Shift from Assessment Year to Tax Year — What Changes for Taxpayers (Finin2min)

Status note (important):

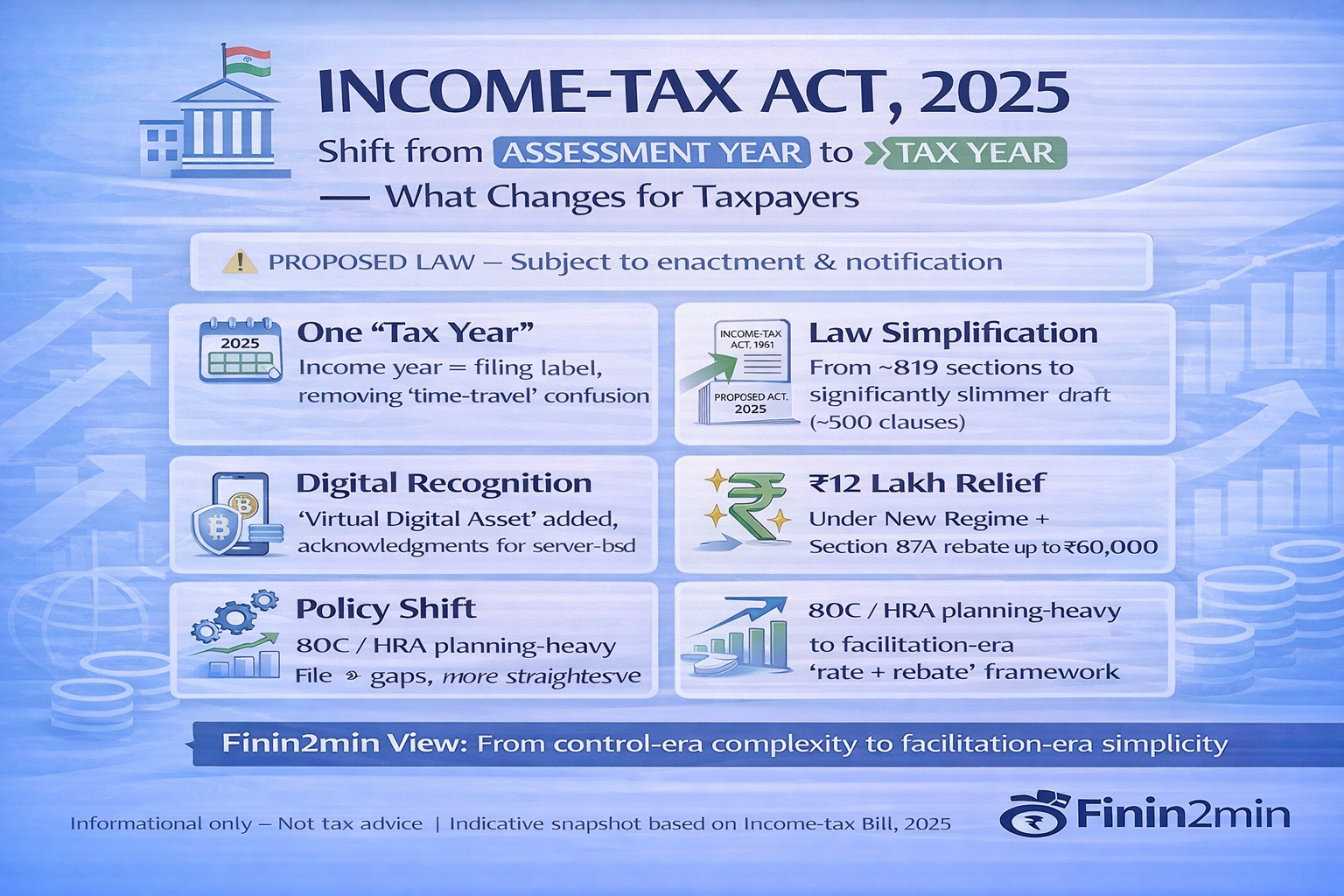

The Income-tax Bill, 2025 is a proposed law. All references below are based on Bill drafts, policy statements, and explanatory material available as of date. Final numbers and provisions will apply only after enactment and notification.

1️⃣ Core Concept Change — Old vs New

| Aspect | Income-tax Act, 1961 | Income-tax Bill, 2025 (Proposed) |

|---|---|---|

| Year terminology | Previous Year + Assessment Year | Single “Tax Year” |

| Income period | Earned in one year | Earned in the same Tax Year |

| Return reference | Filed in next “Assessment Year” | Filed for the same Tax Year |

| Language complexity | Dual timelines | Single, citizen-friendly timeline |

📌 Finin2min view:

This removes the long-standing “time-travel” confusion in tax filing.

2️⃣ Why “Assessment Year” Was a Pain Point

| Issue | Practical Consequence |

|---|---|

| Dual year references | Mismatch between income year & filing year |

| “Assessment” label | Felt like filing for a future year |

| Legal drafting style | Increased dependence on professionals |

| Honest errors | Wrong year selection → notices & rectifications |

📌 Policy intent:

Simplify language, not just procedures.

3️⃣ What “Tax Year” Means in Practice

| Item | Proposed Treatment |

|---|---|

| Income earned | During the Tax Year |

| Return filing | For the same Tax Year |

| Notices & assessments | Tagged to one year identity |

| Forms & portals | Expected to follow the same logic |

📌 Ease-of-living objective:

Tax compliance should feel intuitive, not legalistic.

4️⃣ Structural Simplification — Corrected & Validated

| Metric | Income-tax Act, 1961 | Income-tax Bill, 2025 (Proposed) |

|---|---|---|

| Nature of law | Amendment-driven over decades | Clean-slate redrafting |

| Size | Large, layered statute | Significantly slimmer |

| Sections / clauses | ~819 sections | Estimated ~500 clauses (draft-based) |

| Official final count | Known | Yet to be notified |

| Policy signal | Complexity & overlap | Consolidation & clarity |

📌 Important clarification:

There is no officially notified final clause count yet.

Drafts and public material broadly indicate a substantially reduced statute, commonly estimated in the ~400–500 clause range.

5️⃣ Digital & Future-Ready Design

| Area | Proposed Change |

|---|---|

| Digital assets | “Virtual Digital Asset” expressly defined |

| Technology | Recognition of server-based security |

| Economic alignment | Law drafted for digital-first businesses |

| Enforcement design | Better tech–law synchronisation |

📌 Governance lens:

Reduce gaps between business reality and statutory language.

6️⃣ ₹12 Lakh “Tax-Free” Headline — Reality Check

| Item | Actual Position (Proposed) |

|---|---|

| Tax-free income up to ₹12 lakh | Not automatic |

| Applicable to | New Tax Regime only |

| Mechanism | Section 87A rebate |

| Old regime taxpayers | No blanket ₹12 lakh relief |

| Policy direction | Shift towards rebate-based simplicity |

📌 Key clarification:

This is rebate-driven relief, not a universal zero-tax slab.

7️⃣ Old Regime vs New Regime — Policy Direction

| Parameter | Old Regime | New Regime (Policy-favoured) |

|---|---|---|

| Deductions | 80C, HRA, etc. | Minimal |

| Compliance style | Planning-heavy | Rate & rebate-based |

| Behaviour encouraged | Deduction optimisation | Simple reporting |

| Long-term signal | Gradual de-emphasis | Mainstream framework |

8️⃣ Practical Impact — Expert View

| Area | Expected Outcome |

|---|---|

| Language-related mistakes | Reduced |

| Year-selection disputes | Significantly lower |

| First-time taxpayers | Greater clarity |

| Litigation volume | Expected moderation over time |

| Faceless assessment | More consistent & effective |

| Tax planning | Less structural, more straightforward |

9️⃣ Key Takeaways (Finin2min Snapshot)

| Theme | What Changes |

|---|---|

| Timeline concept | Assessment Year → Tax Year |

| Law structure | Bulky → Significantly slimmer |

| Digital economy | Explicit statutory recognition |

| ₹12 lakh relief | Conditional, New Regime only |

| Policy philosophy | Control-era → Facilitation-era |

📌 Finin2min Bottom Line

The Income-tax Bill, 2025 is not just a tax amendment.

It is a language reset, structural clean-up, and behavioral nudge toward simpler compliance.

⚠️ Disclaimer

This content is for general informational and educational purposes only. It reflects provisions as proposed in the Income-tax Bill, 2025 and publicly available drafts and policy statements. Figures and structures are indicative and subject to change upon enactment. Readers should rely on the notified law and consult professional advisors before taking action.

Article related to –

Income-tax Act 2025

Tax Year vs Assessment Year

Income tax law simplification India

Tax Year concept India

Income Tax Bill 2025 explained

Section 87A rebate 2025

New tax regime India 2025

Tax compliance simplification India

Digital assets income tax law

Virtual digital asset tax India

Faceless assessment India

Income tax reform India