🔹 Executive Summary (Quick Read)

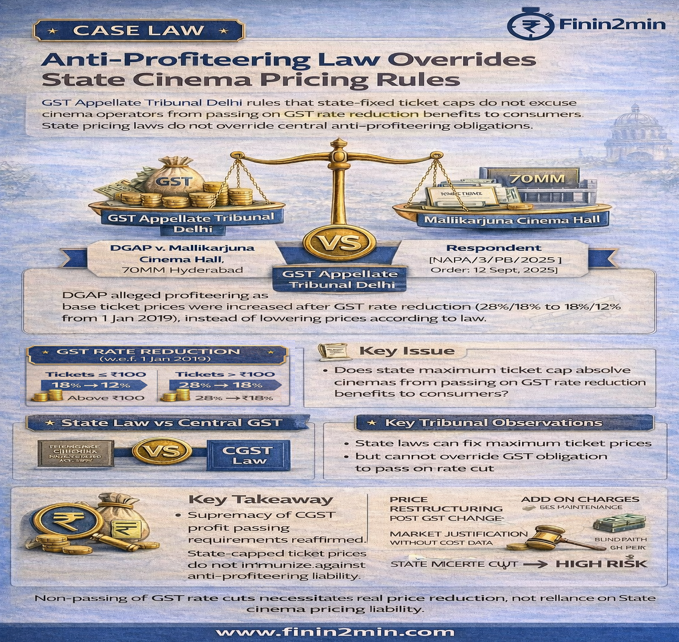

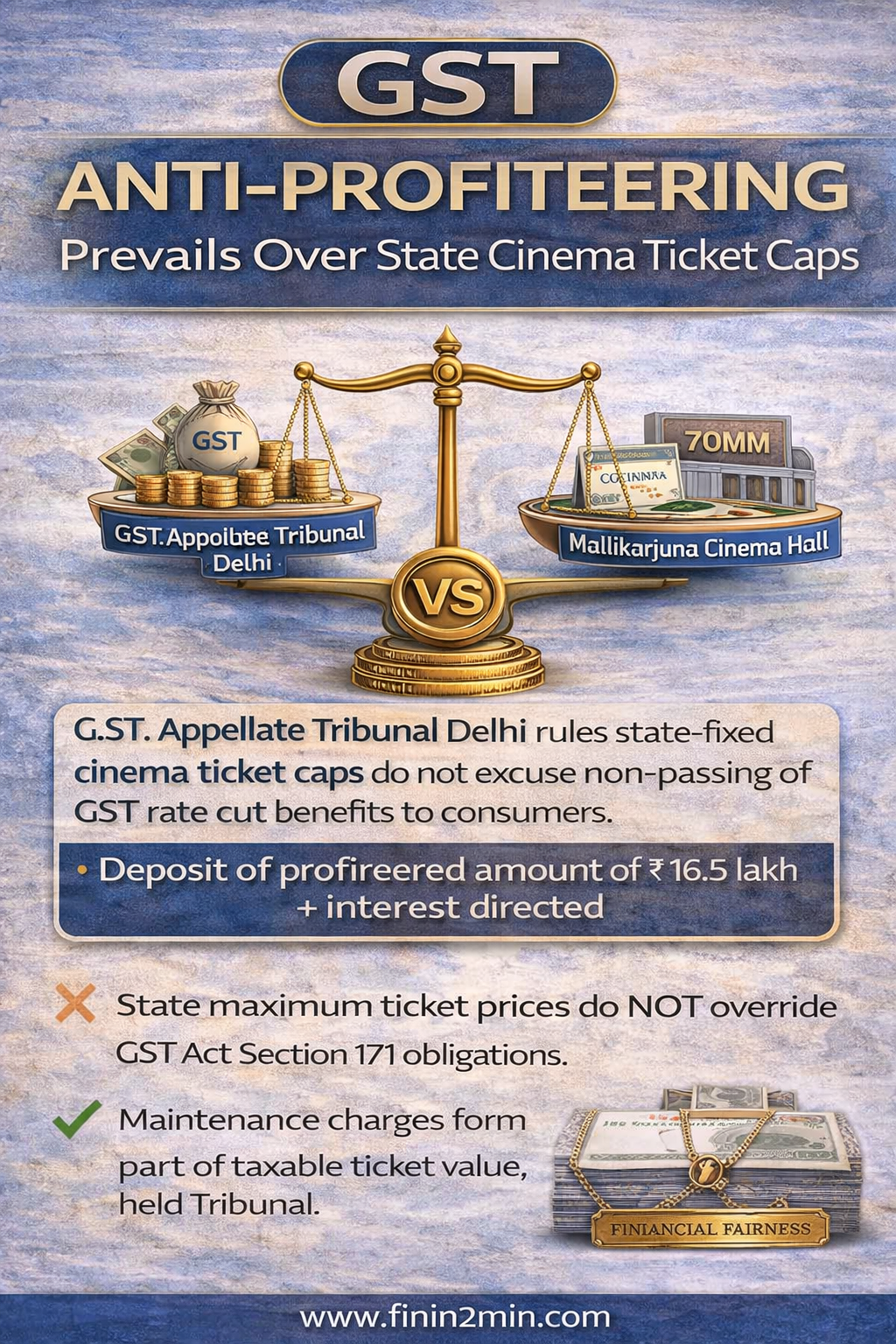

The GST Appellate Tribunal, Delhi in DGAP v. Mallikarjuna Cinema Hall, 70MM Hyderabad

[NAPA/3/PB/2025 | Order dated 12 September 2025] held that:

- State-fixed cinema ticket caps do not override GST anti-profiteering obligations

- GST rate reduction benefits must be passed on to consumers

- Maintenance charges form part of taxable value

- Market forces or commercial justifications cannot excuse profiteering

- Profiteered amount of ₹16.50 lakh + interest directed to be deposited

This ruling reinforces the supremacy of Central GST law over State pricing regulations.

🔹 Background of the Case

Parties Involved

- Appellant: Directorate General of Anti-Profiteering (DGAP)

- Respondent: Mallikarjuna Cinema Hall, 70MM, Hyderabad

Trigger for Investigation

The DGAP initiated proceedings alleging that the Respondent failed to pass on GST rate reduction benefits on cinema tickets following the GST rate cut effective from 1 January 2019.

🔹 GST Rate Reduction on Cinema Tickets

| Period | Ticket Price Category | GST Rate |

|---|---|---|

| Pre-1 Jan 2019 | Above ₹100 | 28% |

| Pre-1 Jan 2019 | Up to ₹100 | 18% |

| Post-1 Jan 2019 | Above ₹100 | 18% |

| Post-1 Jan 2019 | Up to ₹100 | 12% |

Notification: No. 27/2018–CT (Rate) dated 31 December 2018

🔹 Respondent’s Defence

The cinema hall argued that:

- Ticket prices were fixed under the Telangana Cinemas (Regulation) Act, 1955

- Prices were charged with express approval of State authorities

- Maintenance charges were tax-free and wrongly included

- Market dynamics and operational costs justified pricing

- Section 171 allows flexibility under the word “commensurate”

🔹 DGAP’s Findings

Based on actual ticket sales data, DGAP found that:

- Base ticket prices were increased after GST rate reduction

- Consumers did not receive proportional price benefit

- Profiteering was quantified at ₹16,50,166

- Methodology was not disputed by the Respondent

📌 Crucial Admission:

The Respondent admitted attempting to retain additional profit due to tax reduction.

🔹 Issues for Determination

- Whether the Respondent profiteered by not passing GST rate reduction benefits?

- Whether State-fixed ticket price caps override Section 171 of CGST Act?

- Whether maintenance charges can be excluded from taxable value?

🔹 Tribunal’s Ruling & Key Observations

1️⃣ State Pricing Law vs GST Anti-Profiteering

- State laws only fix maximum prices, not mandatory prices

- Cinema owners retain pricing discretion

- Section 171 of CGST Act prevails over State legislation

“State-fixed maximum pricing does not dilute the obligation to pass on tax benefits.”

2️⃣ Maintenance Charges Are Taxable

- Maintenance charges are inseparable from ticket price

- Any amount collected for admission forms part of taxable value

- Central GST law takes precedence

3️⃣ Market Factors Defence Rejected

The Tribunal relied on:

Reckitt Benckiser India Pvt. Ltd. v. Union of India

[2024 SCC Online Del 588]

Holding that:

- “Market conditions” must be proved with cost data

- Cannot be used as a blanket excuse to deny statutory benefit

4️⃣ Admission Equals Proof

“Admissions, if clear and unambiguous, are the best proof of fact admitted.”

The Respondent’s own admission established profiteering conclusively.

🔹 Final Directions of the Tribunal

| Particular | Direction |

|---|---|

| Profiteered Amount | ₹16,50,166 |

| Interest | 18% (pro-rata) |

| Deposit | 50% to Central CWF + 50% to State CWF |

| Timeline | Within 1 month |

| Compliance Report | Within 4 months |

🔹 Prospective Application of Interest

The Tribunal examined whether interest liability is retrospective and held:

- Interest provision applies prospectively

- Relied on Vatika Township (SC Constitution Bench)

(2015) SCC 1 - No retrospective penal effect unless expressly stated

🔹 Legal Framework Involved

Key Provisions

- Section 171, CGST Act, 2017 – Anti-profiteering

- Rule 133(3), CGST Rules, 2017 – Powers of Authority

- Notification 27/2018–CT (Rate) – GST rate cut

- Section 9A, Telangana Cinemas Act, 1955 – Ticket price caps

🔹 Our Analysis & Commentary

🔸 Key Takeaways

✔ Anti-profiteering law overrides State pricing controls

✔ Pricing discretion brings tax compliance responsibility

✔ Charges by any name (maintenance, convenience, etc.) are taxable

✔ Admissions significantly weaken defence

✔ Reckitt Benckiser now a binding benchmark

🔹 Compliance Lessons for Businesses

| Area | Risk |

|---|---|

| Price restructuring post-GST change | High |

| Add-on charges | Taxable |

| Market justification without data | Rejected |

| State law reliance | Not sufficient |

🔹 Conclusion

This ruling reinforces that GST anti-profiteering provisions operate independently of State price regulations. Businesses must ensure real, measurable price reductions whenever GST benefits accrue.

Failure to do so invites recovery, interest, and reputational risk.