(Before You Approach the Bank)

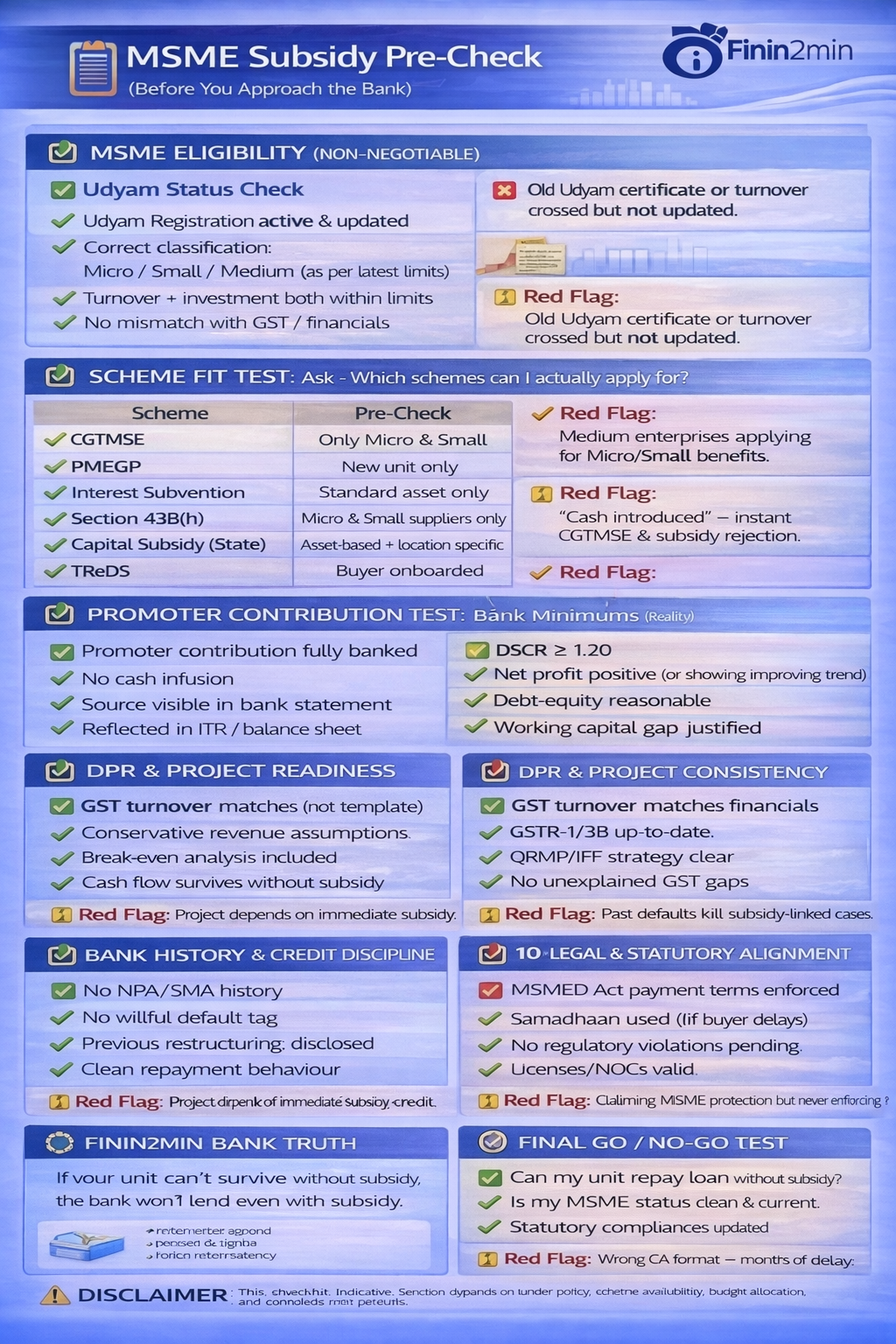

🧱 STEP 1 — MSME ELIGIBILITY (NON-NEGOTIABLE)

✅ Udyam Status Check

- Udyam Registration active & updated

- Correct classification:

- Micro / Small / Medium (as per latest limits)

- Turnover + investment both within limits

- No mismatch with GST / financials

🚫 Red Flag

Old Udyam certificate or turnover crossed but not updated.

🧾 STEP 2 — SCHEME FIT TEST

Ask: Which schemes can I actually apply for?

| Scheme | Pre-Check |

|---|---|

| CGTMSE | Only Micro & Small |

| PMEGP | New unit only |

| Interest Subvention | Standard asset only |

| Section 43B(h) | Micro & Small suppliers only |

| Capital Subsidy (State) | Asset-based + location specific |

| TReDS | Buyer onboarded |

🚫 Red Flag

Medium enterprises applying for Micro/Small benefits.

💰 STEP 3 — PROMOTER CONTRIBUTION TEST

- Promoter contribution fully banked

- No cash infusion

- Source visible in bank statement

- Reflected in ITR / balance sheet

🚫 Red Flag

“Cash introduced” → instant CGTMSE & subsidy rejection.

📊 STEP 4 — FINANCIAL VIABILITY CHECK

Bank Minimums (Reality)

- DSCR ≥ 1.20

- Net profit positive (or improving trend)

- Debt-equity reasonable

- Working capital gap justified

🚫 Red Flag

Assuming subsidy will fix weak cash flows.

📑 STEP 5 — DPR & PROJECT READINESS

- Project Report customised (not template)

- Conservative revenue assumptions

- Break-even analysis included

- Sensitivity (worst-case) scenario added

🚫 Red Flag

Copy-paste DPRs = silent rejection.

🧮 STEP 6 — GST & TURNOVER CONSISTENCY

- GST turnover matches financials

- GSTR-1 / 3B up to date

- QRMP/IFF strategy clear

- No unexplained GST gaps

🚫 Red Flag

GST data ≠ books → subsidy file stalled.

⏳ STEP 7 — TIMELINE AWARENESS

- Know scheme cut-off dates

- Asset installation timelines clear

- Subsidy credit lag (6–24 months) factored

- Cash flow survives without subsidy

🚫 Red Flag

Project depends on immediate subsidy credit.

🏦 STEP 8 — BANK HISTORY & CREDIT DISCIPLINE

- No NPA / SMA history

- No wilful default tag

- Previous restructuring disclosed

- Clean repayment behaviour

🚫 Red Flag

Past defaults kill subsidy-linked cases quietly.

🧾 STEP 9 — DOCUMENT HYGIENE CHECK

- Audited / provisional financials ready

- CA certificates in correct format

- Board resolutions (if company)

- Statutory compliances updated

🚫 Red Flag

Wrong CA format = months of delay.

⚖️ STEP 10 — LEGAL & STATUTORY ALIGNMENT

- MSMED Act payment terms enforced

- Samadhaan used (if buyer delays)

- No regulatory violations pending

- Licences / NOCs valid

🚫 Red Flag

Claiming MSME protection but never enforcing it.

🧠 FININ2MIN BANK TRUTH

If your unit can’t survive without subsidy,

the bank won’t lend even with subsidy.

Subsidies:

- Follow credit approval

- Reward discipline

- Punish inconsistency

✅ FINAL GO / NO-GO TEST

Ask yourself honestly:

- Can my unit repay loan without subsidy?

- Is my MSME status clean & current?

- Are all numbers bank-verifiable?

If YES → Approach bank confidently

If NO → Fix first, apply later

⚠️ DISCLAIMER

This checklist is indicative. Sanction depends on lender policy, scheme availability, budget allocation, and borrower risk profile.

Article related to –

MSME subsidies India 2025

MSME Checklist

MSME government schemes

MSME loan subsidy eligibility

MSME subsidy application process

MSME credit guarantee CGTMSE

MSME bank loan documents

MSME finance schemes India

MSME support schemes government

MSME subsidy checklist

MSME funding schemes India

How to apply for MSME subsidy in India

MSME subsidy eligibility criteria bank

Documents required for MSME loan subsidy

CGTMSE guarantee coverage explained

PMEGP subsidy calculation example

MSME export subsidy schemes India

MSME interest subvention scheme

Why MSME subsidy applications get rejected

MSME working capital government support

MSME compliance before bank loan

CGTMSE scheme details

PMEGP subsidy rules

Mudra loan eligibility

Stand-Up India scheme

Credit Linked Capital Subsidy Scheme (CLCSS)

MSME export credit support

MSME interest subvention

MSME Samadhaan delayed payment

TReDS MSME financing

DPIIT startup credit guarantee