(AY 2025–26 | FY 2024–25)

Filing timelines under the Income-tax Act, 1961 are strictly enforced. However, the law also provides graded remedial mechanisms for taxpayers who miss deadlines.

For Assessment Year (AY) 2025–26, 31 December 2025 is a critical cut-off date. After this date, the choice narrows significantly.

This article explains — in a practical, tabular format — which option remains available, its cost, limitations, and compliance implications.

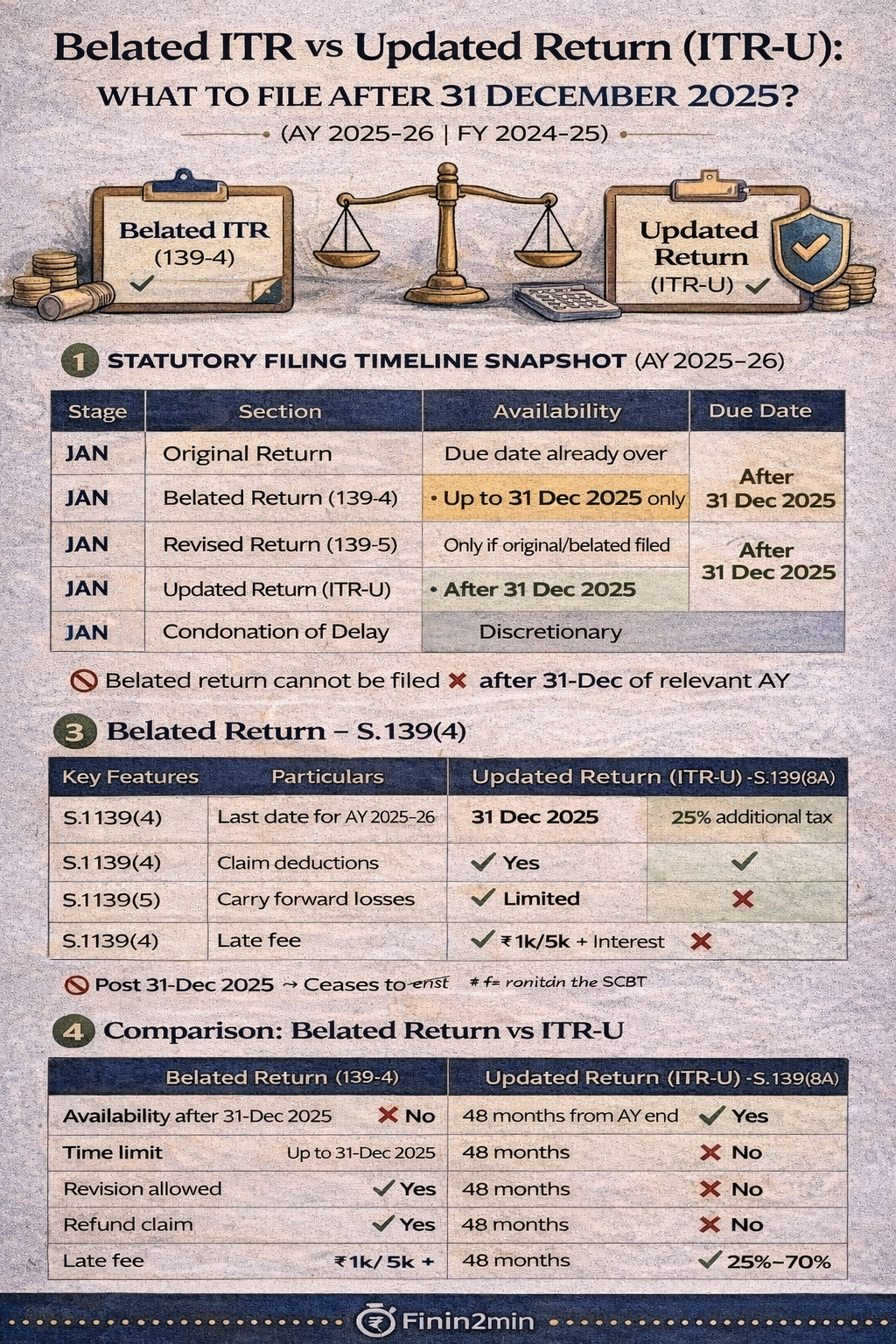

1️⃣ Statutory Filing Timeline Snapshot (AY 2025–26)

| Stage | Section | Availability |

|---|---|---|

| Original return | 139(1) | Due date already over |

| Belated return | 139(4) | Up to 31 Dec 2025 only |

| Revised return | 139(5) | Only if original/belated filed |

| Updated return (ITR-U) | 139(8A) | After 31 Dec 2025 |

| Condonation of delay | 119(2)(b) | Discretionary |

Belated/revised return cannot be filed after 31 December of the relevant AY (unless assessment completed earlier).

2️⃣ Belated Return — Section 139(4)

A belated return allows filing after missing the original due date but within the statutory window.

Key Features

| Particulars | Position |

|---|---|

| Last date for AY 2025–26 | 31 December 2025 |

| Can claim deductions (80C, 80D, etc.) | ✅ Yes |

| Can revise later | ✅ Yes (within time) |

| Carry forward losses | ⚠️ Limited (business & capital loss not allowed) |

| Refund claim | ✅ Allowed |

| Late fee | ₹1,000 / ₹5,000 (Section 234F) |

| Interest | Sections 234A/B/C |

🔔 Post-31 December 2025 → This option ceases to exist

3️⃣ Updated Return (ITR-U) — Section 139(8A)

Introduced to promote voluntary post-deadline compliance, ITR-U is available even after belated/revised timelines expire, but at a cost and with restrictions.

Eligibility Window

| Time from end of AY 2025–26 | Additional Tax Payable* |

|---|---|

| Up to 12 months (till 31 Mar 2027) | 25% of tax + interest |

| 12–24 months | 50% |

| 24–36 months | 60% |

| 36–48 months (till 31 Mar 2030) | 70% |

* Additional tax is levied under Section 140B

Restrictions (Critical)

| Item | Allowed in ITR-U? |

|---|---|

| Declare loss | ❌ No |

| Carry forward losses | ❌ No |

| Claim or enhance refund | ❌ No |

| Reduce earlier tax liability | ❌ No |

| Revise ITR-U | ❌ Not permitted |

| Proceedings already initiated | ❌ Not allowed |

ITR-U is only upward-correction oriented.

4️⃣ Belated Return vs Updated Return — Side-by-Side Comparison

| Parameter | Belated Return (139-4) | Updated Return (139-8A) |

|---|---|---|

| Availability after 31 Dec 2025 | ❌ No | ✅ Yes |

| Time limit | Up to 31 Dec 2025 | 48 months from AY end |

| Revision allowed | ✅ Yes | ❌ No |

| Refund claim | ✅ Yes | ❌ No |

| Loss declaration | ⚠️ Limited | ❌ No |

| Carry forward losses | ⚠️ Restricted | ❌ No |

| Additional tax | ❌ No | ✅ 25%–70% |

| Nature | Regular compliance | Voluntary correction |

| Best used for | Late but genuine filing | Risk mitigation |

5️⃣ What Are Your Options After 31 December 2025?

Option A — ITR-U (Statutory Route)

✔ Predictable

✔ Time-bound

✔ Avoids prosecution risk

✖ Costly

✖ No refunds or losses

Best for:

- Missed filing entirely

- Under-reported income

- Compliance clean-up

Option B — Condonation of Delay (Section 119(2)(b))

| Feature | Position |

|---|---|

| Authority | CBDT / Jurisdictional PCIT |

| Relief possible | Refund / deduction |

| Approval | Discretionary |

| Time | Uncertain |

| Grounds required | Genuine hardship |

⚠️ Not a right — only a discretionary relief

6️⃣ Compliance Decision Matrix (Finin2min Practical View)

| Situation | Recommended Action |

|---|---|

| Missed filing but before 31 Dec 2025 | File Belated Return immediately |

| Missed filing after 31 Dec 2025 | Evaluate ITR-U |

| Refund involved | Consider condonation |

| Under-reported income | ITR-U safer than waiting |

| Loss carry-forward needed | No remedy post-deadline |

7️⃣ Key Takeaways (Executive Summary)

- 31 December 2025 is the final statutory exit for belated returns

- After this date, ITR-U is the only guaranteed compliance route

- ITR-U comes with higher tax cost and strict limitations

- Refunds and loss benefits die after the belated deadline

- Condonation should be used sparingly and strategically

📌 Finin2min Compliance Insight

“File within the belated window whenever possible.

Post-deadline compliance is no longer about saving tax — it is about managing risk.”