🗓️ Period: 9 Feb’26 → 15 Feb’26

(Markets • Macro • Commodities • Policy • Global • Strategy • Finin2min)

🧭 FININ2MIN MARKET REGIME SNAPSHOT

Market Regime: Range-bound Distribution → Selective Rotation

Finin2min Market Regime Score (FMRS™): 4.8 / 10 ↓

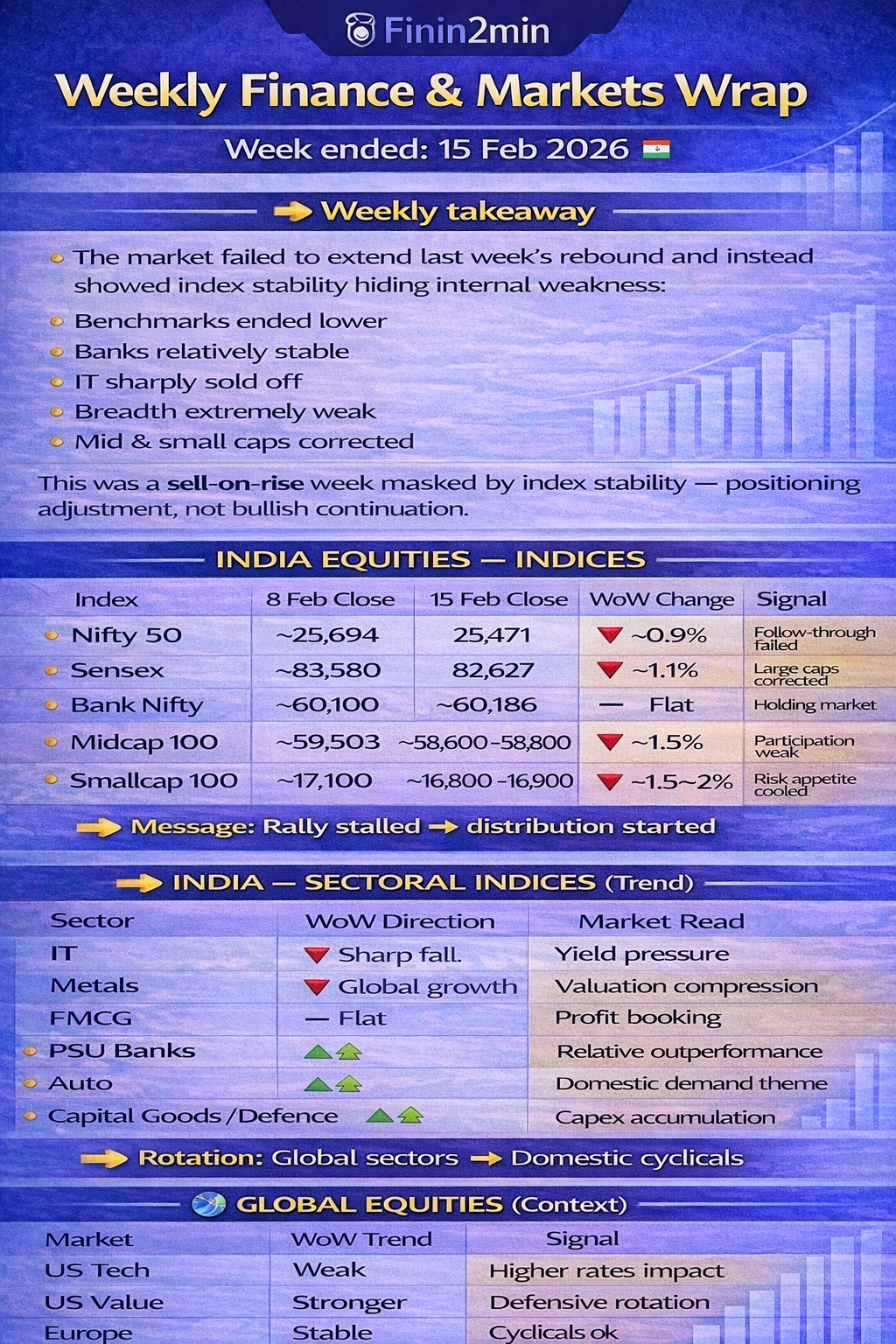

👉 Weekly takeaway

The market failed to extend last week’s rebound and instead showed index stability hiding internal weakness:

- Benchmarks ended lower

- Banks relatively stable

- IT sharply sold off

- Breadth extremely weak

- Mid & small caps corrected

This was a sell-on-rise week masked by index stability — positioning adjustment, not bullish continuation.

📊 FININ2MIN QUANT SCORECARD (FQSM™)

| Metric | Score | Interpretation | Market implication |

|---|---|---|---|

| Risk Sentiment Index | 4.6 / 10 ↓ | Risk appetite fading | Sell on rise |

| Liquidity Score | 4.7 / 10 → | Still tight | No broad rally |

| Trend Strength – India | 4.9 / 10 ↓ | Failed breakout | Range forming |

| Trend Strength – Global | 6.1 / 10 ↑ | Global stable | India lagging |

| Macro Stress Indicator | 6.5 / 10 ↑ | Volatility returning | Wider swings ahead |

📊 WEEK-TO-WEEK MARKET COMPARISON

🇮🇳 INDIA EQUITIES — INDICES

| Index | 8 Feb Close | 15 Feb Close | WoW Change | Signal |

|---|---|---|---|---|

| Nifty 50 | ~25,694 | 25,471 | 🔻 ~-0.9% | Follow-through failed |

| Sensex | ~83,580 | 82,627 | 🔻 ~-1.1% | Large caps corrected |

| Bank Nifty | ~60,100 | ~60,186 | ➖ Flat | Holding market |

| Midcap 100 | ~59,503 | ~58,600–58,800 | 🔻 ~-1.5% | Participation weak |

| Smallcap 100 | ~17,100 | ~16,800–16,900 | 🔻 ~-1.5–2% | Risk appetite cooled |

👉 Message: Rally stalled → distribution started

🏭 INDIA — SECTORAL INDICES (Trend)

| Sector | WoW Direction | Market Read |

|---|---|---|

| IT | 🔻 Sharp fall | Yield pressure |

| Metals | 🔻 | Global growth doubts |

| FMCG | 🔻 | Valuation compression |

| Private Banks | ➖/🔻 | Profit booking |

| PSU Banks | 🔼 | Relative outperformance |

| Auto | 🔼 | Domestic demand theme |

| Capital Goods / Defence | 🔼 | Capex accumulation |

👉 Rotation: Global sectors → Domestic cyclicals

🪙 COMMODITIES

| Asset | 8 Feb | 15 Feb | WoW | Interpretation |

|---|---|---|---|---|

| Gold (INR/10g) | ~₹1.56L | ~₹1.60–1.63L | 🔼 | Defensive demand |

| Silver (MCX/kg) | ~₹2.50L | ~₹2.45–2.60L | ➖ Volatile | Stress stabilising |

| Brent Oil | ~$70–71 | ~$68–72 | ➖ | Inflation uncertainty |

| Metal | 8 Feb | 15 Feb | WoW Move | % Move | Signal |

|---|

| Gold | ~4,890 | 5,041 | 🔼 +150 | ~+3.0% | Strong hedge demand |

| Silver | ~74.8 | 77.3 | 🔼 +2.5 | ~+3.3% | Recovery from liquidation |

Interpretation (Important)

- Gold rising with yields → geopolitical + policy uncertainty hedge

- Silver rising with gold (not alone) → not risk-on, but stress easing

- Metals confirming: markets defensive, not bearish panic

👉 Signal:

Capital moved to safety assets while equities distributed — classic late-cycle behaviour

💱 FX & RATES

| Asset | 8 Feb | 15 Feb | Trend | Signal |

|---|---|---|---|---|

| USD/INR | ~90.7 | ~90.5–90.7 | ➖ | Stable currency |

| India 10Y | ~6.71% | ~6.7% | ➖ | No easing pricing |

| US 10Y | ~4.05% | ~4.15% | 🔼 | Higher-for-longer |

🧠 WEEK-TO-WEEK INTERPRETATION

Week 1 (ending 8 Feb): Stabilisation rally

Week 2 (ending 15 Feb): Distribution & rotation

Markets did not reverse trend —

they absorbed supply after rebound

Key change:

➡️ Liquidity didn’t leave

➡️ But risk appetite narrowed

Finin2min takeaway:

Market shifted from recovery → positioning adjustment

🏭 SECTOR ROTATION — THE REAL STORY

Relatively Strong

- Autos

- PSU Banks

- Defence & capex

- Select domestic cyclicals

Weak

- IT (major drag)

- Metals

- FMCG valuation names

- Some private financials

👉 Money moved from global growth → domestic earnings visibility

🌍 GLOBAL MARKETS

| Region | Trend | Driver |

|---|---|---|

| US | Tech weak | Rising yields |

| Europe | Stable | Value rotation |

| Asia | Stronger | China stimulus hopes |

| Japan | Strong | Policy + weak yen |

👉 India lagged broader Asia

💱 RATES, VOL & FLOWS

| Indicator | Weekly Read | Signal |

|---|---|---|

| India VIX ~13.3 ↑ | Volatility rising | Market cautious |

| US 10Y Yield ↑ | Higher-for-longer | IT pressure |

| FPI flows | Choppy but net positive | Selective buying |

| DII flows | Supportive | Prevents sharp fall |

| USD/INR ~90.5–90.7 | Stable | External anchor |

📌 FPI flows: ~₹11,600 Cr net equity inflows in Feb MTD

🪙 COMMODITIES & MACRO SIGNALS

- Gold firm → defensive positioning

- Silver volatile after earlier crash

- Oil mid-$60s–$70 range → inflation uncertainty

- Dollar stable-firm → EM capped

- Rising yields → growth stock derating

2️⃣ MACRO & FLOWS — KEY SIGNALS

Risk Sentiment

Institutions reduced beta exposure rather than exiting risk:

- Selling rallies

- Buying selective cyclicals

- Avoiding global growth sectors

Global Macro Read

- US CPI: 2.4% headline, 2.6% core

- Disinflation intact but sticky components remain

- Fed cuts delayed, not cancelled

👉 Markets repricing valuations, not earnings collapse

3️⃣ POLICY & GEOPOLITICAL HIGHLIGHTS

🇮🇳 India–US Trade Deal (9 Feb)

Historic agreement announced with phased tariff reductions and market access expansion.

Impact

- Export visibility improves (textiles, pharma, autos)

- Supported return of foreign flows

👉 Positive structural signal amid short-term volatility

🇮🇳 RBI Policy & Liquidity

- Repo: 5.25% unchanged

- FY26 GDP: 7.4%

- Inflation: ~2.1%

- Active FX management near ₹90–91

Impact:

Supports banks • caps valuations • keeps market range-bound

🌏 Global Geopolitics

- Russia–China energy dynamics monitored

- Japan policy shift supportive for equities

- No major escalation in major conflicts during week

🛢 Energy & Inflation

- Oil stable but not falling

→ Delays global rate cuts

🏗️ India Growth & Structural Signals

- Fastest-growing G20 economy retained

- Manufacturing & formalisation boosting tax collections

- Government signalling vertical real-estate expansion near airports

👉 Domestic growth cycle intact

5️⃣ SECTOR & CORPORATE THEMES — INDIA

Accumulation

- PSU banks

- Defence & manufacturing

- Autos & domestic cyclicals

Profit-booking

- IT & export plays

- Metals

- Premium defensives

👉 Institutions favour earnings certainty over global growth sensitivity

⚠️ KEY RISKS

- Rising US yields

- IT earnings downgrades

- Narrow leadership

- Weak breadth

- Elevated retail positioning

👀 NEXT WEEK WATCHLIST

- Bond yield direction

- Breadth recovery

- Bank Nifty support

- IT stabilisation

- FPI participation

🧠 FININ2MIN STRATEGY SIGNAL

➡️ Avoid index chasing

➡️ Prefer domestic cyclicals & PSU themes

➡️ Avoid weak global sectors

➡️ Expect volatility expansion

➡️ Stock picking > beta

🧭 FININ2MIN BOTTOM LINE

The rally is not broad — it is rotational.

Banks are holding indices,

but participation is weakening underneath.

Market is in a positioning adjustment phase before next trend.

Current market drivers

- US bond yields

- INR stability

- Domestic capex cycle

Until global rates cool →

Expect range + rotation, not breakout

Finin2min — insight for discussion, not investment advice.