Detailed Comparison

Since its introduction in Budget 2020, India’s New Tax Regime has evolved through multiple amendments and rate revisions.

As of FY 2025–26 (AY 2026–27), both regimes are still available, but with key differences in tax rates, exemptions, and compliance ease.

This article analyses both systems side-by-side with real calculation examples, data tables, and recommendations for salaried and business taxpayers.

Historical Background

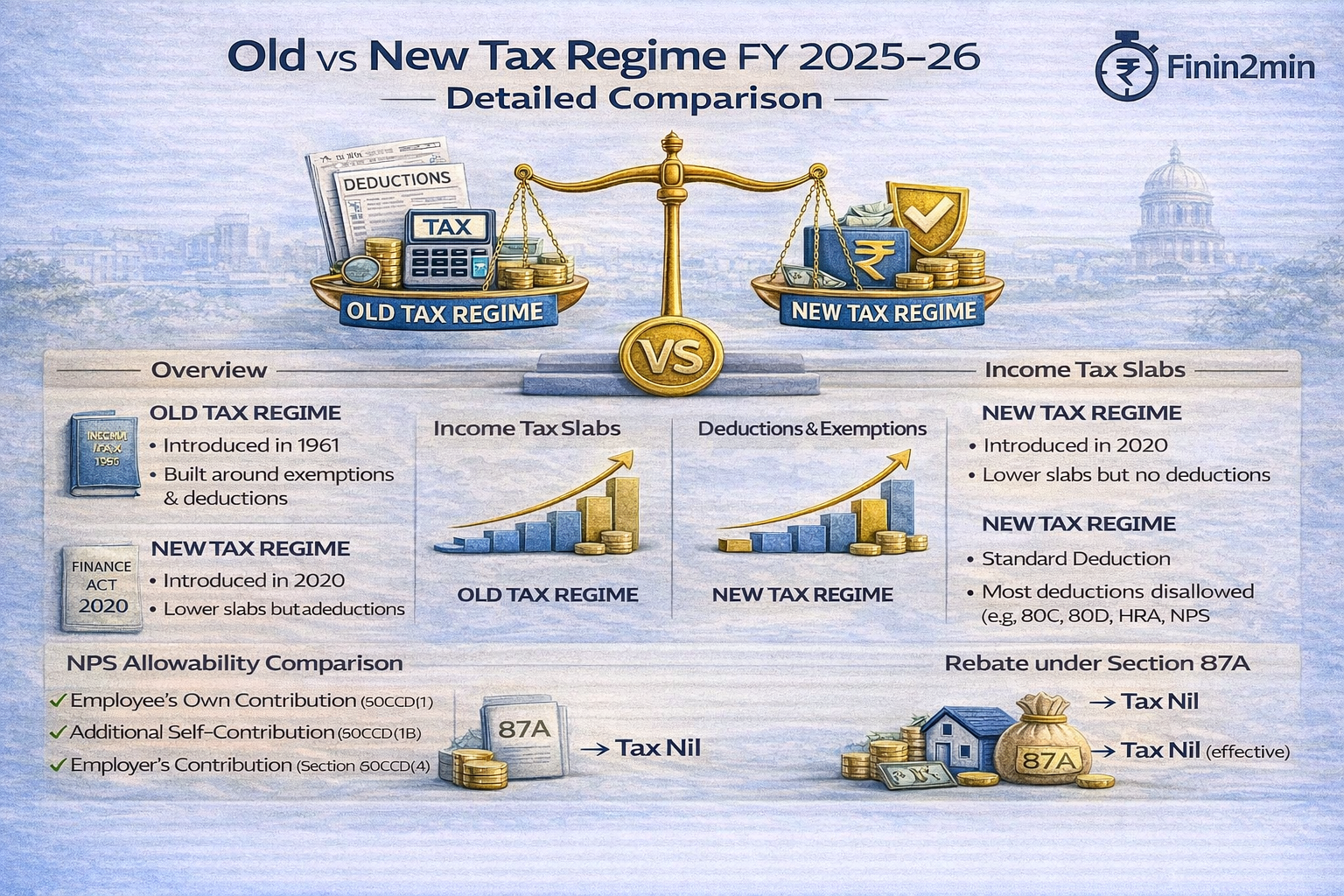

- Old Tax Regime:

In place since 1961, built around tax exemptions and deductions (like 80C, 80D, HRA, LTA, etc.).

Encourages savings through tax planning. - New Tax Regime (Section 115BAC):

Introduced via the Finance Act, 2020 to simplify taxation.

Offers lower slab rates but no exemptions.

Became default regime from FY 2023–24 as per Budget 2023.

1️⃣ Tax Slabs for FY 2025-26 (AY 2026-27)

🔹 New Tax Regime Rates

Under the New Regime, the income slabs and tax rates are:

| Income Range (₹) | Tax Rate |

|---|---|

| 0 – 4,00,000 | Nil |

| 4,00,001 – 8,00,000 | 5% |

| 8,00,001 – 12,00,000 | 10% |

| 12,00,001 – 16,00,000 | 15% |

| 16,00,001 – 20,00,000 | 20% |

| 20,00,001 – 24,00,000 | 25% |

| Above 24,00,000 | 30% |

Standard Deduction (New Regime): ₹75,000 allowed.

Rebate (Section 87A): Up to ₹12 lakh taxable income → tax zero (max ₹60,000 relief).

2️⃣ Old Tax Regime Rates ( unchanged )

For FY 2025-26 under the Old Regime, the slabs are (general individual):

| Income Range (₹) | Tax Rate |

|---|---|

| 0 – 2,50,000 | Nil |

| 2,50,001 – 5,00,000 | 5% |

| 5,00,001 – 10,00,000 | 20% |

| Above 10,00,000 | 30% |

Standard Deduction (Old Regime): ₹50,000 (salary only).

Rebate (Section 87A): Up to ₹5 lakh → tax zero* (₹12,500 max).

* Rebate under old regime is limited and less generous than new regime rebate.

3️⃣ Key Difference — Deductions & Exemptions

| Feature | Old Regime | New Regime |

|---|---|---|

| Standard Deduction | ₹50,000 | ₹75,000 |

| Section 80C (PPF, ELSS, etc.) | Allowed (₹1.5L) | Not Allowed |

| Section 80D (Health Insurance) | Allowed | Not Allowed |

| HRA, LTA | Allowed | Not Allowed |

| Home Loan Interest (Section 24) | Allowed | Not Allowed |

| Other 80D/80CCD/80U | Allowed | Not Allowed |

| Rebate (87A) | ₹5 L ₹12,500* | ₹12 L ₹60,000 |

NPS Allowability Comparison — Validated for FY 2025–26 (AY 2026–27)

| Tax Benefit Component | Old Tax Regime | New Tax Regime |

|---|---|---|

| Employee’s Own Contribution (Section 80CCD(1)) | ✅ Deductible within the overall ₹1.5 lakh limit of Section 80C/80CCE (up to 10% of salary or 20% of GTI for self-employed). | ❌ Not available |

| Additional Self-Contribution (Section 80CCD(1B)) | ✅ Additional deduction up to ₹50,000, over and above the ₹1.5 lakh limit. | ❌ Not available |

| Employer’s Contribution (Section 80CCD(2)) | ✅ Deductible up to: • 10% of salary (Basic + DA) for private-sector employees • 14% of salary for Government employees | ✅ Deductible up to 14% of salary (Basic + DA) for all employees (private & government) |

4️⃣ What This Means — Practical Impact

🧮 Example Scenario

Let’s consider a salary of ₹12,00,000:

- In the New Regime, large standard deduction of ₹75,000 + full rebate means effectively zero tax for incomes ≤ ₹12 lakh.

- In the Old Regime, even with deductions, total tax often remains higher unless total deductions exceed ₹3 L–₹4 L.

Thus new regime has become highly beneficial for middle-income taxpayers up to ₹12 lakh, especially if they do not have big investments to claim under 80C/80D.

5️⃣ When Old Regime Might Still Win

Choose Old Regime if:

✔ You have high deductions/exemptions (80C, 80D, Section 24 home loan)

✔ Your total deductions exceed the benefit of slab relief under new regime

✔ You want to plan long-term tax savings via structured investments

Despite new regime’s simplicity, old regime still offers better tax optimization for deduction-heavy taxpayers.

6️⃣ Rebate & Tax-Free Thresholds

- New Regime: Up to ₹12 lakh income is effectively tax-free due to rebate under Section 87A and the ₹75,000 standard deduction.

- Old Regime: Up to ₹5 lakh income is effectively tax-free with rebate limit ₹12,500 and standard deduction ₹50,000.

This fundamental difference makes the new regime much more taxpayer-friendly for common individual taxpayers.

7️⃣ Recommendations — FY 2025-26

✅ Income ≤ ₹12 L without heavy deductions:

👉 New Regime is likely better.

✅ Income > ₹12 L with significant 80C/80D/Section 24 benefits:

👉 Old Regime may still save more.

In general, the new regime has become the default and tax-efficient choice for most salaried taxpayers.

💬 FAQs

1. Can I switch tax regimes every year?

✔ Yes — salaried individuals can choose their regime at each ITR filing.

2. Is the New Regime compulsory?

✔ No — the New Regime is default, but you can opt for Old Regime.

3. Are HRA and 80C allowed in New Regime?

❌ No — these exemptions are not available under the new slab structure.

4. Does rebate apply to capital gains?

❌ No — Section 87A rebate applies only to regular income, not STCG/LTCG.