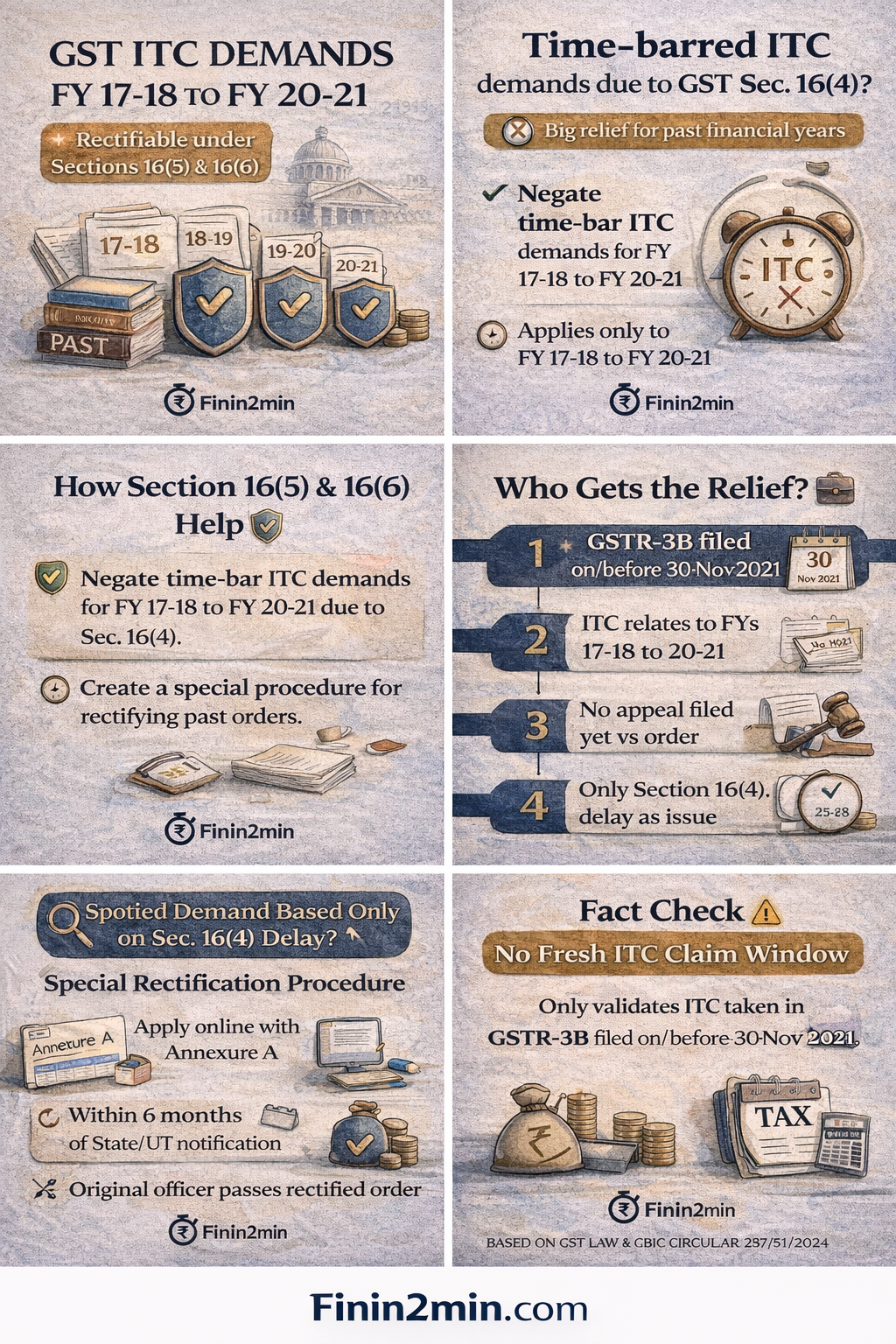

Relief for FY 2017-18 to FY 2020-21 — Law, Scope & Practical Procedure

🔔 Executive Snapshot :

- Section 16(5) retrospectively neutralises ITC demands raised only due to delay under Section 16(4) for FY 2017-18 to 2020-21, provided ITC was actually availed in a Section 39 return filed up to 30-11-2021.

- Section 16(6) grants relief in cancellation–revocation cases, within defined timelines.

- Section 148 special procedures (Central & State) operationalise rectification of already-passed orders (Sections 73/74/107/108), subject to conditions.

- No fresh ITC claim window is opened in 2025/26.

- Refund/re-credit may be restricted where tax was already paid or ITC reversed.

1️⃣ Why This Special Relief Was Needed (Legislative Trigger)

For years, tax authorities raised and confirmed demands solely on the ground that ITC was availed after the Section 16(4) cut-off—even where:

- goods/services were received,

- tax was paid by the supplier,

- ITC was actually taken in returns (Section 39).

To settle this narrow class of disputes, Parliament introduced Sections 16(5) and 16(6) (retrospective from 01-07-2017) and enabled special rectification procedures under Section 148, supplemented by CBIC Circular No. 237/31/2024-GST (15-10-2024) and corresponding State notifications (e.g., Delhi).

✔ Important: This relief targets time-bar disputes only; it does not relax other ITC conditions.

2️⃣ Statutory Framework (Section-wise)

| Provision | What it Does | Status |

|---|---|---|

| Section 16(4) | Prescribes time limit for availing ITC | Core dispute driver |

| Section 16(5) | Retrospective override for FY 2017-18 to 2020-21 | Validates past ITC |

| Section 16(6) | Relief for cancellation–revocation period | Conditional |

| Section 39 | Periodic returns (GSTR-3B) | Operative return |

| Section 148 | Power to notify special procedure | Enables rectification |

| Secs. 73/74/107/108 | Orders covered for rectification | Included |

3️⃣ Section 16(5) — Clause-by-Clause Meaning

(a) “Notwithstanding anything contained in sub-section (4)”

✔ Non-obstante override only to the time limit in Section 16(4).

❌ Does not override other Section 16 conditions (invoice, receipt, tax charged, etc.).

(b) Covered Financial Years

✔ Only FY 2017-18, 2018-19, 2019-20, 2020-21.

(c) Return under Section 39

✔ ITC must have been taken in a GSTR-3B (Section 39 return).

(d) Cut-off: “filed up to 30-11-2021”

✔ Critical condition.

- If the GSTR-3B was filed on/before 30-11-2021, ITC for the covered FYs is treated as within time, even if Section 16(4) would otherwise bar it.

- Returns filed after 30-11-2021 do not get Section 16(5) protection.

(e) Nature of Relief

✔ Validation/cure of past availed ITC — not a fresh claim window today.

4️⃣ Practical Illustrations (Client-Advisory Ready)

| Scenario | Outcome |

|---|---|

| FY 2017-18 invoice; ITC taken in Oct-2021 GSTR-3B filed 20-11-2021 | ✅ Eligible under 16(5) |

| FY 2018-19 invoice; ITC taken in Nov-2021 GSTR-3B filed 05-12-2021 | ❌ Not eligible |

| FY 2018-19 invoice; ITC never taken, attempt in 2025 | ❌ Not covered |

5️⃣ “No-Refund” Caveat (High-Stakes)

Even where Section 16(5) validates ITC:

- Refund/re-credit may be restricted if tax was already paid or ITC reversed,

- as flagged by CBIC (Finance (No. 2) Act mechanism).

Implication: Relief may neutralise demand without yielding cash refund. Case-wise analysis is essential.

6️⃣ Section 16(6) — Cancellation–Revocation Relief (Validated)

Where registration was cancelled and later revoked:

- ITC for supplies during the cancellation period may be taken:

- up to 30 November following the end of the FY, or

- within 30 days of revocation, whichever is later,

- provided the Section 16(4) time limit had not already expired on the date of cancellation.

✔ Important: This is a conditional relaxation, not a blanket waiver.

7️⃣ Section 148 Special Procedure — Why It Matters

Section 148 enables a class-based special procedure to implement relief uniformly for already-passed orders.

CBIC issued Circular 237/31/2024-GST to guide implementation; States/UTs issued parallel notifications.

8️⃣ Delhi Notification No. 22/2024 – State Tax (01-12-2025) — What It Provides

(a) Eligible Cases

All conditions must be met:

- Order under Sections 73/74/107/108 exists;

- ITC disallowed only due to Section 16(4);

- ITC now eligible under Section 16(5)/(6);

- No appeal filed against the order.

(b) Time Limit to Apply

- Within 6 months from 01-12-2025

→ Practical outer date: 31-05-2026 (subject to official computation).

(c) Application & Annexure

- Electronic application on portal;

- Annexure-A with:

- Order details,

- Year-wise breakup,

- Portion eligible under 16(5)/(6),

- Declaration (no appeal pending).

(d) Officer & Timeline

- Original adjudicating authority to pass rectified order,

- Within ~3 months (directory).

(e) Portal Trail

- 73/74 rectification → FORM GST DRC-08

- 107/108 rectification → FORM GST APL-04

(f) Limited Scope

- Only the Section 16(4) portion is rectified.

- No reopening of other issues.

(g) Natural Justice

- If rectification is adverse, hearing required.

9️⃣ What This Relief Does — and Does Not Do (Chart)

| Aspect | Position |

|---|---|

| Fresh ITC claim today | ❌ Not allowed |

| Validate past ITC (filed ≤ 30-11-2021) | ✅ Allowed |

| Reopen merits (receipt, invoice, tax paid) | ❌ No |

| Neutralise 16(4)-only demands | ✅ Yes |

| Guarantee refund | ❌ Not guaranteed |

1️⃣0️⃣ Compliance Checklist

- ✔ Identify orders solely based on Section 16(4)

- ✔ Verify GSTR-3B filing date ≤ 30-11-2021

- ✔ Segregate eligible ITC portion

- ✔ Ensure no appeal pending (or assess strategy)

- ✔ File application within limitation

- ✔ Evaluate refund vs neutralisation impact

🧾 Conclusion

Sections 16(5) and 16(6) were enacted to settle legacy ITC disputes where credit was denied only due to time-bar under Section 16(4).

If ITC for FY 2017-18 to 2020-21 was actually availed in a Section 39 return filed up to 30-11-2021, such credit is statutorily validated, and demands based solely on delay become rectifiable through the Section 148 special procedure (e.g., Delhi’s notification).

Relief is targeted and conditional—with no fresh claim window and possible refund restrictions where tax has already been paid.