal.

This judgment reinforces that GST enforcement must respect procedure as much as power.

Disclaimer : This content is for general information and educational purposes only. It does not constitute legal, tax, accounting, or professional advice. Views expressed are based on prevailing laws and interpretations at the time of publication. Readers should consult their professional advisors before taking any action

Article related to –

Delhi High Court GST SCN natural justice

premature show cause notice GST

CGST audit limitation section 65

GST audit commencement explained

SCN issued before reply period illegal

GST writ petition natural justice