Markets • Gold & Silver • Sectors • Global Economy

Finin2min | 2025 Year-in-Review

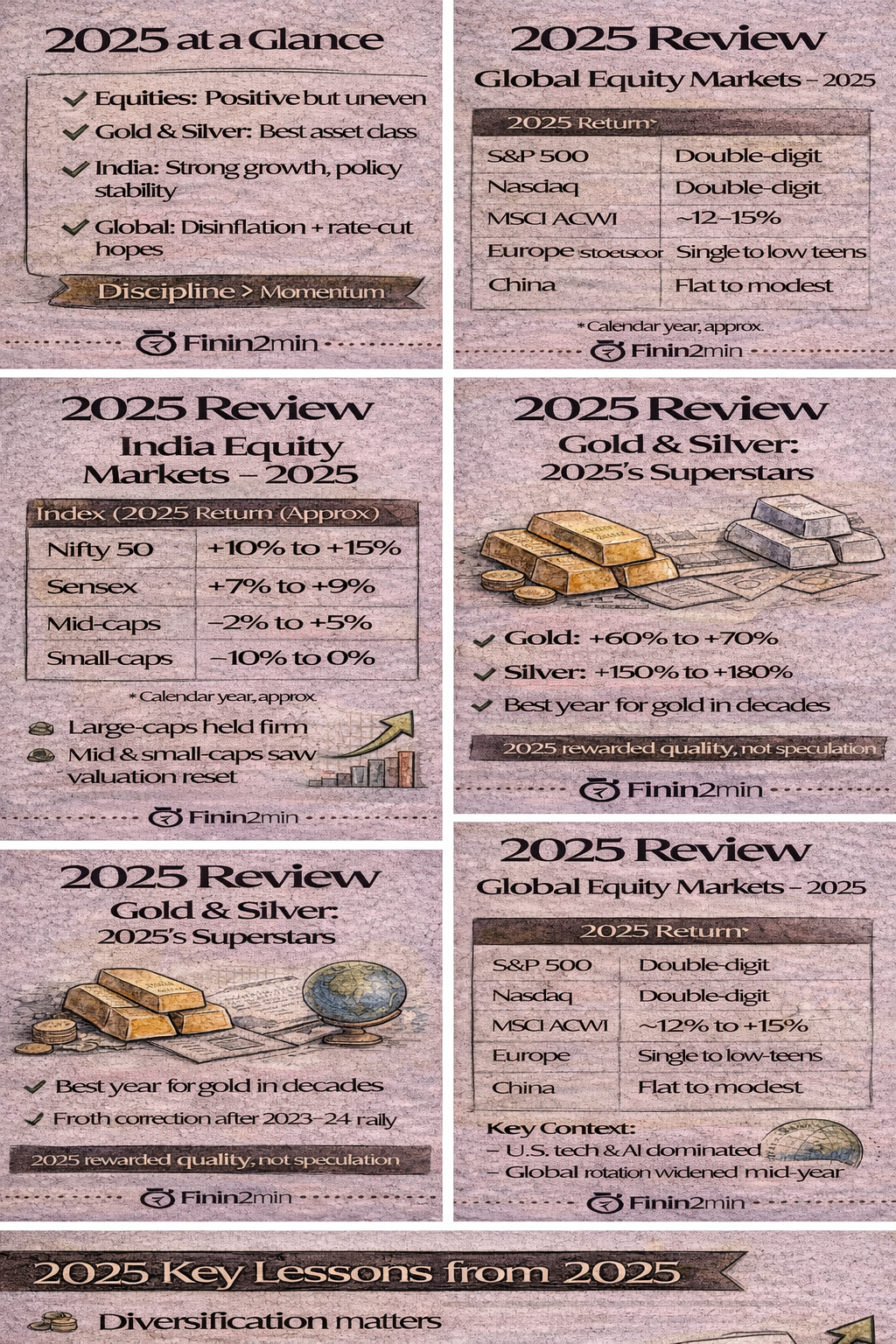

Executive Snapshot – 2025 at a Glance

| Theme | 2025 Outcome |

|---|---|

| Equity markets | Positive but uneven; large-caps resilient |

| Gold & silver | Best-performing asset class |

| Sector trends | Defence, infra & metals outperformed |

| India macro | Strong growth with policy stability |

| Global economy | Disinflation phase, rate-cut expectations |

2025 was a year of recalibration, not excess — markets rewarded discipline, balance-sheet strength, and diversification.

1. Indian Equity Markets – Calendar Year 2025

Headline Index Performance (Price Returns, Approx.)

| Index | 2025 Return | Interpretation |

|---|---|---|

| Nifty 50 | +10% to +15% | Large-caps absorbed volatility |

| Sensex | +7% to +9% | Similar large-cap composition |

| Mid-cap indices | -2% to +5% | Post-froth cooling |

| Small-cap indices | -10% to 0% | Valuation reset phase |

Key Market Drivers

- FPI flows volatile, with net outflows at intervals

- Domestic SIP & retail flows stabilised large-caps

- Earnings scrutiny intensified after 2023–24 rally

- Valuation discipline returned to mid & small-caps

Finin2min Take:

2025 separated quality leadership from momentum excess.

2. Global Equity Markets – Relative Performance (2025)

| Market / Index | 2025 Return (Approx.) | Key Theme |

|---|---|---|

| S&P 500 (US) | High single to low double-digit | AI & mega-cap tech |

| Nasdaq (US) | Double-digit | Growth & AI premium |

| MSCI ACWI (Global) | ~12% to 15% | Broad global participation |

| STOXX 600 (Europe) | Single-digit to low-teens | Rate-cut optimism |

| China equities | Flat to mildly positive | Policy stabilisation |

Global Market Context

- Disinflation + rate-cut expectations lifted risk assets

- U.S. remained return anchor, but rotation widened

- Geopolitics caused volatility, not trend reversal

3. Gold & Silver – The Clear Winners of 2025

Precious Metals Performance (India Prices, YoY)

| Asset | 2025 Gain (Approx.) | Why It Matters |

|---|---|---|

| Gold | +60% to +70% | One of best years in decades |

| Silver | +150% to +180% | Exceptional cyclical & speculative rally |

Key Drivers Behind the Surge

- Anticipation of global rate cuts in 2026

- Central-bank gold accumulation

- Geopolitical uncertainty & currency concerns

- Silver benefited from industrial + investment demand

Finin2min Take:

2025 reaffirmed metals as macro-risk insurance, not just commodities.

4. India Sectoral Performance – Winners & Laggards

| Sector | 2025 Trend | Commentary |

|---|---|---|

| Banking & Financials | Stable | Earnings-led support |

| Defence & Aerospace | Strong outperformer | Order visibility + policy push |

| Metals & Mining | Strong | Global commodity upcycle |

| Capital goods / Infra | Positive | Public capex momentum |

| IT & Technology | Mixed | Margin & demand pressure |

| FMCG / Consumption | Muted | Rural & cost headwinds |

Theme:

Cyclicals and policy-linked sectors outperformed defensives and consumption.

5. Policy & Macro Landscape – India vs Global

Union Budget 2025–26 & RBI

- Focus on fiscal discipline with growth

- Continued infrastructure & capex emphasis

- Tax regime simplification and compliance analytics

- RBI maintained data-driven stability, no shocks

Macro Indicators (Approx.)

| Indicator | India | Global |

|---|---|---|

| GDP growth | ~6%–7% | ~3%–3.2% |

| Inflation | Moderating | Sticky but easing |

| Fiscal stance | Expansion with discipline | Mixed |

| Growth ranking | Among fastest-growing | Uneven recovery |

India entered 2026 structurally stronger than peers.

6. Key Lessons from 2025 (Investor & Business Lens)

| Lesson | What 2025 Proved |

|---|---|

| Diversification | Crucial across assets |

| Commodities | Effective macro hedge |

| Valuations | Excess corrects eventually |

| Policy stability | Matters more than stimulus |

| Compliance | Data-driven enforcement is permanent |

Finin2min Final Word

2025 was not about chasing momentum — it was about respecting cycles.

Markets rewarded discipline, diversification, and alignment with macro and policy reality.

Gold and silver reminded investors that risk hedging matters as much as return chasing.

The core 2025 takeaway:

Sustainable wealth is built by structure, not speculation.