0.05% / 0.1% Route Explained — Finin2min Playbook

Law • GST • Exports • Compliance • Risk Management

Practical | Supplier-first | Audit-ready | FY 2025–26

1️⃣ What This Scheme Is — and What It Is NOT

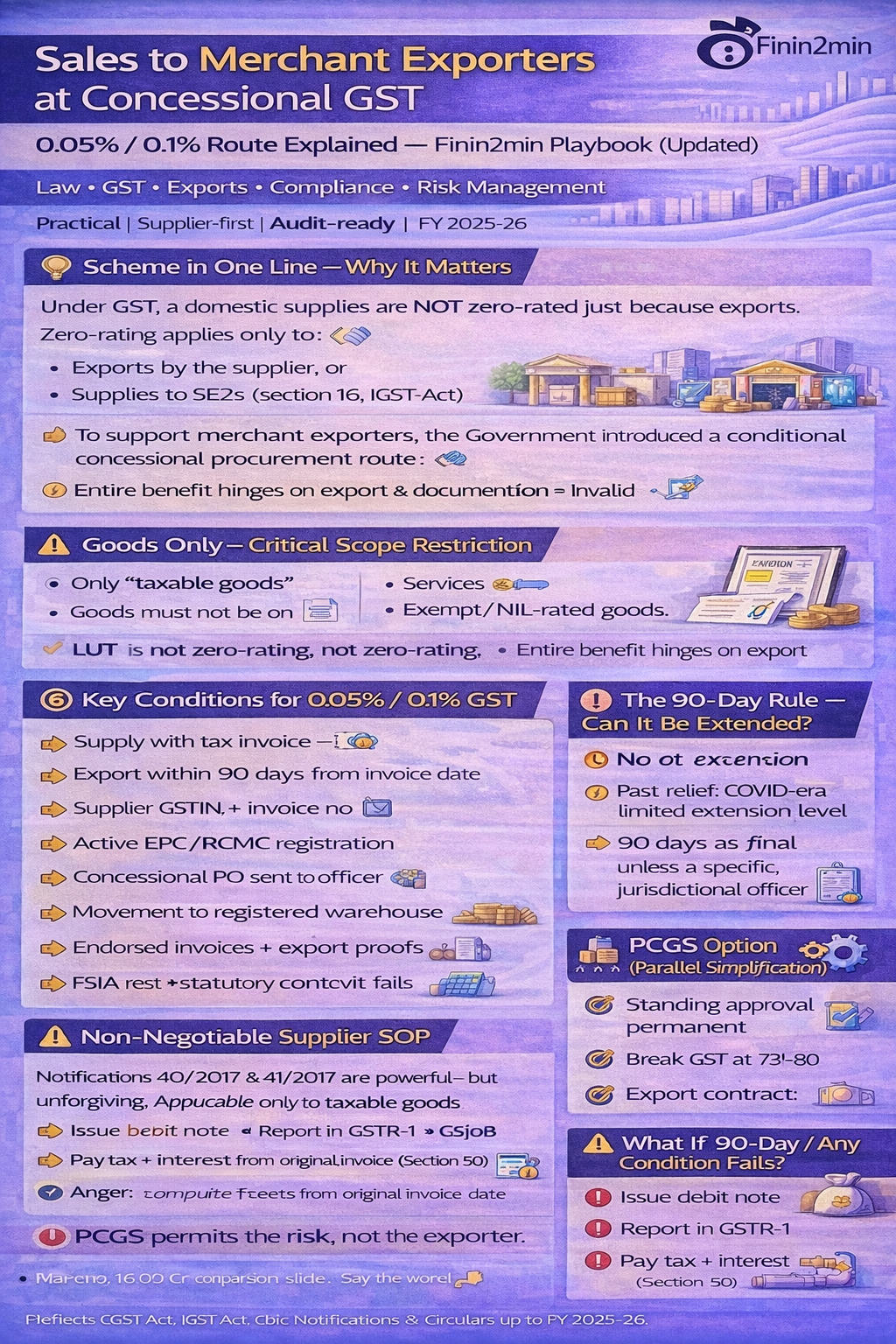

Under GST, a domestic supply does not become zero-rated merely because the buyer exports.

Zero-rating applies only to:

- Exports by the supplier, or

- Supplies to SEZ (Section 16, IGST Act)

To support merchant exporters, the Government introduced a conditional concessional procurement route:

| Nature of Supply | Notification | GST Rate |

|---|---|---|

| Intra-State | 40/2017-CT (Rate) | 0.05% CGST + 0.05% SGST/UTGST |

| Inter-State | 41/2017-IGST (Rate) | 0.1% IGST |

📌 This is a partial exemption, not zero-rating

📌 Entire benefit hinges on export performance + documentation

2️⃣ Scope Restriction — GOODS ONLY (Critical & Often Missed)

✔ What is covered

- Only “taxable goods”

- Goods must not be exempt or NIL-rated

- Supplier must verify HSN eligibility

❌ What is NOT covered

- Services — completely excluded

- Exempt / NIL-rated goods

- Non-taxable supplies

📌 Notifications 40/2017 & 41/2017 are explicitly limited to goods

📌 Any attempt to apply concessional rate to services = invalid

3️⃣ Legal Nature of the Notifications

Both notifications:

- Exempt GST only to the extent it exceeds 0.05% / 0.1%

- Are conditional exemptions

- Fail automatically if export conditions are breached

🚫 If export fails → exemption fails → supplier liability revives

4️⃣ Eligibility Gate Checks (Before Issuing Invoice)

Supplier

✔ Registered GST person

✔ Making taxable supply of goods

Merchant Exporter (Recipient)

✔ Registered GST person

✔ Registered with Export Promotion Council / Commodity Board (RCMC)

✔ Exports under LUT (Rule 96A)

📌 Supplier should retain:

- GST registration copy

- EPC/RCMC

- LUT copy (best practice)

5️⃣ Mandatory Conditions (i)–(ix) — Consolidated & Explained

| Condition | Legal Requirement | Practical Risk |

|---|---|---|

| (i) Tax Invoice | Must issue tax invoice | No bill of supply |

| (ii) Export in 90 days | From supplier invoice date | Absolute timeline |

| (iii) Shipping Bill Link | Supplier GSTIN + invoice no. | Most litigated |

| (iv) EPC/RCMC | Mandatory | Keep on record |

| (v) Procurement Order | PO + copy to supplier’s officer | Often missed |

| (vi) Movement Route | Direct port OR registered warehouse | No deviation |

| (vii) Aggregation | Multi-supplier → warehouse mandatory | Common failure |

| (viii) Warehouse Proof | Endorsed invoice + ack | Must share |

| (ix) Post-export Proof | SB + EGM proof to supplier & officer | Closes loop |

6️⃣ Warehouse Rule — More Than Just GST Registration

Where aggregation is involved:

- Warehouse must be registered

- Preferably customs-bonded / notified

- Non-compliant warehouse = exemption void

📌 This is derived from the movement conditions of the notification and reinforced in departmental audits.

7️⃣ LUT / Bond — Exporter Obligation, Supplier Impact

Merchant exporter must:

- Export under LUT (Rule 96A)

- Bond only if LUT not permitted

📌 LUT is not mentioned in 40/41

📌 But without valid LUT, export itself becomes questionable → supplier risk

8️⃣ The 90-Day Export Rule — Any Extension?

General Rule

- No automatic extension

- 90 days = strict statutory condition

Exceptional Past Relief

- COVID-era relaxations allowed Commissioner-level condonation

- No standing relaxation exists today

📌 Any extension must be:

- Specific

- Written

- Jurisdiction-approved

9️⃣ What If Conditions Fail? (Supplier Fallout)

If export not completed in 90 days or any condition fails:

Supplier must:

- Issue debit note for differential GST

- Report in GSTR-1

- Pay tax + interest via GSTR-3B

- Recover tax contractually from exporter

🔟 Interest Computation (Often Misapplied)

- Interest payable under Section 50, CGST Act

- Computed from date of original invoice

- Rate as notified (monthly, not daily)

📌 Interest exposure can be significant — not just tax differential

1️⃣1️⃣ GSTR & Shipping Bill Reconciliation Reality

- Shipping bill data may auto-link with GST systems

- But supplier must still manually track:

- Shipping bill copy

- Invoice linkage

- EGM / export report filing

🚫 Auto-population ≠ compliance completion

1️⃣2️⃣ PCGS OPTION — Alternative Route (Post-2023, Valid)

Principal Commissioner-based General Approval Scheme

(As per CBIC Circular No. 199/11/2023-GST)

✔ Available for frequent / regular merchant exporter supplies

✔ Allows standing approval for concessional procurement

✔ Reduces per-transaction compliance burden

📌 Still requires:

- Export within 90 days

- Shipping bill linkage

- Documentation discipline

📌 This is an administrative facilitation, not a dilution of conditions

1️⃣3️⃣ ITC Accumulation & Refund (Supplier Impact)

Concessional output GST + normal input GST ⇒ ITC pile-up

Supplier may:

- Evaluate refund of accumulated ITC (where legally permitted)

- Strategically limit concessional supplies

1️⃣4️⃣ When NOT to Use This Scheme

Avoid concessional route where:

- Export timelines uncertain

- Exporter weak on documentation

- Warehouse routing unclear

- Supplier unwilling to monitor post-export compliance

📌 Normal GST + exporter refund is always permitted

🧠 Finin2min Final Takeaway

Notifications 40/2017 & 41/2017 are powerful — but unforgiving.

✔ Applicable only to taxable goods

✔ Export + documentation discipline is non-negotiable

✔ Supplier bears downstream risk

Use this route only with strong SOPs, indemnities, and tracking.

⚠️ Disclaimer

This article is based on CGST Act, IGST Act, CBIC Notifications, and Circulars as applicable up to FY 2025–26. Interpretations may vary by jurisdiction.

Article related to –

Sales to merchant exporters under GST

Concessional GST 0.05% 0.1%

Notification 40/2017 CT Rate explained

Notification 41/2017 IGST Rate explained

GST supply to merchant exporter without full tax

Merchant exporter GST conditions

90 days export rule GST

GST export via merchant exporter

Supplier risk under concessional GST

PCGS approval merchant exporter GSTSection 16 IGST Act zero-rated supply

Section 50 CGST Act interest computation

Rule 48 e-invoicing GST

Circular 37/11/2018-GST

Circular 199/11/2023-GST PCGS

GSTR-1 and GSTR-3B reconciliation

EGM proof GST export

LUT vs Bond GST export