🗓️ Period: 26 Jan’26 → 1 Feb’26

(Markets • Macro • Commodities • Policy • Global • Strategy • Finin2min)

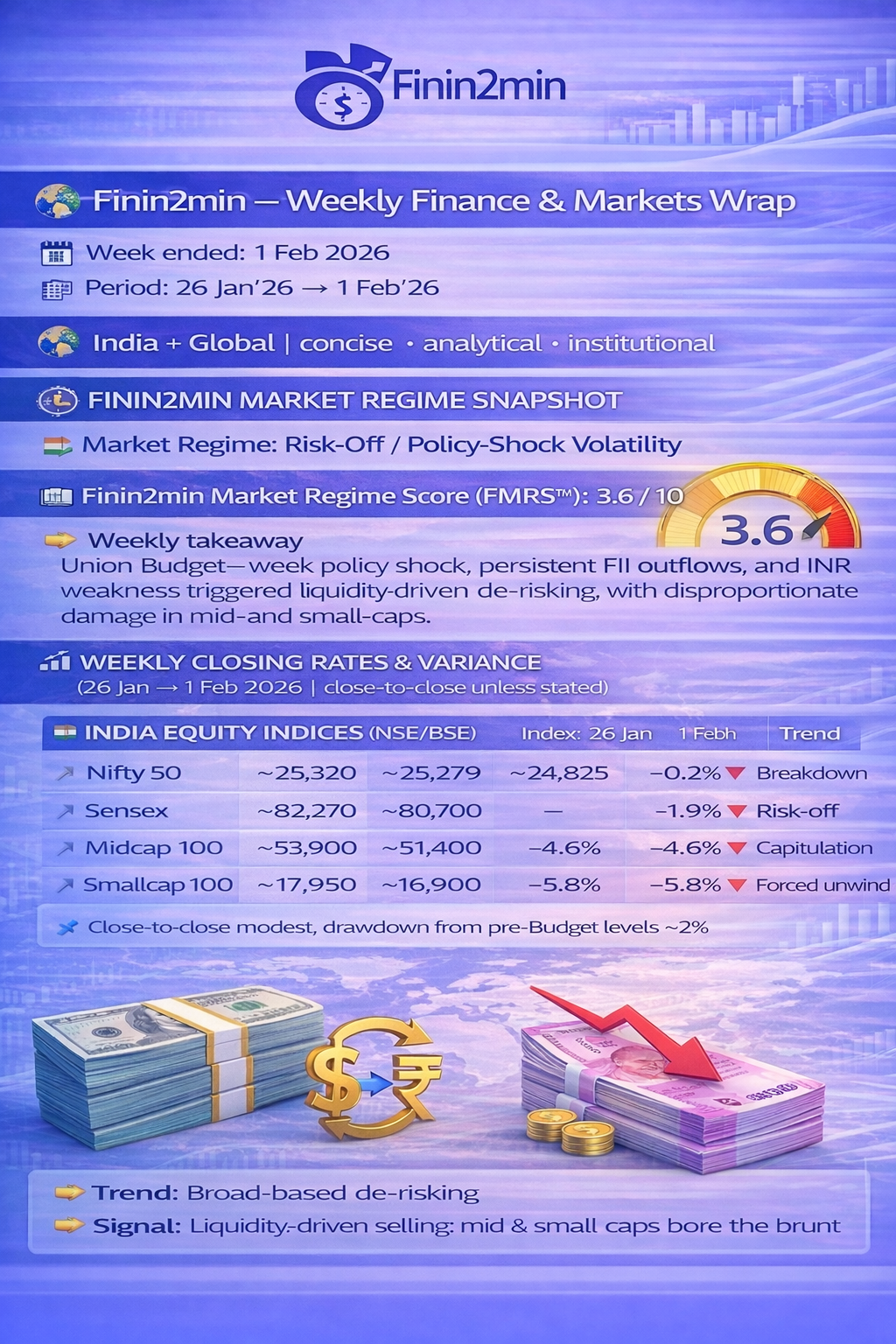

🧭 FININ2MIN MARKET REGIME SNAPSHOT

Market Regime: Risk-Off / Policy-Shock Volatility

Finin2min Market Regime Score (FMRS™): 3.6 / 10

👉 Weekly takeaway

Union Budget–week policy shock, persistent FII outflows, and INR weakness triggered liquidity-driven de-risking, with disproportionate damage in mid- and small-caps.

📊 FININ2MIN QUANT SCORECARD (FQSM™)

- Risk Sentiment Index: 3.5 / 10 ↓

→ Volatility expansion, weak breadth, bearish positioning - Liquidity Score: 4.3 / 10 ↓

→ Firm DXY, higher yields, fiscal supply overhang - Trend Strength

- India: 3.0 / 10 ↓ → Breakdown

- Global: 5.4 / 10 → → Range / selective strength

- Macro Stress Indicator: 7.1 / 10 ↑

→ FX stress + policy uncertainty + volatility spike

📊 WEEKLY CLOSING RATES & VARIANCE

(26 Jan → 1 Feb 2026 | close-to-close unless stated)

🇮🇳 INDIA EQUITY INDICES (NSE/BSE)

| Index | 26 Jan | 1 Feb Close | Weekly Low | WoW % | Trend | Signal |

|---|---|---|---|---|---|---|

| Nifty 50 | ~25,320 | ~25,279 | ~24,825 | -0.2%* | 🔽 | Breakdown |

| Sensex | ~82,270 | ~80,700 | — | -1.9% | 🔽 | Risk-off |

| Midcap 100 | ~53,900 | ~51,400 | — | -4.6% | 🔽🔽 | Capitulation |

| Smallcap 100 | ~17,950 | ~16,900 | — | -5.8% | 🔽🔽🔽 | Forced unwind |

*Close-to-close modest; drawdown from pre-Budget levels ~-2%.

👉 Trend: Broad-based de-risking

👉 Signal: Liquidity-driven selling; mid & small caps bore the brunt

🌍 GLOBAL EQUITIES (WEEKLY % MOVE)

| Index | WoW % | Trend | Signal |

|---|---|---|---|

| S&P 500 | ~-0.3% | ➖ | Range |

| Nasdaq | ~-0.5% | 🔽 | Momentum cooling |

| Dow Jones | ~-0.2% | ➖ | Defensive bias |

👉 Global markets more resilient than India

👉 India underperformance was policy- and FX-driven, not a global risk collapse

🪙 COMMODITIES — USD & INR (MCX/COMEX ranges)

🟡 GOLD

| 26 Jan | 1 Feb (close range) | WoW % | Trend | Signal | |

|---|---|---|---|---|---|

| Gold (USD/oz) | ~5,020 | ~4,880–4,900 | -2.5% to -3% | 🔽 | Profit-booking |

| Gold (INR / 10g) | ~₹1.69–1.70L | ~₹1.45–1.50L | -12% to -15% | 🔽🔽 | Volatility flush |

Interpretation: INR-denominated fall driven by USD correction + extreme positioning unwind.

Hedge value intact, but momentum broken.

⚪ SILVER

| 26 Jan | 1 Feb (close range) | WoW % | Trend | Signal | |

|---|---|---|---|---|---|

| Silver (USD/oz) | ~107 | ~85 | -20% | 🔽🔽🔽 | Forced liquidation |

| Silver (INR / kg) | ~₹3.94–4.00L | ~₹2.68–3.50L | -12% to -30% | 🔽🔽🔽 | Deleveraging stress |

Interpretation: Classic liquidity washout; silver acted as the stress barometer.

🛢️ CRUDE OIL

| Commodity | Close | WoW | Trend | Signal |

|---|---|---|---|---|

| Brent | ~$70–72 | +1% | ➖ | Capped |

| WTI | ~$65 | Flat | ➖ | Growth caution |

👉 Oil capped = growth concerns dominate geopolitics

💱 FX & YIELDS (RBI / global benchmarks)

| Asset | 26 Jan | 1 Feb (range) | WoW | Trend | Signal |

|---|---|---|---|---|---|

| USD/INR | ~91.7–91.8 | ~92.3–92.4 | ↑ | 🔼 | EM stress |

| DXY | ~104.5 | ~105.2 | ↑ | 🔼 | Risk-off |

| India 10Y | ~7.15% | ~7.25% | ↑ | 🔼 | Fiscal supply |

| US 10Y | ~4.05% | ~4.10% | ➖ | ➖ | Sticky yields |

👉 Macro signal: DXY + yields + INR = triple headwind for equities

📉 FLOWS, VOLATILITY & ROTATION

- FPIs: Persistent net sellers (verified flow data)

- DIIs: Partial stabilisers, not trend-changing

- PCR: < 1 → bearish positioning

- India VIX: ~+14% WoW → volatility regime shift

Sectoral rotation

- 🔴 Mid/small caps, rate-sensitives, derivatives-linked names (post STT hike)

- 🟢 FMCG, select private banks, quality defensives

🧠 MARKET SUMMARY

🇮🇳 India Equities

Domestic markets ended the week decisively weaker as sustained foreign selling and currency pressure weighed on sentiment. Benchmarks fell, while mid- and small-caps underperformed sharply, reflecting broad de-risking rather than stock-specific issues. India also logged its weakest monthly equity performance in nearly a year.

🌍 Global Equities

Global markets were volatile but relatively resilient. U.S. and European indices showed mixed patterns amid geopolitical and policy uncertainty. Global equity funds still saw inflows for a third straight week, indicating regional differentiation, not uniform risk exit.

🧠 Macro & Policy

India’s macro backdrop remains structurally resilient (official growth guidance ~6.8–7.2%), but near-term risks from exports, tariffs, capital flows, and FX volatility persist.

The Union Budget dominated sentiment: markets focused on fiscal supply and taxation (STT on F&O) rather than long-term growth intent.

🧠 POLICY & MACRO — WEEKLY DRIVERS

- Union Budget 2026

- Record capex push

- Elevated gross borrowing

- STT hike on F&O

- Market impact: Long-term growth supportive, short-term market negative

- RBI: Liquidity supportive, but FX pressure constrains easing flexibility

🔮 FININ2MIN OUTLOOK

- Base (60%) → Volatile, range-bound with downside bias

- Risk (25%) → Deeper correction if INR/FII worsen

- Bull (15%) → Tactical bounce on global relief rally

🧠 FININ2MIN STRATEGY SIGNAL

➡️ Selectivity > Beta

➡️ Defensives > Cyclicals

➡️ Liquidity > Narratives

➡️ Gold = hedge, not momentum trade

🧭 FININ2MIN BOTTOM LINE

This was not a valuation correction — it was a liquidity and policy repricing week.

Markets are trading flows, FX, and volatility far more than fundamentals.

Market data and developments are based on live updates, news coverage, and financial sources as of the end of today’s session. Finin2min content is for market insight and discussion only. Not investment advice.