Latest Changes, ITC Logic & Audit-Safe Reconciliations (Finin2min)

Objective:

File GSTR-9 with defensible workings, not forced “zero differences”.

1️⃣ What GSTR-9 Really Does (Conceptual Clarity)

| Return | Purpose |

|---|---|

| GSTR-1 | Outward supplies (invoice level) |

| GSTR-3B | Summary return + tax payment |

| GSTR-9 | Annual reconciliation of: |

| • Outward supplies | |

| • ITC availed/reversed/reclaimed | |

| • Spillovers across FYs |

📌 Key insight:

GSTR-9 simultaneously touches 3 FYs (prior, current, next).

Tables 6 & 8 are designed for this cross-year logic — perfect zero is not expected.

2️⃣ “Primary Source” Myth — What CBIC Clarified

CBIC Press Release (03-07-2019):

| Data Set | Role in GSTR-9 |

|---|---|

| GSTR-1 | Outward supply details |

| GSTR-3B | Tax paid & ITC availed |

| Books of Accounts | Accounting truth |

📌 Conclusion :

There is no single primary source.

Different tables rely on different sources → reconciliation is the goal.

3️⃣ Outward Supplies — Missed Reporting Scenarios (Chart)

A. Missed FY 2023-24 supply, reported in April 2024

| Question | Treatment |

|---|---|

| Report in GSTR-9 of FY 2024-25? | ❌ No |

| Correct table | Table 10 of FY 2023-24 |

| Table 4 of FY 2024-25 | ❌ Not to be used |

| Table 9 mismatch | Acceptable (editable tax payable) |

📌 Design logic:

Table 9 tax paid ≠ Table 5 liability is expected here.

B. Missed FY 2024-25 supply, reported in April 2025

| Scenario | Table |

|---|---|

| Reported via GSTR-1/3B by Nov 30 | Table 10 (FY 2024-25) |

| Detected after deadline | Table 4 + DRC-03 |

⚠️ Rule:

You can add liability via GSTR-9.

You cannot reduce liability / claim ITC via GSTR-9.

4️⃣ ITC — Reversal & Reclaim Framework (Validated)

ITC Classification

| Type | Legal Reference | Reclaimable |

|---|---|---|

| Permanent | Sec 17(5), Rules 38/42/43 | ❌ No |

| Temporary (Statutory) | Rule 37, Rule 37A | ✔ Yes |

| Temporary (Circular) | Circular 170/02/2022 | ✔ Yes |

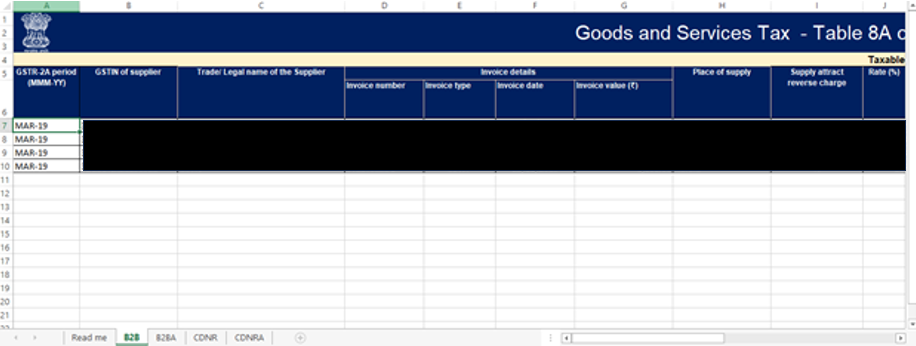

5️⃣ Table-wise ITC Map (High-Value Section)

Table 6 — ITC Claimed

| Table | What to Report | What NOT to Report |

|---|---|---|

| 6A | Total ITC as per GSTR-3B | — |

| 6A1 | Prev FY ITC claimed in current FY (excluding Rule 37/37A) | Rule 37/37A reclaims |

| 6B | Current FY ITC (non-RCM) | Reclaimed ITC |

| 6H | ITC reclaimed under Rule 37 / 37A / Circular 170 | Fresh claims |

(Illustrative visuals to users to Table 6 structure)

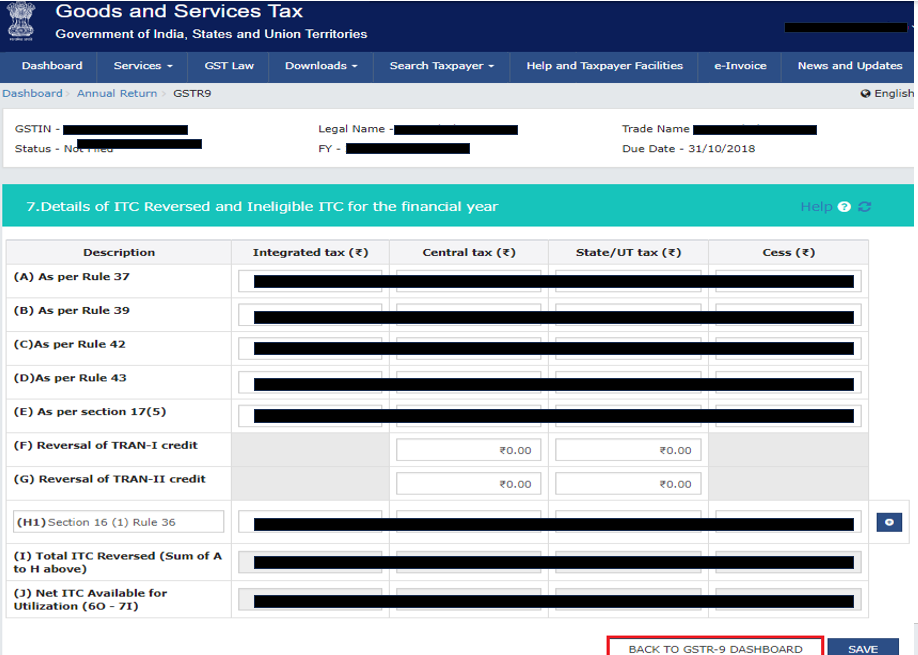

Table 7 — ITC Reversals

| Sub-Table | Reversal Type |

|---|---|

| 7A | Rule 37 |

| 7A1 | Rule 37A |

| 7H | Other reversals (incl. Circular 170) |

📌 FAQ validated:

Prev-year ITC reversed in current FY does NOT come to Table 7 of current FY.

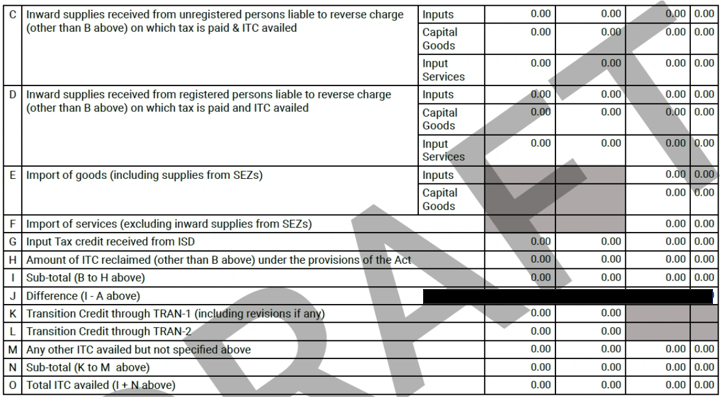

6️⃣ Table 8 — The Most Misunderstood Block

8A vs 8B vs 8C vs 8D (Clean Comparison)

| Table | Meaning |

|---|---|

| 8A | ITC as per GSTR-2B |

| 8B | ITC actually claimed (Table 6B) |

| 8C | Missed ITC of current FY claimed next FY |

| 8D | Difference = 8A – (8B + 8C) |

📌 Expected behaviour:

Table 8D should be positive or zero.

Negative → investigation needed (not automatic fault).

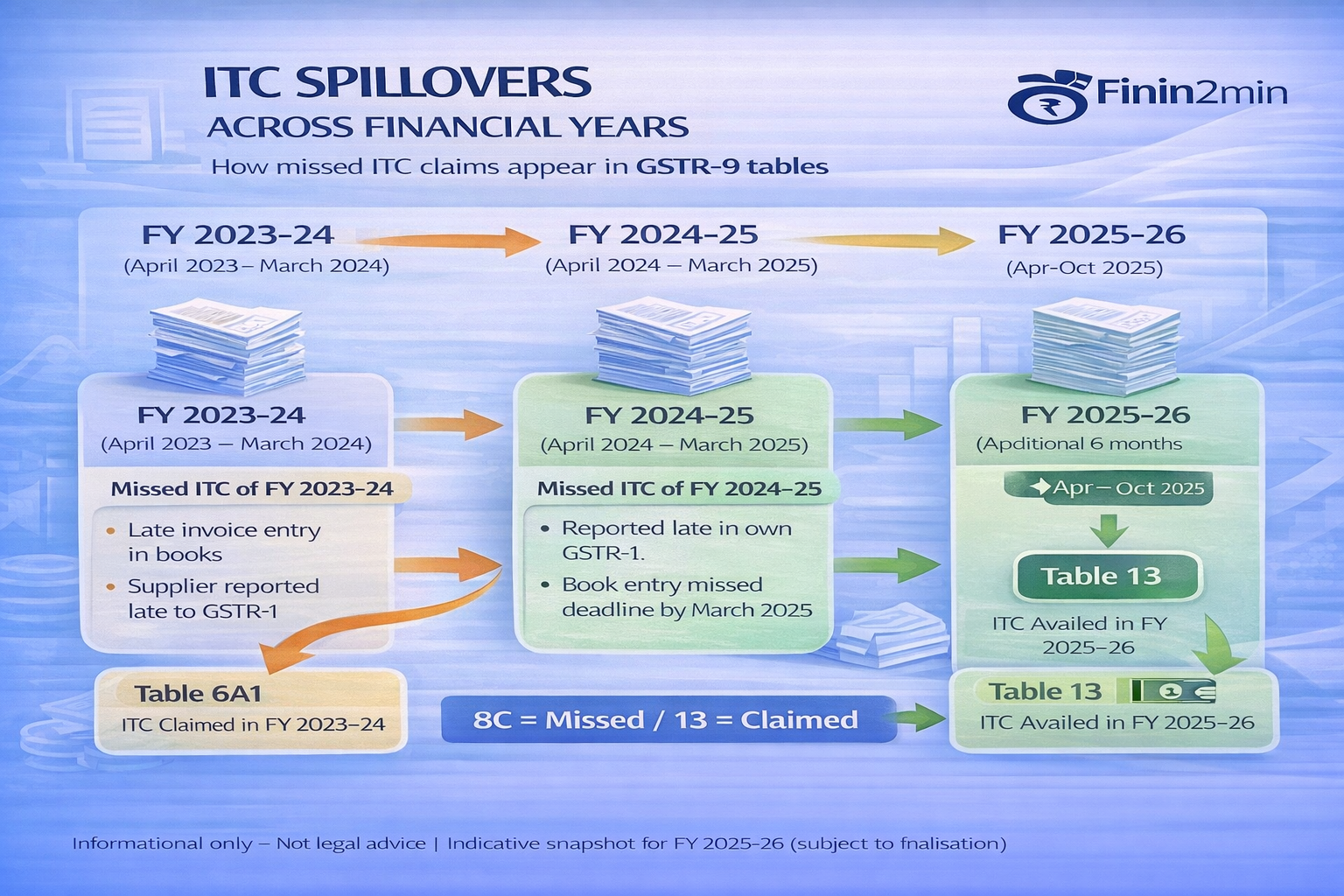

7️⃣ Table 13 — ITC Claimed in Next FY (Key Distinction)

| Aspect | Table 8C | Table 13 |

|---|---|---|

| Nature | Missed in year | Claimed later |

| Basis | GSTR-2B mismatch | Books + eligibility |

| Rule 37/37A | ❌ | ❌ |

| Relation | Current FY | Prev FY spillover |

In one line:

8C = Missed in year

13 = Claimed in next year

8️⃣ FAQs (CBIC 04-12-2025) — Validated Positions

| FAQ Issue | CBIC Clarification |

|---|---|

| 6A1 ITC but no reversal in Table 7 | ✔ Correct |

| Table 7J mismatch with 3B | ✔ Acceptable |

| Table 12B redundancy in 9C | ✔ Explain via Table 13 |

| Negative 8D | ✔ Explanation opportunity |

9️⃣ Audit-Safe Checklist (Finin2min)

✔ Table-wise reconciliation sheets

✔ Prior-year spillover mapping

✔ Rule 37/37A tracking register

✔ DRC-03 challans linked

✔ Explanation notes for non-zero tables

🔟 Finin2min Bottom Line

GSTR-9 is not about zero differences.

It is about logical differences + documented explanations.

A well-reconciled GSTR-9 reduces litigation risk, even when numbers don’t match perfectly.

⚠️ Disclaimer

This guide is for educational purposes only, based on prevailing GST law, CBIC press releases, and FAQs as on date. It does not constitute professional advice. Users should evaluate facts case-by-case and consult advisors before filing.

Article associated with –

ITC spillover under GST

GSTR-9 ITC reconciliation

ITC claimed in next financial year

Table 6A1 GSTR-9 explained

Table 8C vs Table 13 GSTR-9

GSTR-2B vs GSTR-3B ITC mismatch

GST annual return ITC issues

ITC reversal and reclaim GST

GST ITC spillover chart

GSTR-9 ITC tables explained

GST audit reconciliation ITC

Input tax credit spillover India