How to Correct Excess Tax on Leave Encashment for AY 2025-26

🔷 1. What Changed in Law? (At a Glance)

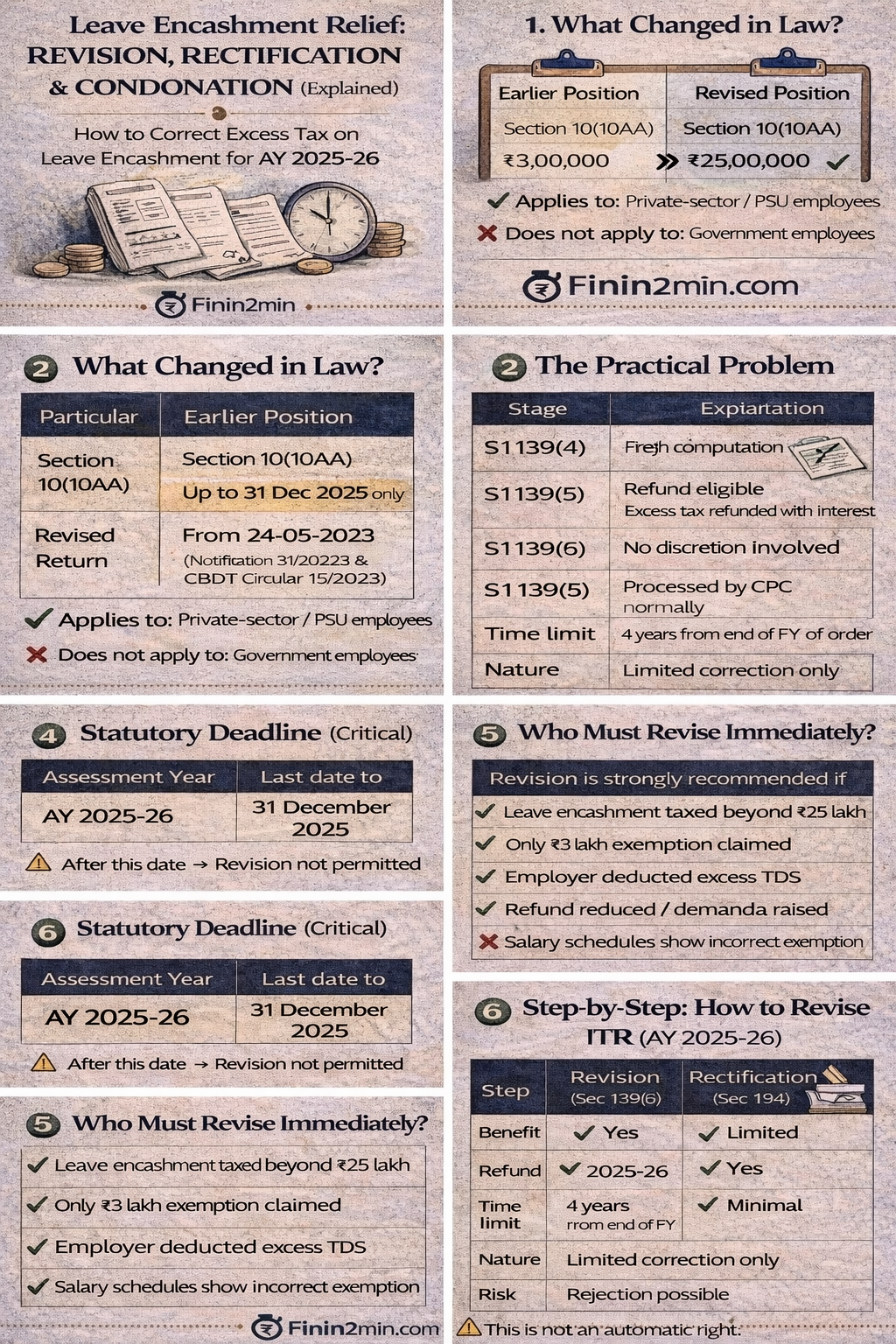

| Particular | Earlier Position | Revised Position |

|---|---|---|

| Applicable section | Section 10(10AA) | Section 10(10AA) |

| Exemption limit (non-Govt employees) | ₹3,00,000 | ₹25,00,000 |

| Effective date | Till 23-05-2023 | From 24-05-2023 onwards |

| Legal basis | Old ceiling | Notification 31/2023 + CBDT Circular 15/2023 |

✅ Applies to: Private-sector / PSU employees

❌ Does not apply to: Government employees (already fully exempt)

🔷 2. The Practical Problem

Many taxpayers for AY 2025-26 have already:

- Filed ITR using old ₹3 lakh limit

- Paid excess tax / received lower refund

- Faced incorrect TDS deduction by employer

➡ Result: Excess taxation on terminal leave encashment

🔷 3. Best Remedy Before 31 December 2025

✅ Revision of Return (Section 139(5))

Why revision is the first & fastest option

| Benefit | Explanation |

|---|---|

| Automatic correction | Fresh computation allowed |

| Refund eligible | Excess tax refunded with interest |

| No discretion involved | Processed by CPC normally |

| Least litigation risk | No approval / scrutiny stage |

🔷 4. Statutory Deadline (Critical)

| Assessment Year | Last date to revise return |

|---|---|

| AY 2025-26 | 31 December 2025 |

⚠️ After this date → Revision not permitted

🔷 5. Who Must Revise Immediately?

Revision is strongly recommended if:

✔ Leave encashment taxed beyond ₹25 lakh

✔ Only ₹3 lakh exemption claimed

✔ Employer deducted excess TDS

✔ Refund reduced / demand raised

✔ Salary schedules show incorrect exemption

🔷 6. Step-by-Step: How to Revise ITR (AY 2025-26)

| Step | Action |

|---|---|

| 1 | Login to Income-tax e-Filing Portal |

| 2 | e-File → Income-Tax Returns → Revised Return |

| 3 | Select AY 2025-26 |

| 4 | Enter original ITR acknowledgement |

| 5 | Modify salary schedule → restrict taxable leave encashment to amount exceeding ₹25,00,000 |

| 6 | Recompute tax & submit |

| 7 | Verify electronically |

📌 Refund (if any) is processed through CPC automatically.

🔷 7. What Happens If You Miss 31 December 2025?

After the revision window closes, only two fallback remedies exist, both less efficient.

🔷 8. Remedy 2 – Rectification (Section 154)

| Parameter | Details |

|---|---|

| Applicable where | Mistake apparent on record |

| Typical error | ₹3 lakh applied instead of ₹25 lakh |

| Eligible AYs (practically) | AY 2021-22 to AY 2024-25 |

| Time limit | 4 years from end of FY of order |

| Nature | Limited correction only |

| Discretion | Minimal |

📌 Cannot re-examine facts or fresh claims.

🔷 9. Remedy 3 – Condonation of Delay (Section 119(2)(b))

| Parameter | Details |

|---|---|

| Applicable for | Older AYs where revision + rectification barred |

| Typical AYs | AY 2020-21 & earlier |

| Time limit | Up to 6 years from end of AY |

| Nature | Discretionary |

| Requirement | Proof of genuine hardship |

| Risk | Rejection possible |

⚠️ This is not an automatic right.

🔷 10. Remedy Comparison Table (Quick Decision Guide)

| Criteria | Revision | Rectification | Condonation |

|---|---|---|---|

| Legal basis | Sec 139(5) | Sec 154 | Sec 119(2)(b) |

| Automatic | ✅ Yes | ⚠️ Limited | ❌ No |

| Refund possible | ✅ Yes | ✅ Yes | ✅ Yes |

| Discretion | ❌ | ⚠️ Minimal | ❌ High |

| Best use case | AY 2025-26 | AY 2021-22 to 2024-25 | Older AYs |

| Complexity | Low | Medium | High |

🔷 11. Key Takeaway (Finin2min View)

31 December 2025 is not just a deadline — it is the last clean exit.

- Revision is fastest, safest, and legally secure

- Rectification & condonation are fallback tools, not substitutes

- Delay converts a simple correction into a discretionary battle

📌 Final Recommendation

✔ If AY 2025-26 → Revise immediately

✔ If revision closed → Check rectification eligibility

✔ If both closed → Explore condonation carefully

📍 Finin2min Summary Box

Enhanced leave encashment exemption = ₹25 lakh

Missed it? Revise before 31-12-2025

After that → remedies narrow, risk increases