It’s about control without operations

At first glance, Adani’s latest move looks confusing.

The group has repeatedly said it doesn’t like businesses with:

- volatile cash flows

- low margins

- heavy operational risk

That’s why it stayed away from running an airline.

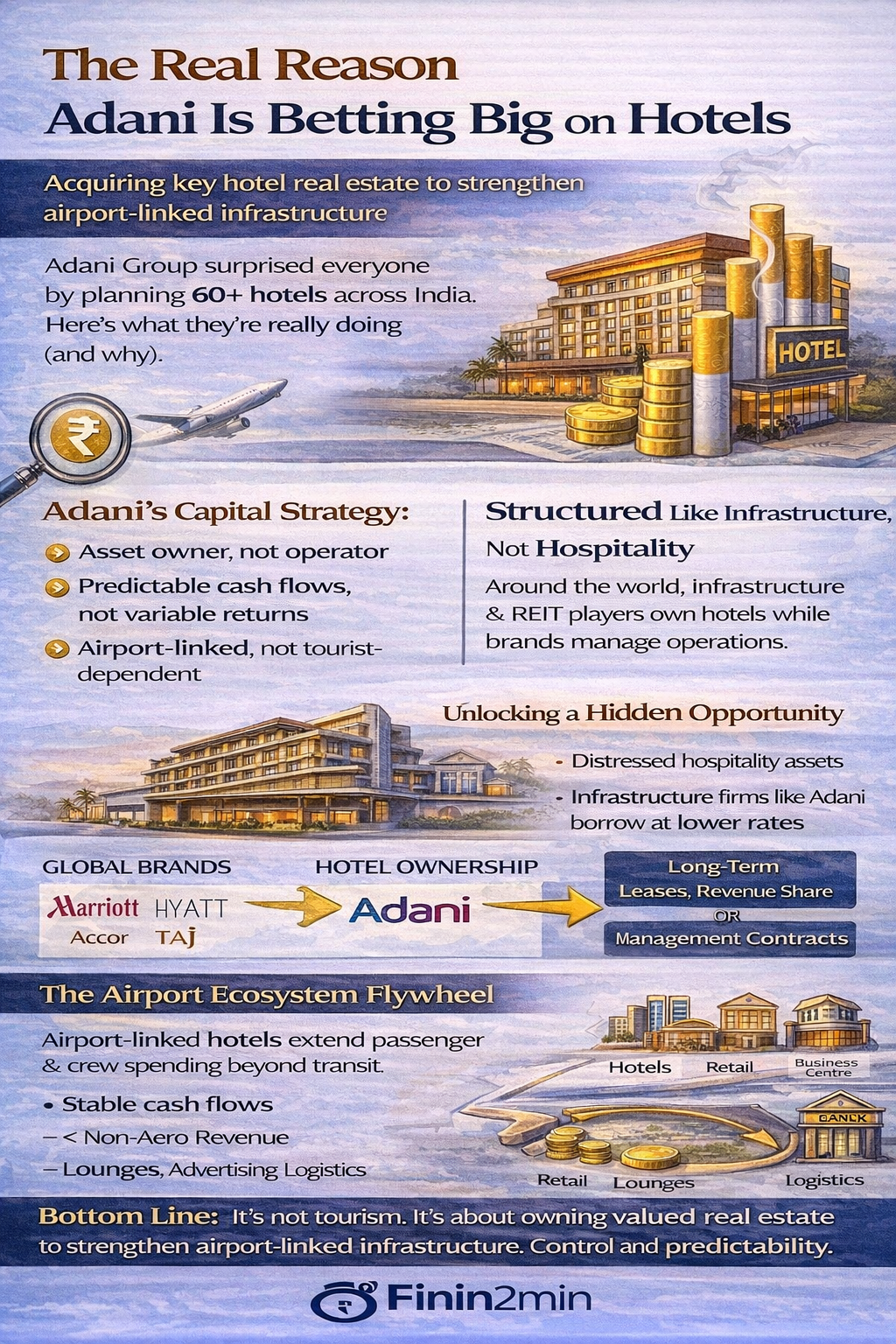

And yet, reports now say Adani plans to build and own more than 60 hotels across India.

Hotels are cyclical.

Hotels are labour-intensive.

Hotels bleed cash in downturns.

So why step in?

The short answer: Adani isn’t chasing hotel profits. It’s chasing predictability.

The Puzzle: Why Adani Avoids Airlines but Likes Hotels

Let’s start with what Adani clearly doesn’t want.

Despite owning multiple airports, training infrastructure, and aviation-adjacent assets, the group has categorically ruled out launching an airline.

That stance was reinforced publicly when Adani Airports leadership explained that:

- airline margins are structurally thin

- returns are unpredictable

- capital risk is disproportionate to upside

Airlines are operationally complex businesses where:

- fuel costs swing violently

- pricing power is limited

- competition destroys returns

From an infrastructure investor’s lens, aviation operations fail the test.

So why does hospitality pass?

Because Adani Is Not Building a Hotel Company

Here’s the key shift in perspective:

Adani is not entering hospitality.

It is expanding its infrastructure footprint using hospitality assets.

That distinction matters.

Adani doesn’t plan to:

- run front desks

- manage staff

- handle occupancy volatility

- build a hotel brand

Instead, it wants to own hotel real estate, especially in strategic locations, and let others do the hard work.

The Asset-Owner Playbook (Already Proven)

Globally, this model is well established.

In markets like the US, Middle East, and Singapore:

- REITs and infrastructure groups own hotels

- Global brands operate them

- Asset owners earn stable returns via leases, revenue share, or management contracts

India has quietly moved in the same direction.

Large institutional investors increasingly prefer:

- owning hospitality assets

- while outsourcing operations to brands like Marriott, Accor, Hyatt, or IHCL

Why?

Because the risk-return profile improves dramatically.

Where Adani Fits In

Adani’s strength has never been running consumer businesses.

Its edge lies in:

- land acquisition

- financing at scale

- long-duration assets

- regulatory navigation

- ecosystem building

Hotels—when viewed as real estate plus annuity cash flows—fit that playbook neatly.

Especially when they are:

- airport-adjacent

- business-focused

- conference-oriented

- crew-driven

These hotels are less dependent on tourism cycles and more aligned with infrastructure demand.

Distressed Assets Are the Hidden Opportunity

Another reason the timing makes sense: India is full of stressed hospitality assets.

Many hotels in India:

- were built with expensive debt

- struggle during low occupancy phases

- face refinancing challenges

Infrastructure groups like Adani enjoy:

- lower cost of capital

- access to long-tenure funding

- stronger lender confidence

If Adani acquires or develops hotel assets and classifies them as infrastructure-linked real estate, it can:

- refinance high-cost hotel debt

- lower interest burden materially

- improve asset viability without changing operations

This is classic balance-sheet arbitrage.

This Is Really an Airport Story

The hotel push is not a standalone bet.

It sits squarely inside Adani Airport Holdings Limited (AAHL).

And that’s the clue.

Airports globally are no longer valued just on:

- passenger footfalls

- landing fees

They are valued on non-aeronautical monetisation.

That includes:

- retail

- lounges

- advertising

- business centres

- hotels

- convention infrastructure

Hotels next to airports:

- extend passenger spend beyond transit

- attract airline crews

- anchor conferences and exhibitions

- stabilise cash flows independent of flight cycles

In short, they make airport earnings more predictable.

Completing the Ecosystem

Seen through this lens, several Adani moves line up:

- Expansion of airport-linked real estate

- Plans for large convention and exhibition centres

- Focus on logistics, cargo, and infrastructure finance

Together, they create economic clusters around airports, not just terminals.

For a future AAHL listing, that story is far more compelling than runways alone.

Why This Fits Adani’s Capital Strategy

Adani’s core investment logic is consistent across sectors:

- Own the asset

- Control the ecosystem

- Minimise operational exposure

- Monetise long-term demand

Hotels—when structured correctly—are infrastructure assets in disguise.

They generate:

- stable lease income

- predictable cash flows

- appreciation in land value

- optional upside via revenue share

All without day-to-day execution risk.

The Clever Part

Adani gets:

- exposure to hospitality upside

- airport monetisation benefits

- refinancing advantages

- IPO-ready diversification

Without:

- running a hotel

- hiring hotel staff

- managing occupancy cycles

That’s not hospitality expansion.

That’s infrastructure optimisation.

Finin2min Bottom Line

Adani’s hotel strategy isn’t about tourism, luxury, or room rates.

It’s about:

- owning strategic real estate

- strengthening airport economics

- building predictable cash flows

- and telling a stronger infrastructure growth story

All while letting someone else handle the operational grind.

Control without operations.

Returns without running the business.

That’s the Adani way.

Disclaimer: This article is for informational and educational purposes only and does not constitute investment advice, a recommendation, or an offer to buy or sell any securities. Views expressed are based on publicly available information and personal analysis as of the date of publication. Readers should conduct their own research or consult a qualified financial advisor before making any investment decisions.