Inter-State Supply Confirmed Despite Transfer of Title at Factory

(Toyota Kirloskar Motor Pvt. Ltd. v. UOI – Nov 2025)

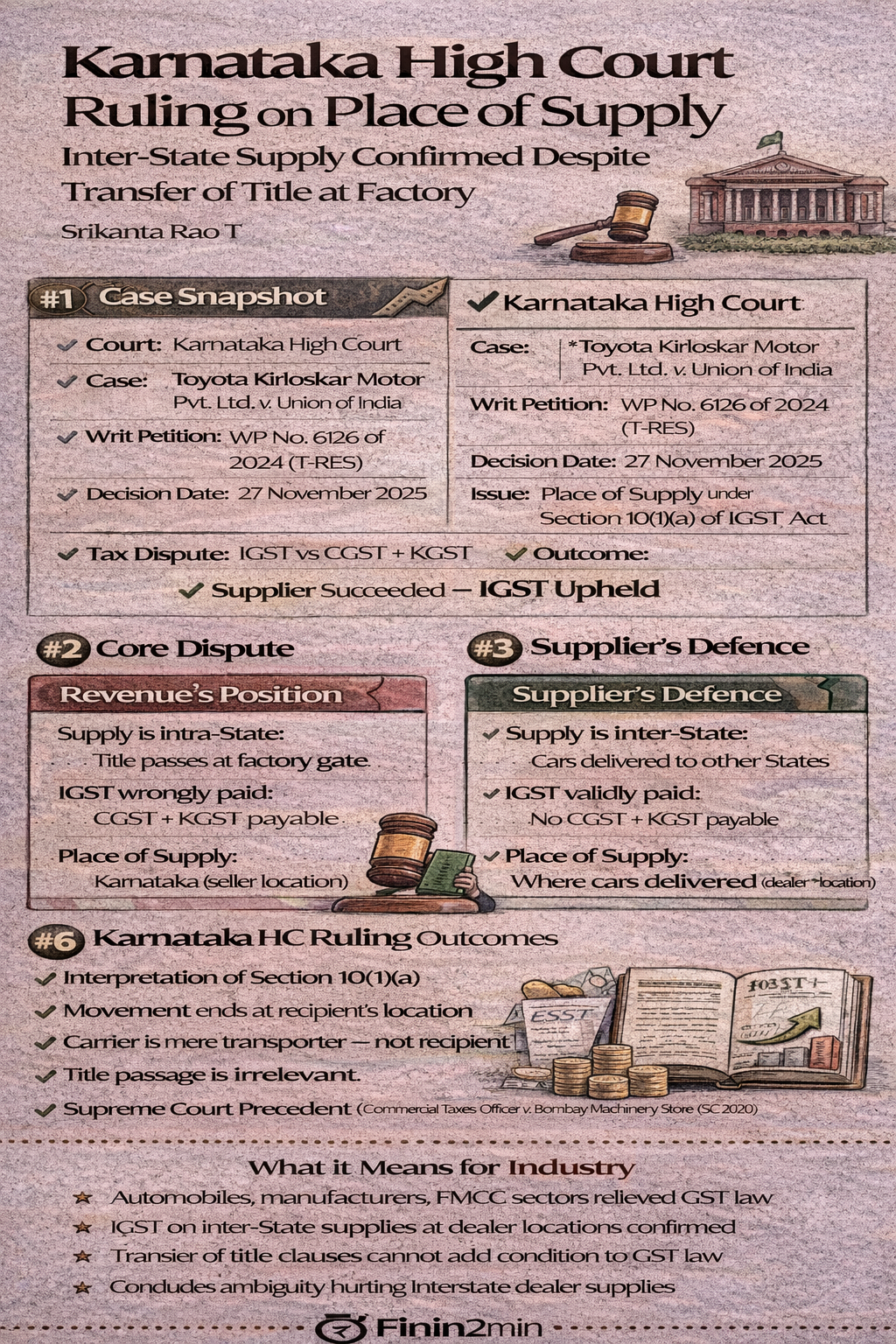

1️⃣ Case Snapshot (At a Glance)

| Particulars | Details |

|---|---|

| Court | Karnataka High Court |

| Case | Toyota Kirloskar Motor Pvt. Ltd. v. Union of India & Ors. |

| Writ Petition | WP No. 6126 of 2024 (T-RES) |

| Decision Date | 27 November 2025 |

| Issue | Place of Supply under Section 10(1)(a) of IGST Act |

| Tax Dispute | IGST vs CGST + KGST |

| Outcome | Supplier succeeded – IGST upheld |

2️⃣ Core Legal Issue

Whether supply of motor vehicles to dealers located outside Karnataka becomes an intra-State supply merely because:

- Title and risk pass at the factory gate in Karnataka, and

- Goods are handed over to a common carrier at Karnataka?

3️⃣ Relevant Statutory Provision (Validated)

Section 10(1)(a) – IGST Act, 2017

| Parameter | Statutory Position |

|---|---|

| Applicability | Supply of goods within India (non-import/export) |

| Test | Whether supply involves movement of goods |

| Place of Supply | Location of goods when movement terminates for delivery to recipient |

| Key Point | No reference to transfer of ownership/title |

✔️ The statute focuses on “termination of movement for delivery”, not “passing of title”

4️⃣ Revenue’s Stand (Rejected by Court)

| Revenue Argument | Basis |

|---|---|

| Supply is intra-State | Title & risk pass at factory gate |

| Delivery completed at Karnataka | Dealer agreement clauses |

| IGST wrongly paid | CGST + KGST payable |

| Place of supply | Karnataka (factory location) |

📌 Error Identified: Revenue imported Sale of Goods Act concepts into GST law.

5️⃣ Supplier’s Stand (Accepted)

| Supplier’s Argument | Reasoning |

|---|---|

| Supply is inter-State | Dealers located outside Karnataka |

| Movement continues | Till dealer location |

| Carrier ≠ Recipient | Dealer is the recipient |

| IGST correctly discharged | No double taxation possible |

6️⃣ Karnataka HC’s Findings (Key Holdings)

A. Interpretation of Section 10(1)(a)

| Aspect | Court’s Finding |

|---|---|

| Movement of goods | Continues till delivery to recipient |

| Common carrier | Merely a transporter, not recipient |

| Termination of movement | At dealer’s destination, not factory |

| Transfer of title | Irrelevant for place of supply |

✔️ Passing of title ≠ Termination of movement

B. Revenue Neutrality

| Scenario | Impact |

|---|---|

| IGST already paid | Refund required if CGST+KGST demanded |

| Result | Double taxation |

| Court’s view | Legally impermissible |

7️⃣ Supreme Court Support (Binding Precedent)

Commercial Taxes Officer v. Bombay Machinery Store (SC – 2020)

| Principle | Legal Position |

|---|---|

| Movement begins | When goods handed to carrier |

| Movement ends | When delivery taken from carrier |

| Constructive delivery | Not recognised |

| Administrative interpretation | Cannot override statute |

📌 GST law mirrors CST logic on movement of goods

8️⃣ Divergent Kerala HC View (Why It’s Distinguishable)

| Case | Kun Motor Co. Pvt. Ltd. (Kerala HC) |

|---|---|

| Context | E-way bill requirement |

| Facts | Temporary registration, insurance, vehicle usage |

| Finding | Treated as used personal effect |

| Limitation | Fact-specific; not a pure POS ruling |

⚠️ Does not dilute Section 10(1)(a) interpretation in commercial dealer supplies

9️⃣ Comparative Legal Position (Quick Chart)

| Test | Karnataka HC | Kerala HC |

|---|---|---|

| Focus | Destination delivery | Ownership indicators |

| POS Determination | Recipient location | Seller location |

| Alignment with SC | ✔ Yes | ❌ Weak |

| Applicability | Industry-wide | Fact-specific |

🔟 Compliance & Industry Impact

What This Ruling Clarifies

| Area | Impact |

|---|---|

| Dealer supplies | Inter-State if destination is outside State |

| IGST liability | Correct even if title passes earlier |

| Audit objections | Cannot rely on title clauses |

| Double taxation | Prevented |

🧠 Finin2min Practical Takeaways

✔ Place of supply follows movement, not ownership

✔ Carrier is not the recipient

✔ Title clauses in contracts cannot override GST statute

✔ Audit interpretations must align with Section 10(1)(a)

✔ Industry relief for automobile & manufacturing sector

📌 Final Word

The Karnataka High Court ruling restores statutory discipline to GST place-of-supply analysis.

By aligning with Supreme Court jurisprudence, it rejects administrative overreach and provides much-needed certainty for inter-State dealer supplies.

Under GST, delivery destination determines place of supply — not factory gates, invoices, or title clauses.