Using a Hindu Undivided Family Correctly & Avoiding Clubbing

(Finin2min | Direct Tax Explainer)

1️⃣ WHAT IS AN HUF? (LEGAL POSITION)

| Aspect | Position under Income Tax |

|---|---|

| Status | Separate taxable person |

| Governing law | Hindu law + Income-tax Act |

| Covered families | Hindus, Jains, Sikhs, Buddhists |

| Tax return | Separate ITR required |

| PAN | Mandatory |

| Bank account | Mandatory (separate) |

📌 Key Point:

An HUF exists by status, but tax benefits arise only after formalisation.

2️⃣ STRUCTURE OF AN HUF

| Role | Explanation |

|---|---|

| Karta | Head of HUF (usually eldest coparcener) |

| Coparceners | Members by birth (sons & daughters) |

| Members | Spouse, daughter-in-law, etc. |

| Decision making | Karta manages HUF affairs |

📌 Daughters are equal coparceners after Hindu Succession (Amendment) Act.

3️⃣ BASIC COMPLIANCE CHECKLIST (NON-NEGOTIABLE)

| Step | Mandatory? |

|---|---|

| HUF Deed | ✔ Recommended |

| PAN in HUF name | ✔ Mandatory |

| Bank account (HUF) | ✔ Mandatory |

| Separate books / records | ✔ Essential |

| Independent investments | ✔ Essential |

⚠️ Paper-only HUFs fail scrutiny.

4️⃣ WHY HUF IS USED FOR TAX PLANNING

| Benefit Area | How HUF Helps |

|---|---|

| Basic exemption | Separate threshold available |

| Capital gains | Separate exemption limits |

| Rental income | Taxed in HUF, not individual |

| Business income | Permitted if genuine |

| Investments | Separate portfolio |

📌 Threshold-based benefits apply separately only if income source is valid.

5️⃣ WHAT AN HUF CAN DO (VALID ACTIVITIES)

| Activity | Allowed? |

|---|---|

| Hold ancestral property | ✔ Yes |

| Earn rent | ✔ Yes |

| Invest in shares / MFs | ✔ Yes |

| Earn interest | ✔ Yes |

| Capital gains | ✔ Yes |

| Run business | ✔ Yes (with genuine capital) |

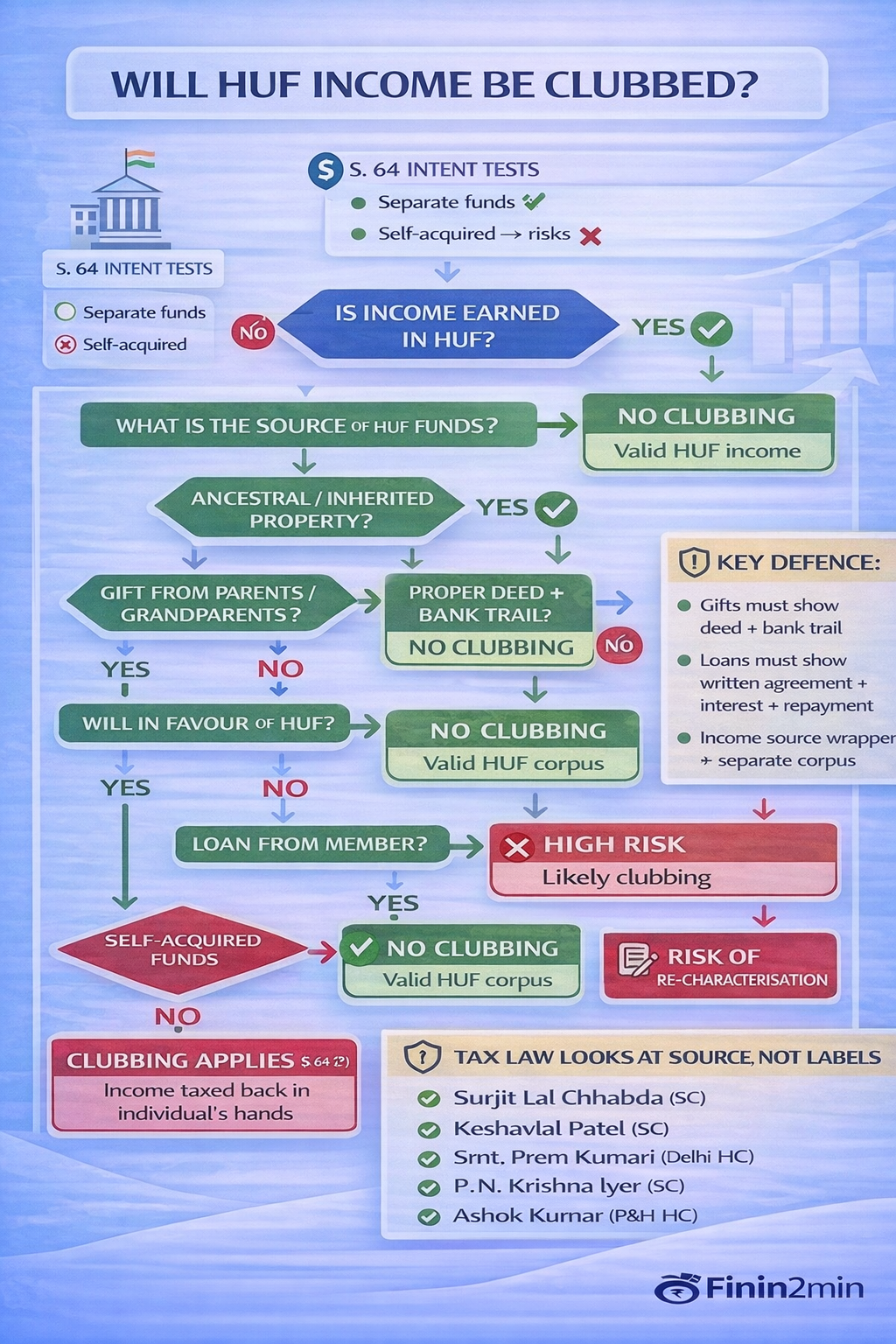

6️⃣ FUNDING THE HUF — MOST CRITICAL AREA

✅ ACCEPTABLE SOURCES (LOW RISK)

| Source | Tax Position |

|---|---|

| Ancestral / inherited property | ✔ Safe |

| Income from ancestral property | ✔ Safe |

| Gifts from parents / grandparents | ✔ With documentation |

| Will in favour of HUF | ✔ Strong |

| Loan from members | ✔ If properly structured |

❌ HIGH-RISK SOURCES (CLUBBING APPLIES)

| Source | Consequence |

|---|---|

| Self-acquired funds of Karta | ❌ Income gets clubbed |

| Asset transfer without consideration | ❌ Section 64 applies |

| Informal cash transfer | ❌ High litigation risk |

📌 Key Law Trigger (Section 64):

If a member transfers separate property to HUF, income is clubbed back.

7️⃣ SAFER ALTERNATIVE: MEMBER → HUF LOAN

| Requirement | Best Practice |

|---|---|

| Loan agreement | Written |

| Interest rate | Reasonable |

| Repayment schedule | Defined |

| Bank trail | Mandatory |

| Accounting | Proper entries |

✔ Loan interest is taxable in lender’s hands

✔ HUF income remains separate

8️⃣ OPERATIONAL DISCIPLINE (OFTEN MISSED)

| Area | What to Do |

|---|---|

| Banking | No personal use of HUF funds |

| Withdrawals | Proper resolutions & entries |

| Investments | In HUF name only |

| Records | Maintain gift deeds, wills, loan docs |

| Karta actions | Document decisions |

⚠️ Mixing personal & HUF money kills the structure.

9️⃣ BENEFITS NOT AVAILABLE TO HUF (IMPORTANT)

| Provision | Applicability |

|---|---|

| Individual rebates (e.g. Sec 87A) | ❌ Not available |

| Individual-specific deductions | ❌ If wording restricts |

| Assumptions of parity | ❌ Incorrect |

📌 Always read wording:

“An assessee, being an individual resident in India…”

🔟 COMMON MISTAKES SEEN IN SCRUTINY

| Mistake | Result |

|---|---|

| Creating HUF only for tax saving | Disallowed |

| No valid corpus source | Clubbing |

| No bank separation | Adverse inference |

| Using HUF funds personally | Litigation |

| No documentation | Additions & penalty |

🔚 FININ2MIN TAKEAWAY

| Principle | Why It Matters |

|---|---|

| HUF is a separate person | But not a loophole |

| Source of funds matters | More than paperwork |

| Documentation is critical | Defence in scrutiny |

| Compliance first | Tax saving follows |

| Casual structuring fails | Clubbing neutralises benefit |

📌 FINAL WORD

HUF planning works only when it is real, funded correctly, and run like a separate taxpayer — not when it is used as a paper shield.

⚠️ Disclaimer

This content is for general information and educational purposes only and does not constitute tax or legal advice. Laws and interpretations may change. Please consult a professional advisor before taking action.

Article related to –

HUF taxation in India

Hindu Undivided Family tax rules

HUF income tax planning

Clubbing of income HUF

HUF vs individual tax comparison

HUF tax benefits India

HUF capital gains tax

HUF gift taxation rules

HUF PAN and bank account

HUF income sources explained

HUF partition tax implications

HUF assessment and compliance