India’s tax system has undergone a major digital transformation in the last three decades — and at the center of this modernization are two identifiers:

PAN (Permanent Account Number) and TAN (Tax Deduction and Collection Account Number).

These unique alphanumeric codes connect taxpayers to their financial and tax records, ensuring transparency and traceability across India’s vast economy.

1️⃣ The Birth of PAN — A Digital Tax Identity

Before PAN was introduced, taxpayers were identified manually through local Income Tax offices — a process prone to duplication and corruption.

The Need for a Unified Code

In the early 1970s, as the number of taxpayers increased, the CBDT (Central Board of Direct Taxes) realized the necessity of a nationwide identification system for individuals and businesses.

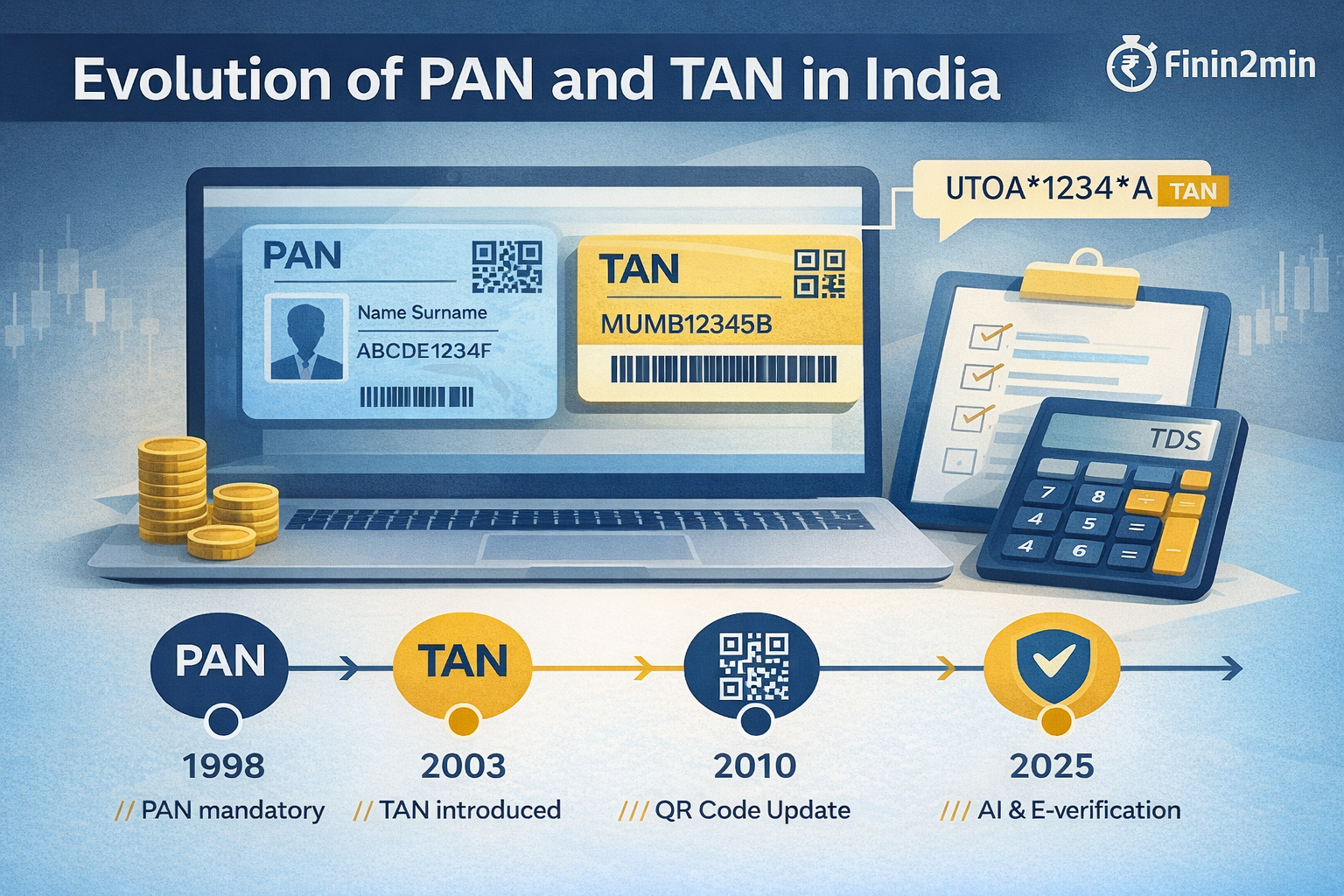

Hence, in 1972, a rudimentary system was introduced, later replaced by a modern, computer-based PAN in 1995.

2️⃣ What is PAN (Permanent Account Number)?

PAN is a 10-character alphanumeric code issued by the Income Tax Department under Section 139A of the Income-tax Act, 1961.

Format Example:

👉 ABCDE1234F

| Character | Meaning |

|---|---|

| 1–5 | Alphabetic (Name/Entity Type) |

| 6–9 | Numeric (Unique Code) |

| 10 | Alphabet (Check digit) |

Issued By:

NSDL (Now Protean eGov Technologies) and UTIITSL, authorized by the CBDT.

3️⃣ Why PAN Matters

PAN acts as a universal financial identity for both individuals and companies.

It is mandatory for almost all major financial transactions, including:

- Filing income tax returns

- Opening a bank account

- Buying property above ₹10 lakh

- Investing in shares, mutual funds, or gold

- Registering a business

- High-value cash deposits (₹50,000+)

Linking with Aadhaar

As per Section 139AA, linking PAN with Aadhaar is mandatory for it to remain active.

Unlinked PANs are considered inoperative from July 1, 2023.

4️⃣ Digital Evolution of PAN

Over the years, PAN has transformed into a fully digital, paperless ID:

Key Milestones:

| Year | Change | Impact |

|---|---|---|

| 1995 | Computerized PAN system | Reduced duplication |

| 2003 | Online PAN application via NSDL | Nationwide accessibility |

| 2017 | PAN–Aadhaar linking | Single national ID |

| 2020 | Instant e-PAN using Aadhaar e-KYC | 10-minute issuance |

| 2022 | PAN–GST–CIN integration | Unified business identity |

Current Status (2025):

Over 70 crore PANs issued, with 97% Aadhaar linkage rate (CBDT data).

5️⃣ TAN — Tax Deduction and Collection Account Number

While PAN is universal, TAN is specifically for those who deduct or collect tax at source (TDS/TCS).

Legal Basis:

- Introduced under Section 203A of the Income-tax Act, 1961

- Issued by Income Tax Department through NSDL

TAN Format Example:

👉 DELX12345B

| Character | Meaning |

|---|---|

| 1–4 | City/Office code |

| 5–9 | Unique number |

| 10 | Alphabet check digit |

6️⃣ Why TAN is Crucial

Every person responsible for deducting tax at source (TDS) or collecting tax (TCS) must quote their TAN in:

- TDS/TCS returns

- Certificates issued to deductees

- Challans for tax payment

- Correspondence with the Income Tax Department

Without a TAN, TDS returns cannot be filed — and penalties apply under Section 272BB.

7️⃣ PAN vs TAN — Key Differences

| Basis | PAN | TAN |

|---|---|---|

| Meaning | Permanent Account Number | Tax Deduction/Collection Account Number |

| Purpose | Universal financial ID | For TDS/TCS activities |

| Who Needs It | Every taxpayer | TDS deductors only |

| Governing Section | 139A | 203A |

| Issued By | NSDL/UTIITSL | NSDL |

| Link to Aadhaar | Mandatory | Not applicable |

8️⃣ Integration with TIN and GST

The Indian government created a Tax Information Network (TIN) to connect PAN, TAN, and other tax identifiers.

Key Integrations:

- TIN 2.0 Portal (launched by CBDT)

- PAN–GSTIN linkage for businesses

- PAN-based login for AIS/TIS (comprehensive tax reporting)

These integrations ensure end-to-end transparency and reduce evasion by tracking high-value transactions.

9️⃣ Penalties and Compliance

| Offence | Relevant Section | Penalty |

|---|---|---|

| Failure to apply for PAN | 272B | ₹10,000 |

| Failure to quote PAN in transactions | 272B | ₹10,000 |

| Failure to obtain TAN | 272BB | ₹10,000 |

| Wrong or fake PAN/TAN usage | 277 | Prosecution possible |

🔟 The Future of PAN and TAN

The government plans to merge PAN, TAN, and GSTIN into a single business identifier for MSMEs and startups by 2026, improving ease of compliance.

Other futuristic upgrades include:

- API-based validation for fintechs

- Real-time e-verification of income sources

- AI-backed transaction monitoring

✅ Summary

Both PAN and TAN are the backbone of India’s income tax infrastructure.

While PAN provides identity, TAN ensures compliance. Their integration with Aadhaar, GST, and AI-driven systems has brought India closer to a fully digital tax regime.

💬 FAQs

1. Is PAN mandatory for all taxpayers?

Yes, every taxpayer earning taxable income must have a PAN.

2. Do individuals need TAN?

No, TAN is required only for entities deducting/collecting tax.

3. Can I get PAN instantly?

Yes, instant e-PAN is available via Aadhaar on the Income Tax portal.

4. Can a person have multiple PANs?

No, holding multiple PANs is illegal under Section 139A(7).

5. What is the validity of TAN?

TAN is valid for life unless the business is closed.

📚 References

- Income-tax Act, 1961

- Section 139A & 203A

- CBDT Notifications (2019–2024)

- NSDL & TIN 2.0 Portal

- Union Budget 2024–25