🔹 Executive Summary (At a Glance)

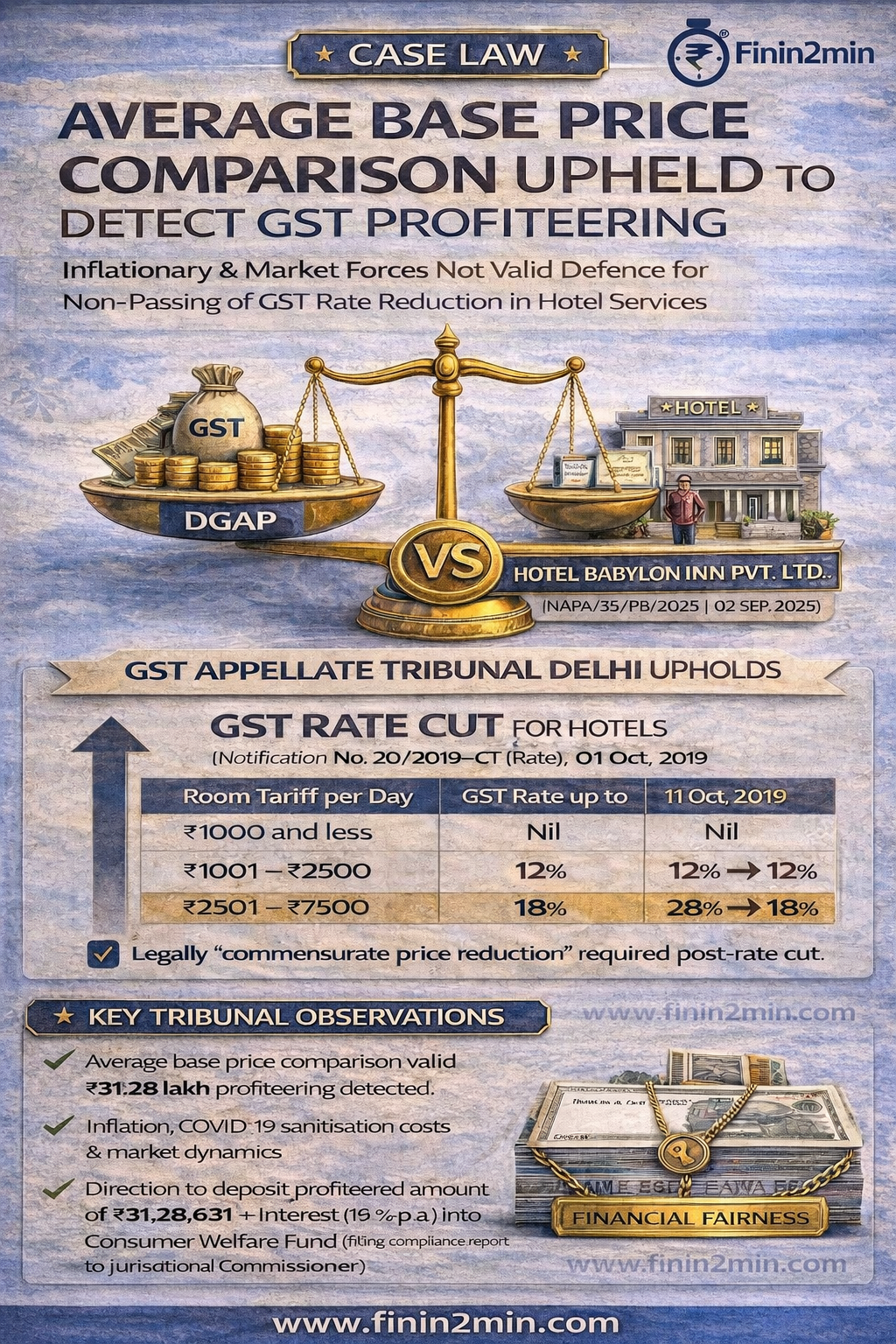

The GST Appellate Tribunal, Delhi in DGAP v. Hotel Babylon Inn Pvt. Ltd.

[NAPA/35/PB/2025 | Order dated 02 September 2025] held that:

- Hotels must pass on GST rate reduction benefits through price reduction

- Average base price comparison is a valid method to compute profiteering

- Inflation, COVID-19 costs, seasonality & market forces are not valid defences

- ₹31.28 lakh profiteered amount + 18% interest ordered to be deposited in Consumer Welfare Fund

- Inflationary & Market Forces not a Valid defense for Non-Passing of GST Rate Reduction on Hotel Services

The ruling reinforces the strict consumer-centric intent of Section 171 of the CGST Act.

🔹 Background of the Case

Parties

- Appellant: Directorate General of Anti-Profiteering (DGAP)

- Respondent: Hotel Babylon Inn Pvt. Ltd.

Trigger for Investigation

DGAP initiated proceedings alleging that the Respondent failed to pass on GST rate reduction benefits on hotel accommodation services effective from 1 October 2019, despite a statutory rate cut.

🔹 GST Rate Reduction on Hotel Accommodation

📊 GST Rate Change (Notification No. 20/2019–CT (Rate), dated 30.09.2019)

| Room Tariff per Day | GST Rate up to 30.09.2019 | GST Rate from 01.10.2019 |

|---|---|---|

| ₹1,000 or less | Nil | Nil |

| ₹1,001 – ₹2,500 | 12% | 12% |

| ₹2,501 – ₹7,500 | 18% | 12% ⬇️ |

| ₹7,501 and above | 28% | 18% ⬇️ |

➡️ Statutory expectation: Prices must reduce commensurately post-rate cut.

🔹 Allegations by DGAP

- Hotel tariffs remained unchanged post-GST rate reduction

- Base prices were effectively increased

- DGAP used average base price comparison methodology

- Profiteering quantified at ₹31,28,631

🔹 Respondent’s Defence

The Respondent argued:

- Hotel pricing depends on market forces & seasonal demand

- COVID-19 sanitisation & operational costs increased prices

- GST was charged separately, hence benefit passed

- Room tariffs fluctuate daily, making comparisons unreliable

- Average base price methodology was incorrect

🔹 Issues for Consideration

- Whether the Respondent profiteered by not passing GST rate reduction?

- Whether average base price comparison is a valid methodology?

- Whether inflation, COVID costs, and market dynamics justify non-passing of benefit?

🔹 Tribunal’s Findings & Analysis

1️⃣ GST Rate Reduction Not Passed On

- Tribunal observed that tariffs were not reduced despite lower GST

- Section 171 mandates actual price reduction, not mere tax disclosure

2️⃣ Average Base Price Comparison is Valid

The Tribunal upheld DGAP’s methodology:

- Comparison of average base prices pre- and post-rate reduction

- Appropriate where:

- Transaction values vary

- Prices are dynamic (hotels, airlines, e-commerce)

“The methodology adopted by DGAP is reasonable, scientific and aligned with the statutory mandate.”

3️⃣ Market Forces & COVID Arguments Rejected

The Tribunal categorically rejected the Respondent’s defence:

- Inflation & sanitisation costs were unsupported by documentary evidence

- Market dynamics defence termed an: “afterthought and a castle built in air”

- Commercial hardships cannot override statutory obligations

4️⃣ Strict Interpretation of Section 171

Relying on Reckitt Benckiser India Pvt. Ltd. v. Union of India

[2024 SCC Online Del 588], the Tribunal held:

- There is a rebuttable presumption of profiteering if prices are not reduced

- Burden lies on the supplier to prove benefit was passed

🔹 Final Directions of the Tribunal

| Particular | Direction |

|---|---|

| Profiteered Amount | ₹31,28,631 |

| Interest | 18% p.a. |

| Period | From 01.10.2019 till realisation |

| Deposit | Consumer Welfare Fund |

| Compliance | Report to be filed by Jurisdictional Commissioner |

🔹 Legal Provisions Involved

📜 Section 171 – CGST Act, 2017

Mandates passing of:

- GST rate reduction

- ITC benefit

by way of commensurate price reduction

📜 Rule 133(3) – CGST Rules, 2017

Authorises:

- Recovery of profiteered amount

- Interest @ 18%

- Deposit into Consumer Welfare Fund

🔹 Our Commentary & Practical Impact

🔍 Key Takeaways for Hospitality Industry

| Aspect | Tribunal’s View |

|---|---|

| Dynamic pricing | Not a defence |

| COVID cost escalation | Must be proven |

| GST shown separately | Not sufficient |

| Price comparison | Average base price valid |

| Consumer benefit | Mandatory |

🔹 Compliance Lessons

✔ Document cost increases with verifiable data

✔ Re-work pricing immediately after GST changes

✔ Maintain audit-ready pricing justification

✔ Avoid post-rate base price escalation

🔹 Conclusion

This ruling strengthens the anti-profiteering jurisprudence by confirming that:

- Economic hardship does not dilute statutory consumer protection

- Hotels and service providers must ensure real benefit transfer

- Average base price comparison remains a robust compliance benchmark

Failure invites financial recovery, interest, and reputational risk.