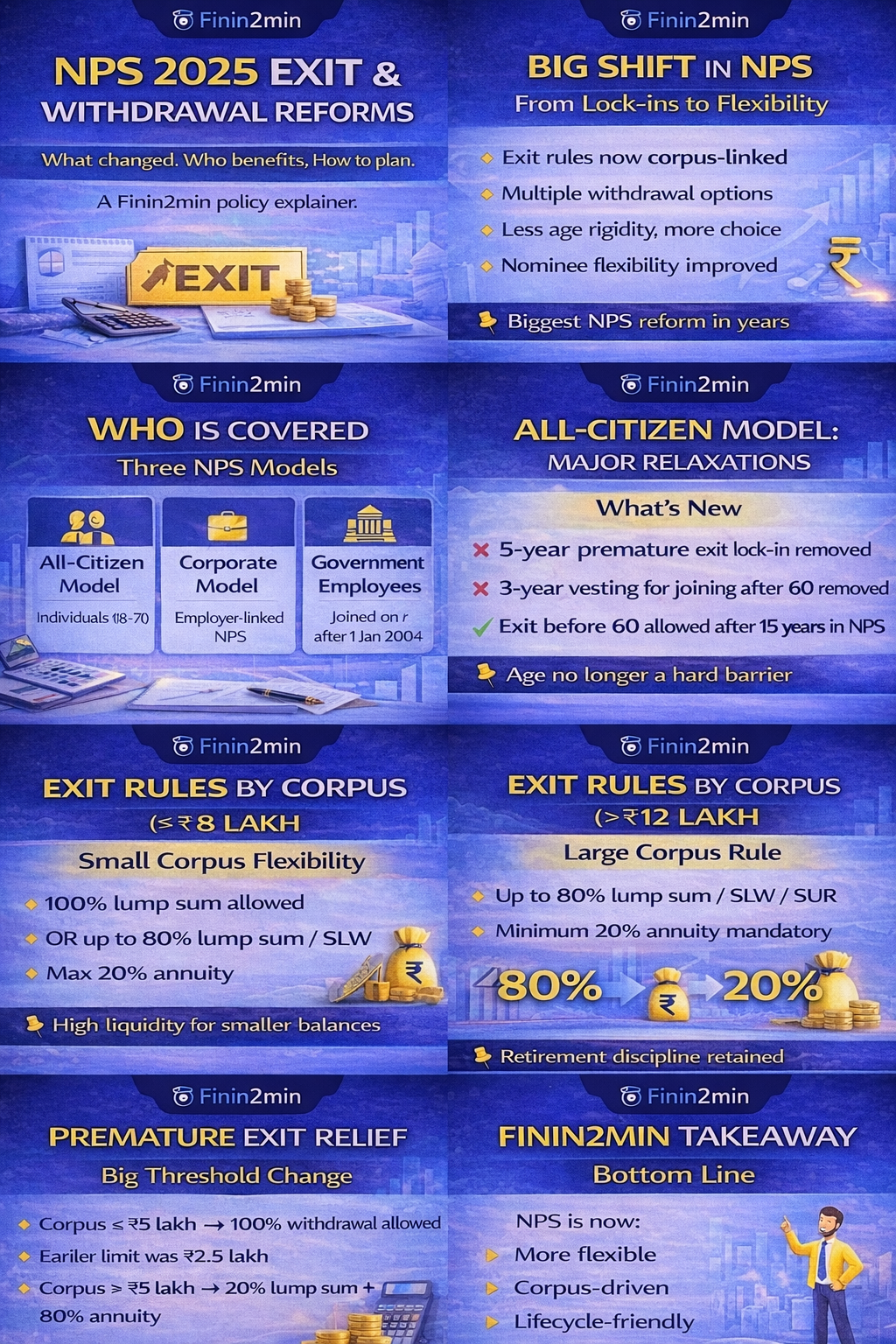

More flexibility. Corpus-driven exits. Fewer lock-in

Regulatory basis: Amendments notified on 16 December 2025 under the PFRDA (Exits and Withdrawals under NPS) Amendment Regulations, 2025 by Pension Fund Regulatory and Development Authority (PFRDA).

The 2025 NPS amendments fundamentally modernise exit rules, shifting the system from lock-in driven to lifecycle-friendly. Subscribers now have real control over liquidity, timing, and structure, without diluting retirement discipline.

⚠️ Disclaimer

This guide is for educational purposes only, based on prevailing law, press releases, and FAQs as on date. It does not constitute professional advice. Users should evaluate facts case-by-case and consult advisors before investing.

Article related to – NPS 2025 amendments explained NPS exit and withdrawal rules 2025 PFRDA NPS reforms NPS premature exit rules NPS corpus based withdrawal NPS annuity vs lump sum rules