SC upholds Delhi HC (Aug 2025): Consolidated GST SCNs for multi-year fraud valid

Key ruling:

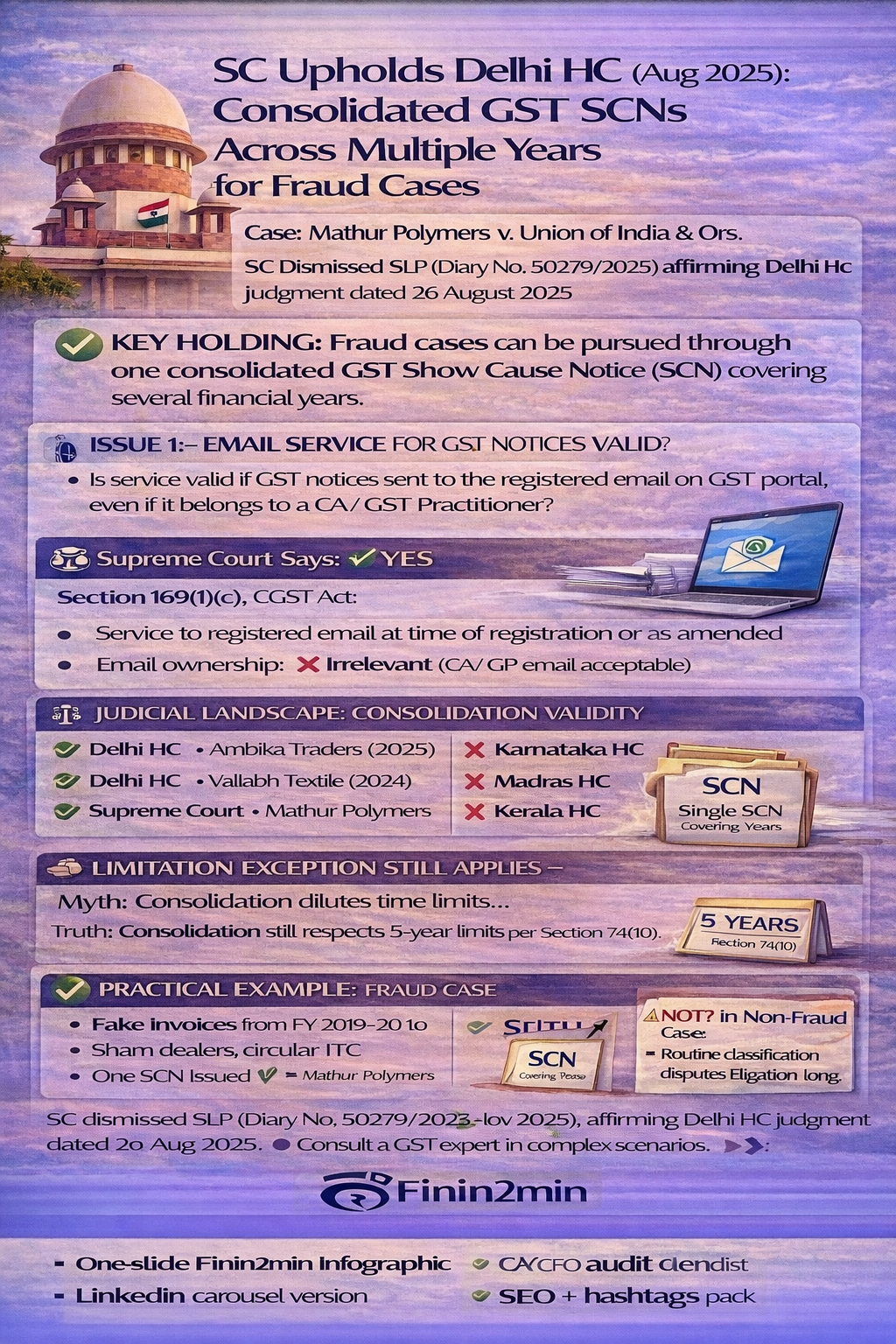

In fraud cases, one consolidated GST Show Cause Notice (SCN) covering multiple financial years is legally permissible, and email service to the registered GST portal address is valid — even if it belongs to a CA / GST Practitioner.

📌 CASE SNAPSHOT

| Particular | Details |

|---|---|

| Case | Mathur Polymers v. Union of India & Ors. |

| Court | Supreme Court of India |

| Date | SC upholds Delhi HC (Aug 2025) |

| Nature | Fraudulent ITC |

| Issue 1 | Validity of email service under GST |

| Issue 2 | Validity of consolidated SCN for multiple years |

| Outcome | Revenue succeeded; taxpayer’s SLP dismissed with costs |

🔍 ISSUE 1 — SERVICE OF GST NOTICE BY EMAIL

Question

Is service of GST notices valid if sent to the registered email on GST portal, even if it belongs to a CA / GST Practitioner?

Supreme Court’s Answer: YES

📜 Statutory Basis — Section 169(1)(c), CGST Act

| Provision | What it Allows |

|---|---|

| Section 169(1)(c) | Service by email to address provided at registration or as amended |

| Condition | Email must be the registered email on GST portal |

| Ownership of email | Irrelevant (CA / GP email acceptable) |

🧠 Court’s Reasoning (Simplified)

| Aspect | Court’s Finding |

|---|---|

| Registered email | Shown on GST portal |

| Taxpayer’s defence | Claimed no personal notice |

| Court’s view | Taxpayer withheld material facts |

| Natural justice | No violation |

| Income-tax precedents | Not applicable (different statutory language) |

📌 GST law focuses on “registered contact”, not “personal inbox”.

🔍 ISSUE 2 — CONSOLIDATED SCN FOR MULTIPLE YEARS

Question

Can the GST department issue one SCN covering several financial years in fraud cases?

Supreme Court’s Answer: YES — in fraud cases

🧩 WHY CONSOLIDATION IS LEGALLY PERMISSIBLE

📜 Statutory Language Matters

| Section | Key Words Used |

|---|---|

| Section 73 | “for any period” |

| Section 74 | “for such periods” |

| Missing phrase | ❌ “financial year–wise only” |

➡️ No statutory bar on multi-year consolidation where fraud spans years.

🧠 Core Logic Endorsed by SC

Fraud is rarely isolated to one year.

Authorities must examine patterns, modus operandi, and continuity.

📊 CONSOLIDATED SCN — WHEN VALID vs NOT

✅ Permissible (As per SC / Delhi HC)

| Scenario | Status |

|---|---|

| Fraudulent ITC across years | ✔ Allowed |

| Same modus operandi | ✔ Allowed |

| Common investigation | ✔ Allowed |

| Section 74 (fraud) invoked | ✔ Allowed |

❌ Disputed / Not Permissible (Some HCs)

| Scenario | Concern Raised |

|---|---|

| Non-fraud demands | ❌ |

| Year-wise limitation prejudice | ❌ |

| Rule 142 procedural issues | ❌ |

⚖️ JUDICIAL LANDSCAPE — COMPARATIVE VIEW

Courts Supporting Consolidation

| Court | Case |

|---|---|

| Delhi HC | Ambika Traders (2025) |

| Delhi HC | Vallabh Textile (2024) |

| Calcutta HC | Britannia Industries (2024) |

| Supreme Court | Mathur Polymers (2025) |

Courts Opposing Consolidation

| Court | Case |

|---|---|

| Karnataka HC | Veremax Technology (2024) |

| Madras HC | R. Ashaarajaa (2025) |

| Kerala HC | Lakshmi Mobile Accessories (2025) |

📌 SC ruling now tilts balance in favour of consolidation — at least in fraud cases.

⏱️ LIMITATION — STILL YEAR-SPECIFIC

Important Clarification

| Aspect | Position |

|---|---|

| SCN format | Can be consolidated |

| Limitation under Section 74(10) | Still applies year-wise |

| Department’s burden | Must justify each year separately |

➡️ Consolidation ≠ dilution of limitation safeguards

🧠 PRACTICAL EXAMPLE (FININ2MIN STYLE)

Example — Fraud Case

- Fake invoices issued from FY 2019–20 to FY 2023–24

- Same suppliers, same pattern, circular ITC

- Department issues one SCN covering all years

✔ Valid after Mathur Polymers

Example — Non-Fraud Case

- Classification dispute across years

- No suppression / fraud alleged

⚠️ Consolidated SCN still litigation-prone

🎯 FININ2MIN TAKEAWAYS

What Is Settled Now

✔ Email to GST-registered address = valid service

✔ Consolidated SCNs permissible in fraud cases

✔ Courts won’t import restrictions absent in statute

What Taxpayers Must Watch

⚠ Keep GST portal email updated

⚠ Consolidation does not override limitation

⚠ Fraud tag (Section 74) changes everything

🧾 KEY PROVISIONS AT A GLANCE

| Provision | Relevance |

|---|---|

| Section 169(1)(c) | Valid service by registered email |

| Section 73 | Non-fraud demands |

| Section 74 | Fraud / suppression cases |

| Section 74(10) | 5-year limitation (year-wise) |

| Rule 142 | SCN & demand procedure |

The Supreme Court, by dismissing the SLP (Diary No. 50279/2025) in November 2025, affirmed the Delhi High Court’s judgment dated 26 August 2025, thereby upholding the validity of consolidated GST show cause notices covering multiple financial years in cases involving fraudulent ITC.

⚠️ DISCLAIMER

For information purposes only. Judicial positions may evolve. Applicability depends on facts, nature of allegations (fraud vs non-fraud), and jurisdiction. Not a substitute for professional advice.

Article related to –

Supreme Court GST consolidated SCN

Consolidated GST show cause notice fraud

Section 74 GST multiple years notice

Mathur Polymers GST case

Delhi HC consolidated GST notice upheld

GST fraud ITC consolidated notice

Email service of GST notice Section 169

Fraudulent ITC GST Supreme Court

Validity of consolidated SCN under GST

GST limitation Section 74(10)