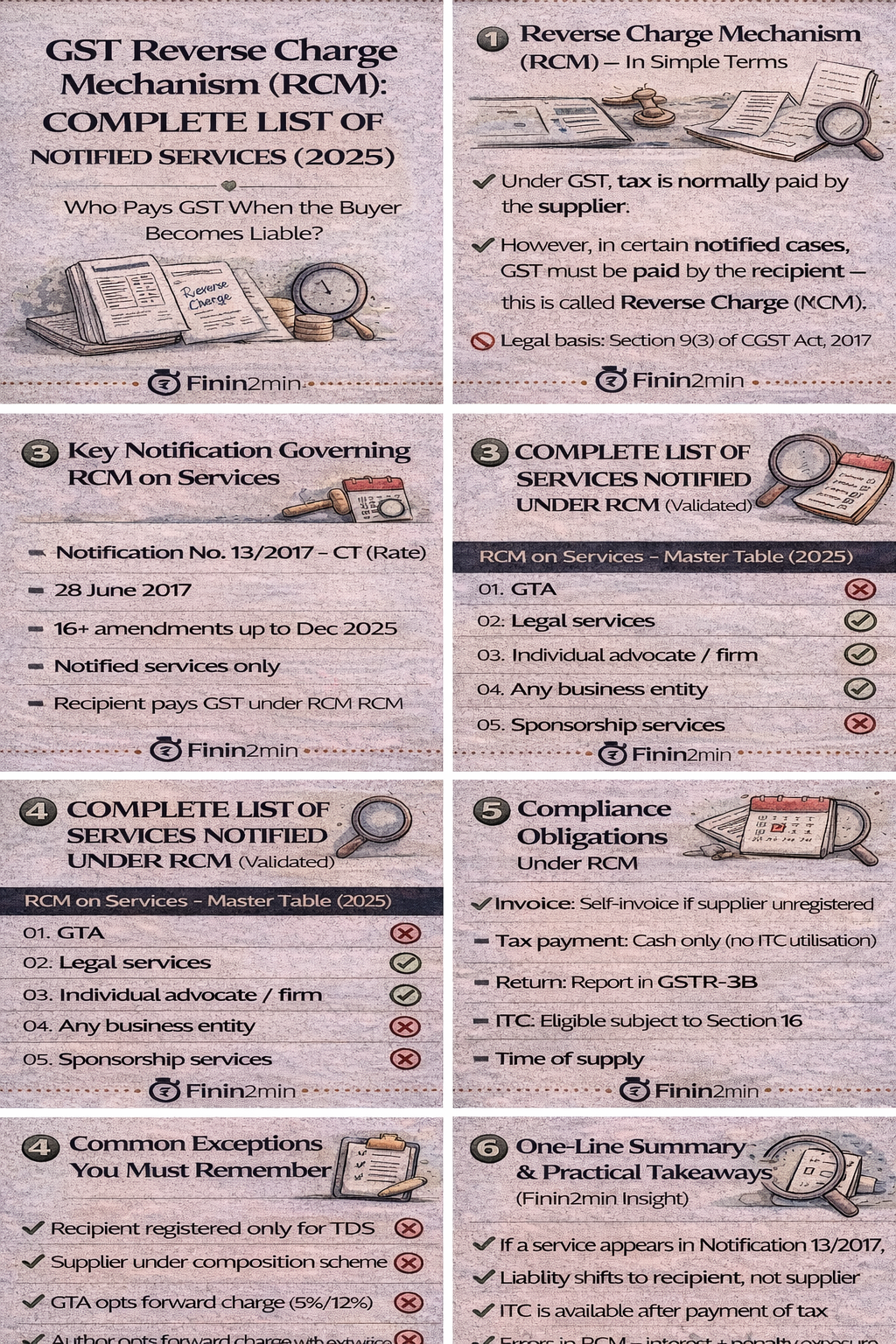

Who Pays GST When the Buyer Becomes Liable?

🔷 1. Reverse Charge Mechanism (RCM) – In Simple Terms

Under GST, tax is normally paid by the supplier.

However, in certain notified cases, GST must be paid by the recipient — this is called Reverse Charge Mechanism (RCM).

📌 Legal basis: Section 9(3) of CGST Act, 2017

🔷 2. Key Notification Governing RCM on Services

| Particular | Details |

|---|---|

| Principal Notification | Notification No. 13/2017 – CT (Rate) |

| Date | 28 June 2017 |

| Amendments | 16+ amendments up to Dec 2025 |

| Coverage | Notified services only |

| Liability | Recipient pays GST under RCM |

🔷 3. Complete List of Services Notified Under RCM (Validated)

RCM on Services – Master Table (2025)

| Sl. | Nature of Service | Service Provider | Service Recipient (Liable to Pay GST) | Key Conditions / Exceptions |

|---|---|---|---|---|

| 1 | Goods Transport Agency (GTA) | Any GTA | Registered person / factory / society / body corporate / LLP / partnership | ❌ If supplier opts forward charge & declares on invoice |

| 2 | Legal services | Individual advocate / firm | Any business entity | Includes advisory, consultancy & representational |

| 3 | Arbitral tribunal services | Arbitral tribunal | Any business entity | No threshold exemption |

| 4 | Sponsorship services | Any person (non-body corporate) | Body corporate / partnership / LLP | Recipient liable |

| 5 | Govt./Local Authority services (excluding notified exemptions) | Govt./Local authority | Business entity | Excludes post, railways, transport, aircraft/vessel |

| 6 | Renting of immovable property (Govt.) | Govt./Local authority | Registered person | Mandatory RCM |

| 7 | Renting of residential dwelling | Any person | Registered person | Introduced via 2022 amendment |

| 8 | Renting of immovable property (non-residential) | Any person | Registered person | ❌ Not applicable to composition dealers |

| 9 | Transfer of Development Rights / FSI | Any person | Promoter | Payable at time of completion |

| 10 | Long-term lease of land (≥30 yrs) | Any person | Promoter | Upfront premium / rent covered |

| 11 | Director’s services | Director | Company / body corporate | Includes executive & non-exec directors |

| 12 | Insurance agent services | Insurance agent | Insurance company | Standard RCM entry |

| 13 | Recovery agent services | Recovery agent | Bank / FI / NBFC | Includes loan recovery |

| 14 | Copyright – music/artistic works | Artist / composer | Music company / producer | Includes assignment or licensing |

| 15 | Copyright – literary works | Author | Publisher | ❌ Forward charge allowed with declaration |

| 16 | Overseeing Committee services | Committee member | RBI | Specific RBI notification |

| 17 | Direct Selling Agent (DSA) | Individual DSA | Bank / NBFC | ❌ Not applicable if DSA is body corporate |

| 18 | Business Facilitator (BF) | BF | Bank | Banking outreach services |

| 19 | Agent of Business Correspondent (BC) | Agent | Business Correspondent | Inter-BC services |

| 20 | Security services | Security agency | Registered person | ❌ Not applicable if supplier under composition |

| 21 | Motor vehicle rental (fuel included) | Non-body corporate | Registered person | Invoice must not charge GST |

| 22 | Securities lending services | Lender of securities | Borrower of securities | As per SEBI Scheme, 1997 |

🔷 4. Common Exceptions You Must Remember

| Scenario | RCM Applicable? |

|---|---|

| Recipient registered only for TDS | ❌ No |

| Supplier under composition scheme | ❌ No |

| GTA opts forward charge (5%/12%) | ❌ No |

| Author opts forward charge with declaration | ❌ No |

🔷 5. Compliance Obligations Under RCM

| Particular | Requirement |

|---|---|

| Invoice | Self-invoice if supplier unregistered |

| Tax payment | Cash only (no ITC utilisation) |

| Return | Report in GSTR-3B |

| ITC | Eligible subject to Section 16 |

| Time of supply | As per Section 13 |

🔷 6. Practical Takeaways (Finin2min Insight)

✔ RCM applies only to notified services

✔ Liability shifts to recipient, not supplier

✔ ITC is available after payment of tax

✔ Errors in RCM = interest + penalty exposure

🔷 7. One-Line Summary

If a service appears in Notification 13/2017, always check who pays GST — because under RCM, the buyer often pays.

📌 Finin2min Recommendation

Businesses should:

- Map vendors against RCM list

- Review contracts & invoices

- Ensure cash flow planning for RCM tax

- Automate RCM checks in ERP/accounting systems