“Family ≠ Relative in tax law. One mistake can cost you penalties.”

Finin2min | Income Tax • Personal Finance • Compliance

Key principle:

The Income-tax Act does not use the word family.

Tax exemption depends entirely on whether the donor qualifies as a “Relative” under Section 56(2)(x).

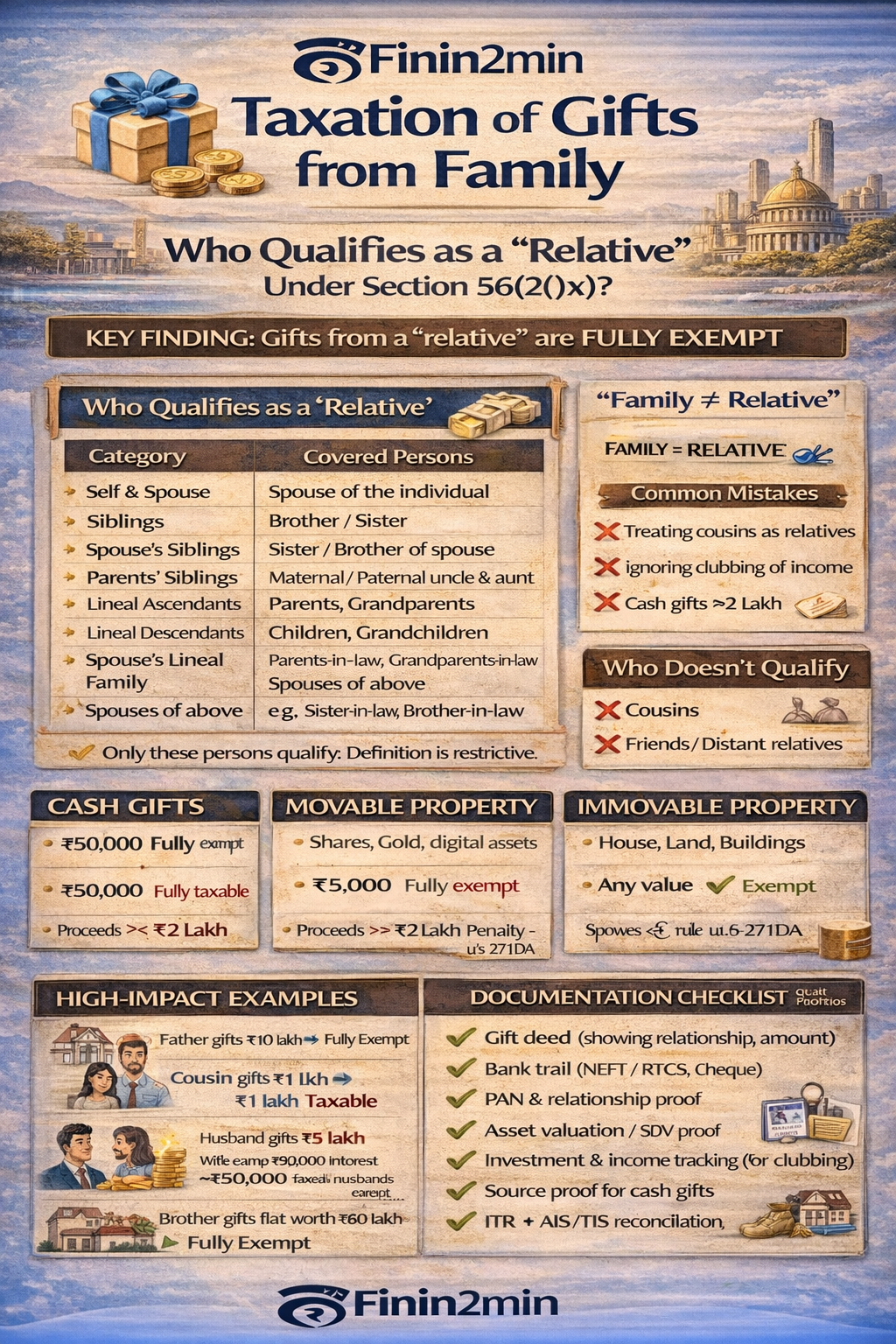

1️⃣ Who is a “Relative” under Section 56(2)(x)?

Gifts received from a relative are fully exempt, irrespective of:

- Amount

- Mode (cash / property / securities)

✅ Statutory Definition (Exhaustive)

| Category | Covered Persons |

|---|---|

| Self & Spouse | Spouse of the individual |

| Siblings | Brother / Sister |

| Spouse’s Siblings | Brother / Sister of spouse |

| Parents’ Siblings | Maternal / Paternal uncle & aunt |

| Lineal Ascendants | Parents, Grandparents |

| Lineal Descendants | Children, Grandchildren |

| Spouse’s Lineal Family | Parents-in-law, Grandparents-in-law |

| Spouses of above | e.g., Sister-in-law, Brother-in-law |

📌 Only these persons qualify. Definition is restrictive.

2️⃣ Common Relationship Clarifications (High-Risk Area)

| Relationship | Tax Treatment |

|---|---|

| Parents / Children | ✅ Exempt |

| Parents-in-law | ✅ Exempt |

| Brother-in-law / Sister-in-law | ✅ Exempt |

| Cousins | ❌ Taxable |

| Friends / Distant relatives | ❌ Taxable |

| Spouse | ✅ Exempt (but clubbing applies later) |

3️⃣ Cash / Monetary Gifts — Tax Rules

📌 Section 56(2)(x)

| Scenario | Tax Impact |

|---|---|

| ≤ ₹50,000 (aggregate in FY) | ✅ Fully exempt |

| > ₹50,000 | ❌ Entire amount taxable |

| From a Relative (any amount) | ✅ Fully exempt |

⚠️ Section 269ST Alert:

Cash receipts ≥ ₹2,00,000 in a single day / transaction / from one person may attract penalty u/s 271DA, even if gift is otherwise exempt.

4️⃣ Gift of Movable Property (Shares, Jewellery, VDA etc.)

📦 Covered Assets (Specified Movable Property)

- Shares & securities

- Jewellery

- Bullion

- Art, paintings, sculptures

- Archaeological collections

- Virtual Digital Assets (crypto, NFTs)

Tax Treatment for Recipient

| Mode | Condition | Tax Impact |

|---|---|---|

| Without consideration | FMV > ₹50,000 | FMV taxable |

| Inadequate consideration | (FMV – price) > ₹50,000 | Difference taxable |

| From Relative | Any value | ✅ Exempt |

📌 Other movable items (cars, furniture, gadgets) → Not taxable under this section.

5️⃣ Gift of Immovable Property (Land / Building)

🏠 Recipient-side Taxation

| Mode | Condition | Taxable Value |

|---|---|---|

| Without consideration | Stamp duty value > ₹50,000 | Entire stamp value |

| Inadequate consideration | SDV exceeds consideration by >10% AND >₹50,000 | Difference taxable |

| From Relative | Any value | ✅ Exempt |

📌 Stamp Duty Value (SDV) governs valuation, not market estimates.

6️⃣ Donor-Side Treatment (Often Misunderstood)

Section 47 — Capital Gains Exemption

| Donor | Capital Gains |

|---|---|

| Gifts to relative | ❌ No capital gains |

| Gifts to non-relative | ❌ No capital gains |

📌 Capital gains arise only when recipient sells the asset

→ Cost & holding period of donor get carried forward.

7️⃣ Gifts from Spouse & Clubbing Provisions ⚠️

Section 64(1)(iv)

| Scenario | Tax Impact |

|---|---|

| Gift from spouse | Gift itself exempt |

| Income from gifted asset | Clubbed with spouse’s income |

| Capital gains on sale | Clubbed |

📌 Exception:

If spouse invests independently (not from gifted funds), clubbing does not apply.

8️⃣ High-Impact Examples

Example 1 — Parent to Child

Father gifts ₹10 lakh → Fully exempt

Example 2 — Cousin gift

Cousin gifts ₹1 lakh → ₹1 lakh fully taxable

Example 3 — Spouse gift

Husband gifts ₹5 lakh → Wife earns ₹50,000 interest

→ ₹50,000 taxed in husband’s hands

Example 4 — Property from brother

Brother gifts flat worth ₹80 lakh → Fully exempt

9️⃣ Common Mistakes Taxpayers Make 🚫

| Error | Risk |

|---|---|

| Treating cousins as relatives | Additions & penalties |

| Ignoring clubbing rules | Income re-taxed |

| Cash gifts ≥ ₹2 lakh | Penalty u/s 271DA |

| No documentation | Scrutiny exposure |

| Not reconciling AIS/TIS | Notices |

🔟 Documentation Checklist (Best Practice)

✔ Gift deed (relationship, amount, no consideration)

✔ Bank trail (NEFT / RTGS / cheque)

✔ PAN & relationship proof

✔ Asset valuation / SDV proof

✔ Investment & income tracking (for clubbing)

✔ Source proof for cash gifts

✔ ITR + AIS/TIS reconciliation

🎯 Finin2min Takeaway

Gift taxation is relationship-driven, not emotion-driven.

Exempt today ≠ tax-free tomorrow (clubbing matters).

Documentation converts family transfers into defensible compliance.

This content is for general information and educational purposes only. It does not constitute legal, tax, accounting, or professional advice. Views expressed are based on prevailing laws and interpretations at the time of publication. Readers should consult their professional advisors before taking any action.

Article related to –

Income Tax on Gifts

Section 56(2)(x)

Gift Tax India

Gifts from Family Taxation

Relative Definition Income Tax

Cash Gift Tax

Property Gift Tax

Clubbing of Income