(Updated with CGST Act, CGST Rules & GSTAT (Procedure) Rules, 2025)

The Goods and Services Tax Appellate Tribunal (GSTAT) has been operationalised pursuant to Section 109 and Section 112 of the CGST Act, 2017.

To regulate its functioning, the Central Government has notified the Goods and Services Tax Appellate Tribunal (Procedure) Rules, 2025, vide Notification dated 24 April 2025, issued under Section 111 of the CGST Act, 2017.

This article provides a comprehensive and practical guide to filing appeals before GSTAT, read together with the CGST Act, 2017 and CGST Rules, 2017, with practitioner-friendly charts and summaries.

1️⃣ Statutory Framework — GST Law Alignment

| Law / Rule | Subject |

|---|---|

| Section 112, CGST Act | Appeal to Appellate Tribunal |

| Section 109, CGST Act | Constitution of GSTAT |

| Section 111, CGST Act | Power to frame procedure rules |

| Rule 110, CGST Rules | Form, manner & fees of appeal |

| Rule 18, GSTAT Rules, 2025 | Filing & structure of appeal |

| FORM GST APL-05 | Prescribed appeal form |

Legal position:

An appeal to GSTAT is a statutory remedy, not discretionary, but must strictly comply with procedural law.

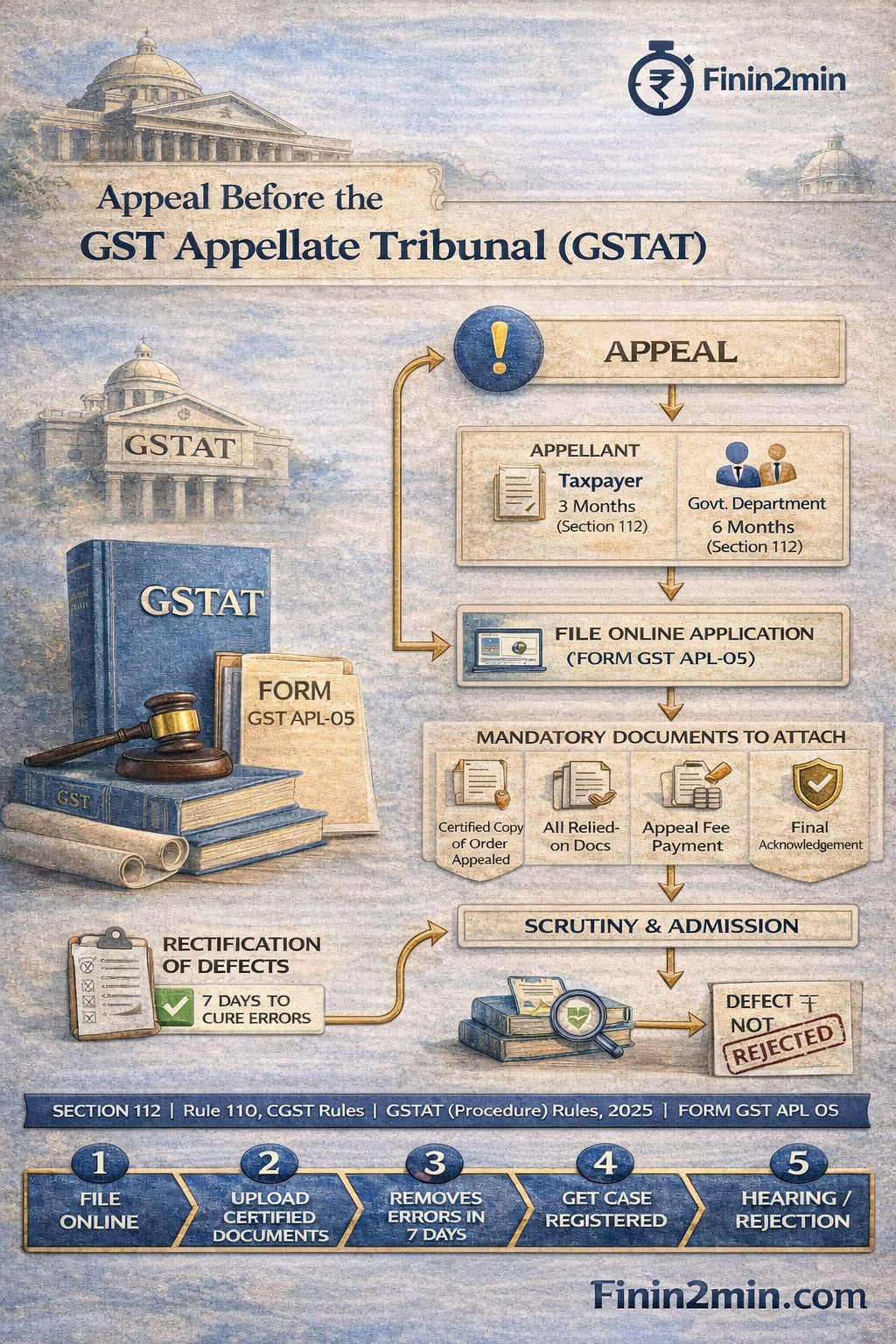

2️⃣ Right to Appeal & Time Limits (Section 112)

Who can appeal?

- Any person aggrieved by an order of the Appellate Authority under:

- Section 107 (First Appeal)

- Revisionary orders under Section 108

Time limit

| Appellant | Time limit |

|---|---|

| Taxpayer | 3 months from communication of order |

| Department | 6 months from communication |

⏳ Delay may be condoned by GSTAT on sufficient cause being shown.

3️⃣ Mandatory Electronic Filing (CGST Rules + GSTAT Rules)

Legal mandate

- Rule 110(1), CGST Rules, 2017

- Rule 18, GSTAT (Procedure) Rules, 2025

Appeal must be filed electronically only on the GSTAT Portal.

Prescribed Form

➡ FORM GST APL-05

Physical or offline filing is not valid.

4️⃣ Drafting & Structure of Appeal (Rule 18, GSTAT Rules)

Mandatory elements

| Requirement | Legal Source |

|---|---|

| Cause title: “In the GST Appellate Tribunal” | Rule 18 |

| Reference to impugned order | Rule 18 |

| Numbered paragraphs | Rule 18 |

| One issue per paragraph | Rule 18 |

| Full party particulars | Rule 18 |

| Fixed party numbering | Rule 18 |

Party numbering remains unchanged even if legal heirs are substituted.

5️⃣ Prescribed Appeal Format (Illustrative)

IN THE GOODS AND SERVICES TAX APPELLATE TRIBUNAL

Appeal under Section 112 of the CGST Act, 2017

[Name of Appellant]

S/o / D/o / W/o ______

GSTIN: ______

Address: ______…Appellant

Versus

- [Name of Respondent Authority]

Designation: ______

Office Address: ______…Respondent

6️⃣ One Appeal vs Multiple Appeals — GST Law Position

✅ One Appeal Sufficient (Rule 18(2))

Where one appellate order covers:

- Multiple SCNs

- Multiple demands

- Multiple refund issues

➡ Single appeal in FORM GST APL-05

❌ Separate Appeals Mandatory (Rule 18(3))

| Situation | Requirement |

|---|---|

| One appellate order covers multiple original orders | Separate appeals |

| One order affects multiple persons | Each person files separately |

| Joint / common appeal | Not permitted |

7️⃣ Grounds of Appeal & Presentation (Rule 20)

Grounds of Appeal

- Clear and concise

- Each ground under a separate heading

- Consecutively numbered

Formatting standards

| Parameter | Requirement |

|---|---|

| Spacing | Double-spaced |

| Paper | A4 |

| Pagination | Mandatory |

| Indexing | Mandatory |

| Binding | Properly tagged |

Applies to:

- Appeals

- Stay applications

- Cross-objections

- Miscellaneous applications

8️⃣ Verification, Signing & Certification

Who can sign?

- Appellant / Respondent

- Authorised Representative (Section 116, CGST Act)

Certification

- Documents must be certified as true copies

Improper verification = defective appeal

9️⃣ Mandatory Documents (Rule 21 + CGST Rules)

Documents to be uploaded

| Nature of Appeal | Documents |

|---|---|

| Against original order | Certified copy of original order |

| Against appellate/revisional order | Certified copy of appellate + original order |

| Commissioner-directed appeal | Attested copy sufficient |

All relied-upon documents must be uploaded.

🔟 Appeal Fee & Acknowledgement

Appeal Fee (Rule 110(5), CGST Rules)

- Fee linked to amount of tax in dispute

- Paid electronically on portal

Acknowledgement

- Portal generates final acknowledgement

- Appeal number assigned post-admission

1️⃣1️⃣ Defective Filing & Rectification (Rule 24)

| Stage | Authority | Timeline |

|---|---|---|

| Scrutiny | Registrar / Authorised officer | — |

| Rectification | Appellant | 7 working days |

| Extension | Registrar | Up to 30 days |

| Non-compliance | Bench | May reject |

Appeal may get a fresh number after rectification.

1️⃣2️⃣ Translation of Documents (Rule 23)

- Documents not in English must be:

- Translated into English

- Certified by authorised representative

- Matter will not be listed until compliance

1️⃣3️⃣ Registration of Appeals (Rule 25)

- On admission:

- Appeal is registered

- Appeal number allotted

- Index updated in Tribunal register

1️⃣4️⃣ Grounds at Hearing — Natural Justice (Rule 31)

- Appellant generally restricted to stated grounds

- Additional grounds only with leave of Tribunal

- Tribunal may consider other grounds only after hearing parties

Ensures compliance with principles of natural justice.

1️⃣5️⃣ Proper Respondents (Rule 33)

| Appellant | Mandatory Respondent |

|---|---|

| Taxpayer | Concerned Commissioner |

| Commissioner | Other party |

1️⃣6️⃣ Service of Copies (Rule 34)

- Copy of appeal + documents must be served on:

- Respondent

- Concerned Commissioner

- Immediately after filing

1️⃣7️⃣ Affidavits (Rules 78–80)

- Title: Before the Goods and Services Tax Appellate Tribunal

- Must comply with Order XIX, CPC

- Sworn before:

- Advocate or

- Notary (with seal)

📊 GSTAT Appeal Lifecycle — Summary Chart

| Stage | Governing Law |

|---|---|

| Right to appeal | Section 112, CGST Act |

| Filing & form | Rule 110, CGST Rules |

| Procedure | GSTAT Rules, 2025 |

| Scrutiny | Rule 24 |

| Admission & registration | Rule 25 |

| Hearing | Rules 31–34 |

| Decision | Section 112 |

✅ Practitioner Checklist

✔ Check limitation under Section 112

✔ Verify correct appellate order

✔ File FORM GST APL-05 only online

✔ Upload certified copies

✔ Ensure indexing & pagination

✔ Translate non-English documents

✔ Serve copies to respondent

✔ Cure defects within timelines

🔚 Final Takeaway

Appeals before GSTAT are procedural-intensive and strictly digital.

Failure to comply with CGST Rules + GSTAT Rules can result in rejection at threshold, irrespective of merits.