Limits, GST QR Thresholds & Compliance Discipline (Finin2min)

UPI has created a perfect banking trail—fast, convenient, and fully traceable.

That transparency brings compliance responsibility, especially for salaried individuals, traders, and service providers.

This Finin2min brief separates law, notified limits, and best practices.

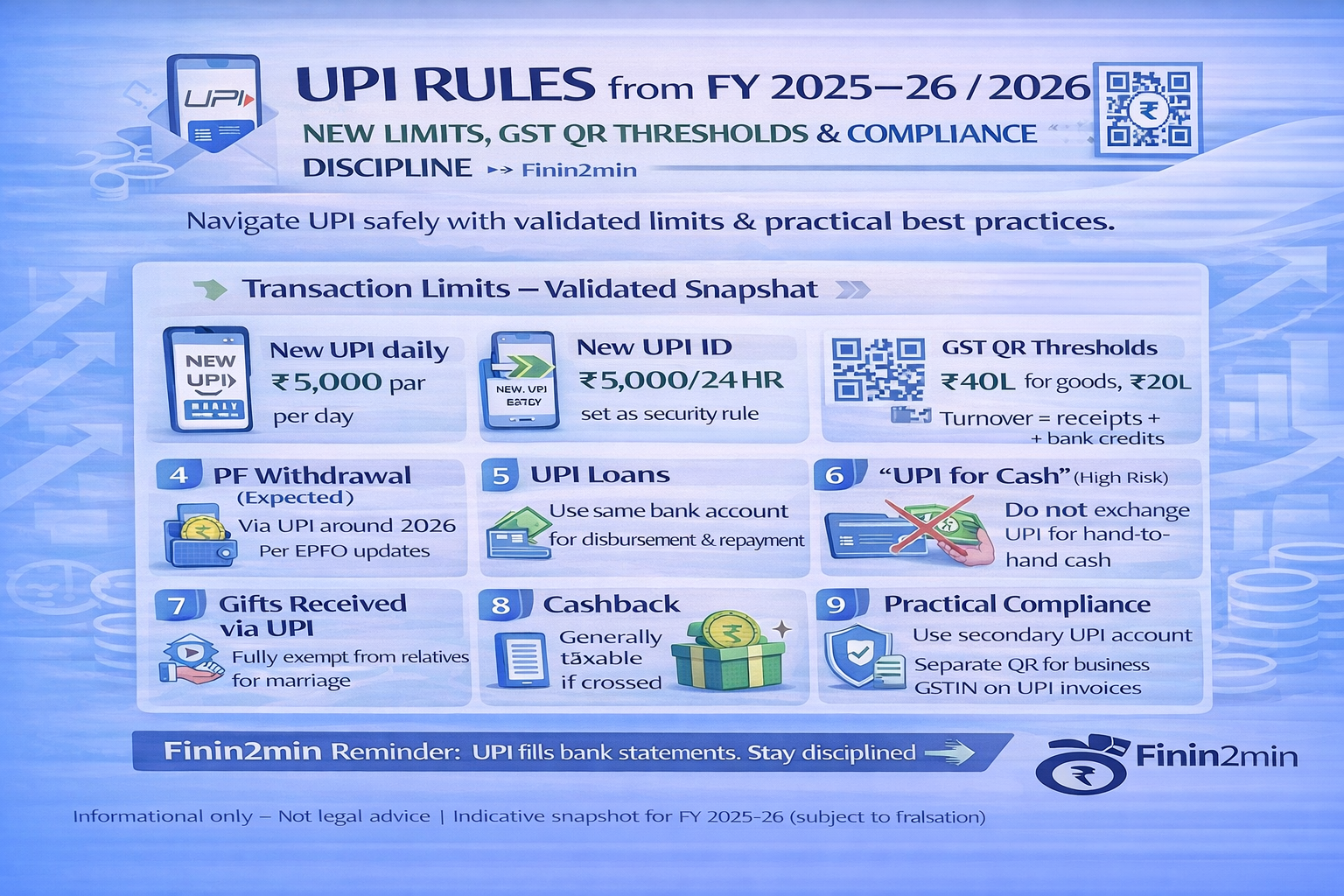

1️⃣ UPI Transaction Limits — Validated Snapshot

| Category | Limit | Status |

|---|---|---|

| Normal UPI daily limit | ₹1,00,000 per day | ✔ Existing |

| Higher limit (specified use-cases) | Up to ₹5,00,000 per day | ✔ Existing |

| Applicable for ₹5 lakh limit | Medical, Education, Insurance, Credit card payments, Travel, Capital markets / IPO | ✔ NPCI-enabled |

| New UPI ID – first 24 hours | ₹5,000 total | ✔ Security rule |

📌 Finin2min insight:

Higher limits apply only if the transaction is tagged to permitted categories.

2️⃣ PF Withdrawal through UPI — Status Clarified

| Item | Position |

|---|---|

| PF withdrawal via UPI | Announced / pilot stage |

| Expected rollout | Around 2026 (as per EPFO updates) |

| Current status | Not fully operational yet |

📌 Important:

Treat this as expected, not guaranteed, until EPFO notification.

3️⃣ Business QR / UPI Receipts & GST Thresholds (Law)

| Nature of Business | GST Registration Mandatory If Turnover Exceeds |

|---|---|

| Sale of goods | ₹40,00,000 |

| Supply of services | ₹20,00,000 |

✔ UPI / QR receipts count as turnover

✔ Bank trail is fully visible to GST authorities

📌 Crossing threshold without GST → notices & penalties possible

4️⃣ If You Are Already GST-Registered

| Area | Compliance Expectation |

|---|---|

| UPI receipts | Must be treated as taxable supply where applicable |

| Invoicing | GSTIN to be reflected correctly |

| Returns | UPI receipts to match GSTR-1, GSTR-3B & books |

📌 Finin2min reminder:

UPI ≠ informal receipt. It is formal banking evidence.

5️⃣ “UPI for Cash” — High-Risk Behaviour (Not Advisable)

| Practice | Risk |

|---|---|

| Taking UPI & giving cash | UPI receipt may be treated as income |

| No documentary context | High scrutiny risk |

| Repeated pattern | Possible tax additions |

❌ Strongly discouraged

✔ This is risk-based guidance, not a separate statute

6️⃣ Loans through UPI — Best Practice (Clarified)

| Aspect | Guidance |

|---|---|

| Loan disbursement & repayment | Use same bank account |

| Reason | Clean audit trail & reconciliation |

| Legal status | Best practice (not mandatory law) |

📌 Avoid multiple UPI IDs/accounts for the same loan flow.

7️⃣ Gifts Received via UPI — Correct Legal Position ✅

| Item | Rule under Income-tax Act |

|---|---|

| General gift exemption | Up to ₹50,000 per year |

| Gift from relatives | Fully exempt (no limit) |

| Gift on marriage | Fully exempt |

| Beyond ₹50,000 (non-relative) | Taxable as income |

8️⃣ Cashback from UPI Apps — Tax Treatment

| Type of Cashback | Tax Position |

|---|---|

| Personal promotional cashback | Generally taxable if significant |

| Business cashback / incentives | Taxable as income |

| Reporting | Must be disclosed in ITR |

📌 Best practice:

Treat cashback as income unless clearly exempt.

9️⃣ Practical Compliance Discipline (Expert View)

| Area | Finin2min Best Practice |

|---|---|

| Accounts | Separate personal & business UPI |

| Bank accounts | Use secondary account for UPI |

| App security | Set limits, locks & trusted contacts |

| Records | Monthly reconciliation |

| GST | Apply tax correctly on UPI receipts |

| Behaviour | Avoid UPI–cash exchange |

🔟 Final Takeaways (Finin2min Snapshot)

| Topic | Key Point |

|---|---|

| UPI limit | ₹1 lakh normal, ₹5 lakh for specific use |

| New UPI ID | ₹5,000 cap for first 24 hours |

| GST & QR | Goods ₹40L / Services ₹20L |

| Gifts | ₹50,000 limit (not ₹500) |

| Cashback | Report in ITR |

| Loans | Same account = clean trail |

| UPI ≠ cash | Always traceable |

📌 Finin2min Bottom Line

UPI convenience comes with audit-level visibility.

Use it with structure, separation, and discipline.

⚠️ Disclaimer

This content is for general informational and educational purposes only. It reflects current UPI norms, GST law, and Income-tax provisions as on date, along with best-practice guidance. It does not constitute legal or tax advice. Readers should consult professionals before acting.

Article related to –

UPI transaction share 2025

UPI market share by app

PhonePe UPI share

Google Pay UPI transactions

Paytm UPI market share

UPI payment apps India

Digital payments market India

NPCI UPI statistics

UPI ecosystem India

Digital payment trends India

Fintech payments India