📅 FY27 | Presented & Introduced: 1 Feb 2026 | Lok Sabha | Finin2min Summary

🎯 Objective: Implement Budget 2026-27 proposals while preserving macro stability and accelerating structural reforms

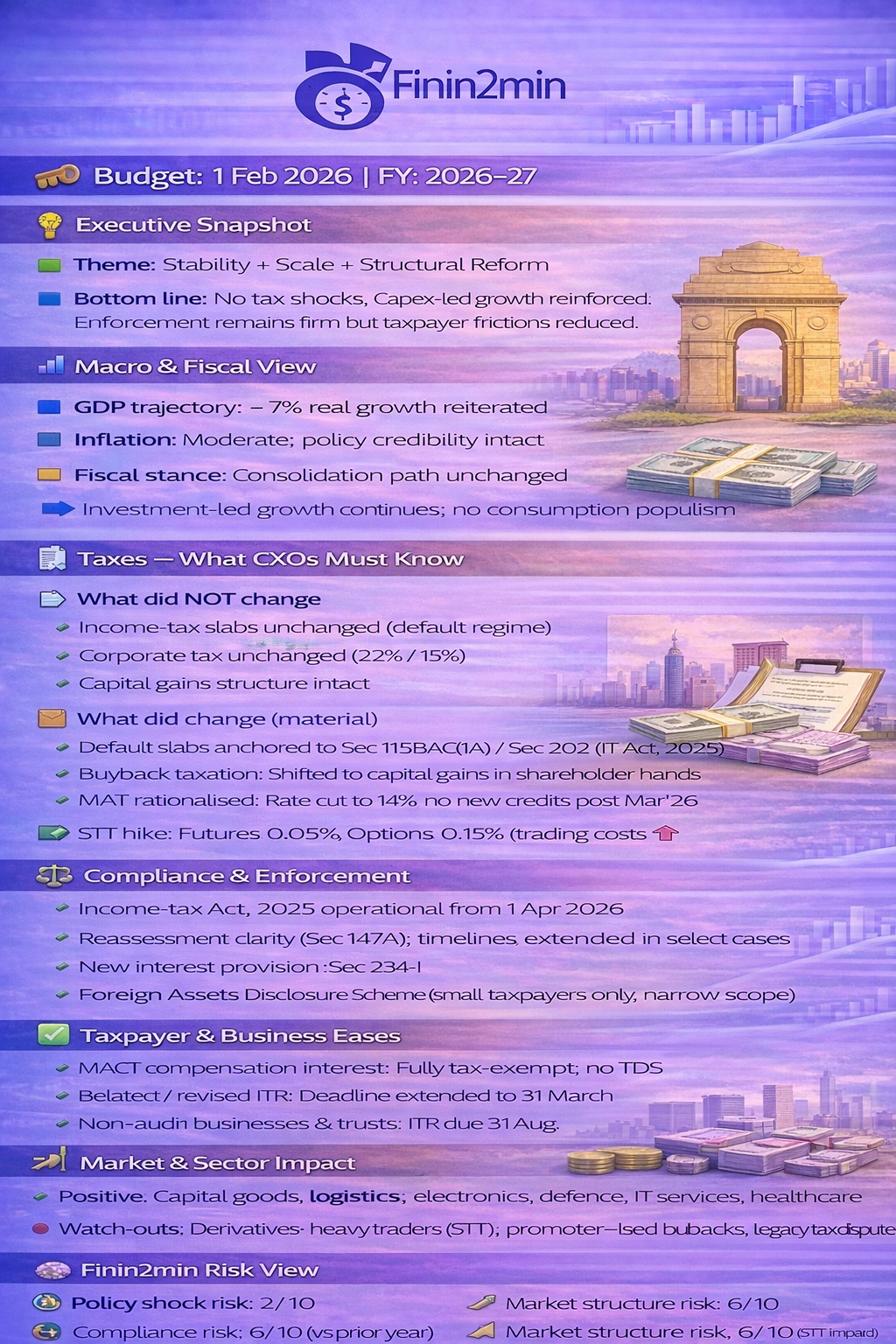

🔑 Big Picture (Executive Summary)

Theme: Stability + Scale + Structural Reform

- No tax shocks for individuals, corporates or markets

- Capex-led growth model reinforced

- Manufacturing + Services positioned as twin engines

- Compliance intensity remains high, but administrative frictions eased

➡️ Net effect: Policy continuity with selective taxpayer relief; enforcement still data-driven

1️⃣ Fiscal & Macro Framework

- Growth: ~7% real GDP trajectory reiterated

- Inflation: Moderate; monetary stability acknowledged

- Fiscal discipline: Consolidation path unchanged

- Public Capex: ₹12.2 lakh crore (↑ from ₹11.2 lakh crore)

➡️ Interpretation: Investment-led growth continues to dominate fiscal strategy

2️⃣ Income-Tax Rates — Status Quo Maintained

- No change in individual or corporate tax slabs

- Default personal taxation anchored to:

- Section 115BAC(1A) — Income-tax Act, 1961 (AY 2026-27)

- Section 202 — Income-tax Act, 2025 (Tax Year 2026-27)

- Banded slab structure (default):

- Nil tax up to ₹4 lakh

- Progressive slabs up to 30% beyond ₹24 lakh

- Surcharge structure unchanged

- Capital-gains surcharge capped at 15%

- Health & Education Cess: 4%

➡️ Signal: Legislative continuity with clean migration to Act-2025 framework

3️⃣ Major Structural Shift — Income-tax Act, 2025

- Act, 2025 operationalised from 1 April 2026

- 1961 Act retained only for legacy matters

- Re-numbered sections, simplified drafting, digital-first processes

➡️ Impact: Long-term simplification; short-term transition load for systems & advisors

4️⃣ Tougher Compliance & Enforcement Framework

- Section 147A clarified:

- Jurisdiction with Assessing Officer, not faceless centres

- Certain provisions retrospective to 1 April 2021

- Time-limit clarifications & extensions:

- Sections 153 / 153B / 144C / 275 / 286

- Some block assessments extended to 18 months

- New interest provision — Section 234-I

- Sharper action on TDS/TCS defaults

- Reduced discretionary penalty relief

➡️ Signal: Enforcement remains strong, but process clarity improves

5️⃣ NEW — Taxpayer Relief & Compliance Eases

(Important counter-balance to enforcement narrative)

✅ Relief Measures

- MACT compensation interest:

- Fully exempt from income tax

- No TDS required

Targeted relief for accident victims

- Revised / Belated ITR timeline eased:

- Filing allowed till 31 March (earlier: 31 Dec)

- Fees capped at:

- ₹1,000 (income ≤ ₹5 lakh)

- ₹5,000 (income > ₹5 lakh)

- Non-audit business cases & trusts: deadline extended to 31 August

- ITR-1 / ITR-2 unchanged at 31 July

- TAN relief:

- No TAN required for resident Individuals / HUFs purchasing immovable property from non-residents

- PAN-based TDS compliance allowed

➡️ Impact: Reduced friction for small taxpayers & genuine transactions

6️⃣ Foreign Assets Disclosure Scheme, 2026

- One-time window for small taxpayers

- Fixed tax + penalty

- Immunity from prosecution

- No reopening of completed assessments

- Payments non-refundable

- Excludes proceeds of crime & PMLA / Black Money Act cases

➡️ Positioning: Narrow compliance window, not a broad amnesty

7️⃣ Capital Gains, Buybacks & Corporate Taxes

Capital Gains

- 15% surcharge cap retained

- No adverse changes to equity LTCG / STCG or dividends

🔄 Buyback Taxation (Major Change)

- Buybacks now taxed as capital gains in shareholder hands

- No longer treated as dividend distribution

- Effective tax impact:

- Promoters (corporate): ~22%

- Others (individuals / non-corporate): up to 30%

➡️ Impact: Discourages promoter-heavy buybacks; nudges dividend discipline

8️⃣ MAT & Corporate Regime Rationalisation

- MAT reduced to 14% (final tax)

- No fresh MAT credits post March 2026

- Legacy MAT credit set-off restricted:

- 1/4th usable under new domestic regime

➡️ Signal: Simplification + gradual sunset of parallel tax systems

9️⃣ TCS & STT Rationalisation

📌 TCS Rate Changes (Uniformisation Push)

| Item | Old Rate | New Rate |

|---|---|---|

| Alcoholic liquor, scrap, minerals (coal/lignite/iron ore) | 1% | 2% |

| Tendu leaves | 5% | 2% |

| LRS – education/medical (>₹10L) | 5% | 2% |

| LRS – other remittances | 20% | Unchanged |

| Overseas tour packages | 5% / 20% | 2% (no threshold) |

➡️ Effect: Lower friction, better cash-flow predictability

📈 STT Changes (Market-side)

- Futures: 0.02% → 0.05%

- Options (premium & exercise): → 0.15%

➡️ Intent: Curb excessive F&O speculation

🔟 Manufacturing, MSMEs, Services, Infra & Finance

(Unchanged in substance — summarised for continuity)

- Manufacturing: Semiconductors, electronics, rare earths, biopharma, textiles, capital goods

- MSMEs: ₹10,000 cr Growth Fund, TReDS mandate, CGTMSE backing, Corporate Mitras

- Services: Medical tourism hubs, IT safe harbour (15.5%), cloud/data-centre tax holiday till 2047

- Infrastructure: ₹12.2 lakh cr capex, freight corridors, waterways, CERs

- Finance: Bond market making, PFC/REC restructuring, Banking HLC

🧠 Updated Finin2min Risk Matrix

- Policy shock risk: 2 / 10

- Compliance / litigation risk: 6 / 10 (↓ due to taxpayer eases)

- Market structure risk: 6 / 10 (↑ due to STT impact on derivatives)

🧮 Finin2min Verdict

Budget + Finance Bill 2026 is not loud — it is deliberate.

- 📈 Growth-positive

- 🧱 Structurally reformist

- ⚖️ Balanced enforcement with targeted relief

- 🗳️ Non-populist

Finin2min Macro Scorecard

- Growth Visibility: 8 / 10

- Fiscal Prudence: 8 / 10

- Market Friendliness: 7.5 / 10

- Compliance Stress: 6.5 / 10

This analysis summarizes Budget 2026 highlights for informational purposes only. Not tax/financial advice. Consult your advisor. Subject to final enactment.