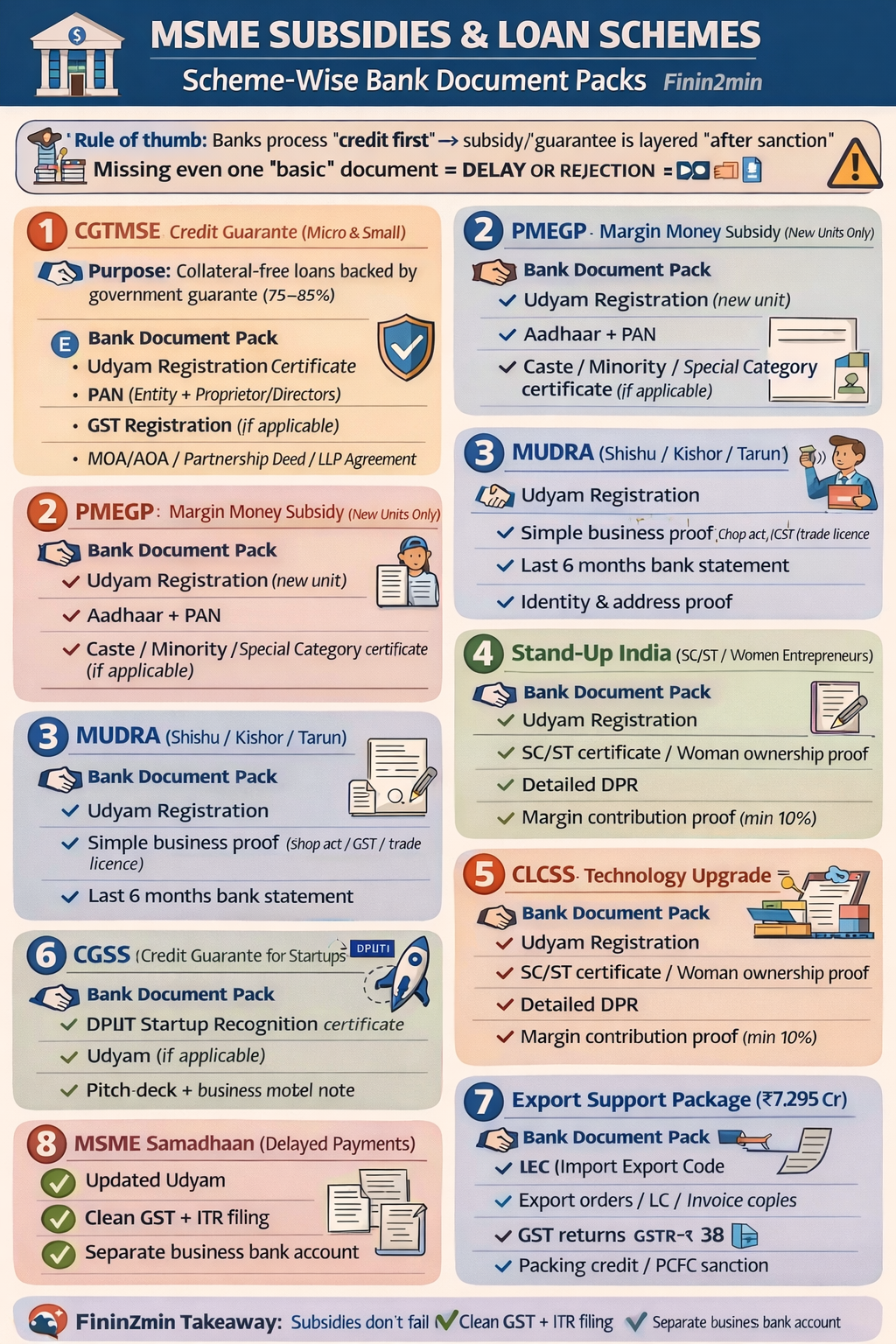

Scheme-Wise Bank Document Packs (Finin2min Playbook)

Rule of thumb: Banks process credit first → subsidy/guarantee is layered after sanction.

Missing even one “basic” document = delay or rejection.

1️⃣ CGTMSE — Credit Guarantee (Micro & Small Enterprises)

📌 Purpose

Collateral-free loans backed by government guarantee (75–85%).

📂 Bank Document Pack

Core Business Documents

- Udyam Registration Certificate

- PAN (Entity + Proprietor/Directors)

- GST Registration (if applicable)

- MOA/AOA / Partnership Deed / LLP Agreement

Financials

- Last 2–3 years ITRs (entity + promoters)

- Audited financials (or provisional, if new)

- Bank statements (last 6–12 months)

Credit Proposal

- Project report / cash-flow statement

- Loan application form (bank-specific)

- KYC of all promoters

CGTMSE-Specific

- Declaration for collateral-free loan

- Undertaking: no third-party guarantee

- Consent for CGTMSE fee debit

🔍 Common Bank Objection

“Promoter net worth not matching loan size”

➡ Fix by attaching personal balance sheet of promoters.

2️⃣ PMEGP — Margin Money Subsidy (New Units Only)

📌 Purpose

15–35% capital subsidy for new micro enterprises.

📂 Bank Document Pack

Eligibility Proof

- Udyam Registration (new unit)

- Aadhaar + PAN

- Caste / Minority / Special Category certificate (if applicable)

Project Documents

- Detailed Project Report (DPR)

- Cost break-up (land, building, machinery, WC)

- Quotations for machinery

Banking

- Bank account opening proof

- Sanction letter from financing bank

PMEGP-Specific

- KVIC / KVIB / DIC application acknowledgement

- Entrepreneur training completion certificate (EDP)

⏱ Timeline Reality

- Subsidy credited after unit setup + verification

- Lock-in: 3 years (cannot close unit)

3️⃣ MUDRA (Shishu / Kishor / Tarun)

📌 Purpose

Small-ticket, collateral-free business loans.

📂 Bank Document Pack

- Udyam Registration

- Simple business proof (shop act / GST / trade licence)

- Last 6 months bank statement

- Identity & address proof

⚠ Important

- No direct “subsidy”

- Treated as priority-sector lending

4️⃣ Stand-Up India (SC/ST / Women Entrepreneurs)

📌 Purpose

₹10 lakh–₹1 crore loans for greenfield units.

📂 Bank Document Pack

- Udyam Registration

- SC/ST certificate / Woman ownership proof

- Detailed DPR

- Margin contribution proof (min 10%)

- Land/lease documents (if applicable)

🔍 Bank Focus Area

“First-time entrepreneur viability”

➡ Strong cash-flow projections are critical.

5️⃣ CLCSS — Technology Upgrade Subsidy

📌 Purpose

15% capital subsidy (max ₹15 lakh) for eligible machinery.

📂 Bank Document Pack

- Udyam Registration (Micro/Small only)

- Machinery invoices (approved technology list)

- Term loan sanction letter

- CA certificate for asset capitalisation

⚠ Ground Reality

- Central CLCSS largely phased out

- State-level technology subsidies now more active

6️⃣ CGSS — Credit Guarantee for Startups (DPIIT)

📌 Purpose

Guarantee support for DPIIT-recognised startups.

📂 Bank Document Pack

- DPIIT Startup Recognition Certificate

- Udyam (if applicable)

- Pitch deck + business model note

- Bank sanction proposal

📌 Coverage

- Typically up to ₹5 crore per case

- Parallel to CGTMSE (not overlapping)

7️⃣ Export Support Package (₹7,295 Cr)

📌 Purpose

Interest subvention + risk support for MSME exporters.

📂 Bank Document Pack

- IEC (Import Export Code)

- Export orders / LC / invoice copies

- GST returns (GSTR-1, 3B)

- Packing credit / PCFC sanction

🧠 Tip

Banks prefer confirmed export orders, not projections.

8️⃣ MSME Samadhaan (Delayed Payments)

📌 Purpose

Recovery of dues beyond 45 days + statutory interest.

📂 Filing Pack

- Udyam Registration

- Invoices + delivery proof

- Agreement / PO

- Buyer details (PAN, GSTIN)

⚖ Award enforceable as civil decree

🔴 Why Banks Reject MSME Subsidy Claims (Reality Check)

❌ Udyam not updated (turnover/investment mismatch)

❌ Weak promoter ITR vs loan size

❌ No proper DPR / unrealistic projections

❌ GST non-compliance

❌ Past loan restructuring not disclosed

❌ Mixing personal & business bank accounts

✅ Finin2min Bank-Ready Checklist (One-Look)

✔ Updated Udyam

✔ Clean GST + ITR filing

✔ Separate business bank account

✔ DPR aligned with financials

✔ Promoter net worth documented

✔ Scheme-specific declarations ready

🧠 Finin2min Takeaway

Subsidies don’t fail because schemes are weak.

They fail because documentation is sloppy.

Banks lend to clarity + compliance, not to intent.

⚠️ DISCLAIMER

This article is based on validated statutory provisions, budget documents, scheme guidelines and judicial interpretation available up to FY 2025-26. Scheme terms may vary by lender, state policy or subsequent notification.

Article related to –

MSME subsidies India 2025

MSME government schemes

MSME loan subsidy eligibility

MSME subsidy application process

MSME credit guarantee CGTMSE

MSME bank loan documents

MSME finance schemes India

MSME support schemes government

MSME subsidy checklist

MSME funding schemes India

How to apply for MSME subsidy in India

MSME subsidy eligibility criteria bank

Documents required for MSME loan subsidy

CGTMSE guarantee coverage explained

PMEGP subsidy calculation example

MSME export subsidy schemes India

MSME interest subvention scheme

Why MSME subsidy applications get rejected

MSME working capital government support

MSME compliance before bank loan

CGTMSE scheme details

PMEGP subsidy rules

Mudra loan eligibility

Stand-Up India scheme

Credit Linked Capital Subsidy Scheme (CLCSS)

MSME export credit support

MSME interest subvention

MSME Samadhaan delayed payment

TReDS MSME financing

DPIIT startup credit guarantee