(Markets • Macro • Commodities • Policy • Global • Strategy • Finin2min)

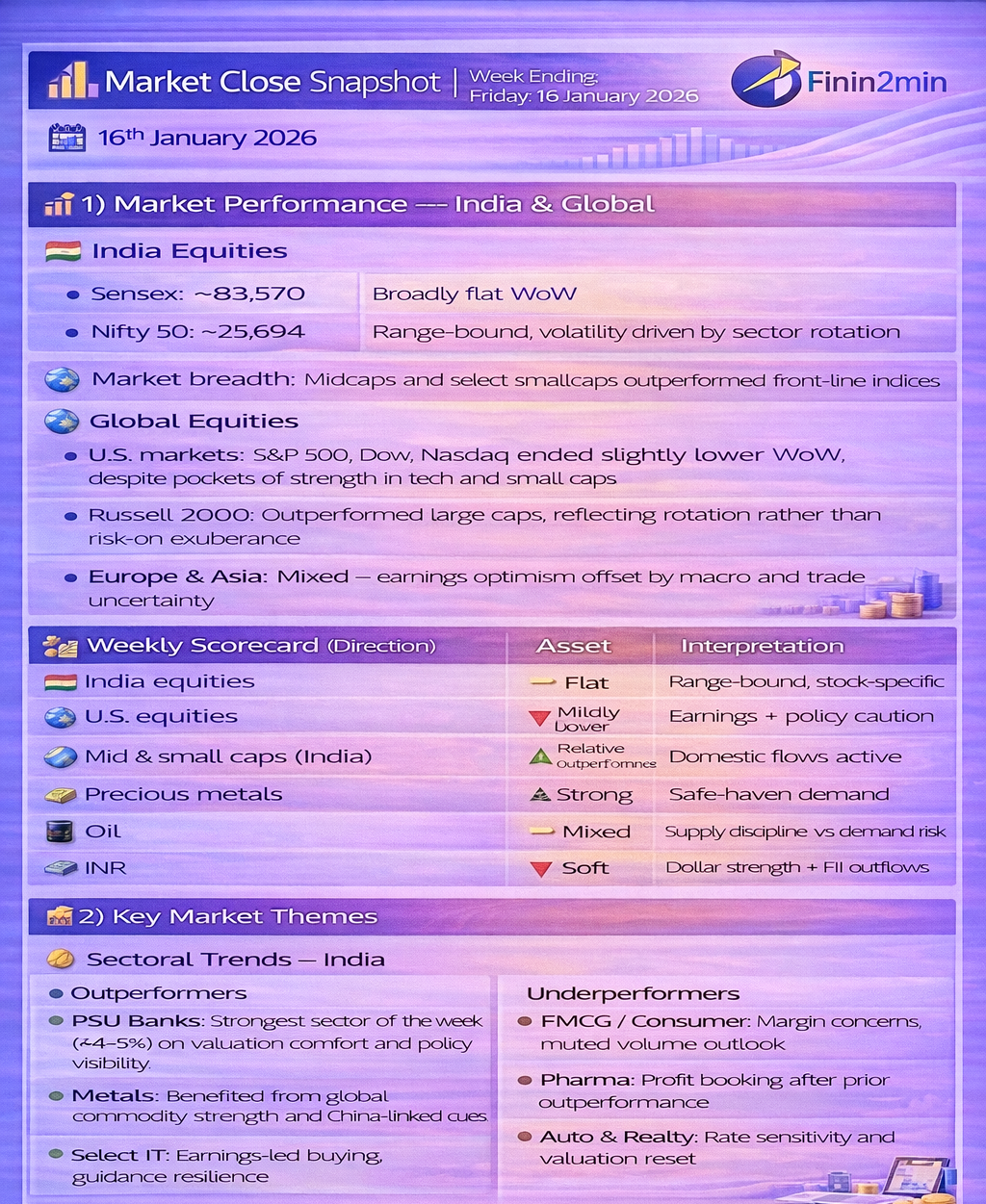

📈 1️⃣ Market Performance — India & Global

🇮🇳 India Equities

- Sensex: ~83,570 — Broadly flat WoW

- Nifty 50: ~25,694 — Range-bound, volatility driven by sector rotation

- Market breadth: Midcaps and select smallcaps outperformed front-line indices

Weekly character:

👉 A selective market — gains concentrated in PSU banks, metals, and a few IT names, while defensives and consumption lagged.

🌍 Global Equities

- U.S. markets: S&P 500, Dow, Nasdaq ended slightly lower WoW, despite pockets of strength in tech and small caps

- Russell 2000: Outperformed large caps, reflecting rotation rather than risk-on exuberance

- Europe & Asia: Mixed — earnings optimism offset by macro and trade uncertainty

📊 Weekly Scorecard (Direction)

| Asset Class | Trend | Interpretation |

|---|---|---|

| India equities | ➖ Flat | Range-bound, stock-specific |

| U.S. equities | 🔽 Mildly lower | Earnings + policy caution |

| Mid & small caps (India) | 🔼 Relative outperformance | Domestic flows active |

| Precious metals | 🔼 Strong | Safe-haven demand |

| Oil | ➖ Mixed | Supply discipline vs demand risk |

| INR | 🔽 Soft | Dollar strength + FII outflows |

🧠 2️⃣ Key Market Themes

🔹 Sectoral Trends — India

Outperformers

- PSU Banks: Strongest sector of the week (~+4–5%) on valuation comfort and policy visibility

- Metals: Benefited from global commodity strength and China-linked cues

- Select IT: Earnings-led buying, guidance resilience

Underperformers

- FMCG / Consumer: Margin concerns, muted volume outlook

- Pharma: Profit booking after prior outperformance

- Auto & Realty: Rate sensitivity and valuation reset

🏛 3️⃣ Policy, Macro & Flows

💸 Flows

- FIIs: Continued net sellers in January (₹20,000+ crore range), remaining a near-term overhang

- DIIs: Provided downside cushion, especially in banks and large caps

🏦 RBI & Bonds (Cautious Framing)

- RBI liquidity conditions remain supportive, helping cap sharp yield spikes

- Global bond index inclusion: Markets continue to speculate on timing and structure; no confirmed Bloomberg index deferral decision was announced during the week

👉 Hence, bond-market expectations remain conditional, not event-driven this week

🪙 4️⃣ Commodities & FX

🪙 Precious Metals — Global (USD/oz)

| Asset | Weekly Range (USD/oz) | Trend | Driver |

|---|---|---|---|

| Gold (Spot) | ~$4,550 – $4,650/oz | 🔼 | Safe-haven flows, policy & trade risk |

| Silver (Spot) | ~$88 – $92/oz | 🔼 | Gold beta + industrial demand |

Interpretation

- Gold remains elevated after a historic 2025 rally, supported by:

- Heightened global trade and policy uncertainty

- Expectations of gradual Fed easing later in 2026

- Silver continues to outperform gold on a relative basis, reflecting both hedge demand and energy-transition narratives

🛢 Oil & Energy

- Brent crude: ~$63–65/bbl range

- Supported by OPEC+ discipline, but upside capped by:

- Demand concerns

- Medium-term surplus expectations

💱 FX

- USD/INR: Mildly weaker bias for INR

- Drivers: Dollar firmness, FII outflows, global risk aversion

🌍 5️⃣ Global Context & Geopolitics

- Markets increasingly pricing heightened U.S. trade / tariff risk in Trump’s second term, reflected in:

- Volatility across EM assets

- Renewed interest in safe-haven assets

- No single trade action dominated this week, but rhetoric-driven uncertainty has become a persistent macro variable

- Global growth expectations remain intact, but risk premiums have widened

📌 6️⃣ Finin2min Bottom Line

This was a range-bound but information-rich week:

- India: Flat indices masked sharp sector rotation — PSU banks, metals, and selective IT outperformed

- Flows: Persistent FII selling continues to cap upside, while domestic flows prevent breakdowns

- Commodities: Gold (~$4,550–4,650/oz) and silver (~$88–92/oz) reinforced their role as macro hedges

- Macro & policy: Markets are navigating policy risk, trade rhetoric, and earnings dispersion, not liquidity stress

🎯 Strategy takeaway

👉 Selectivity > beta.

👉 Policy, trade, and flows now matter more than headline growth.

👉 Quality balance sheets and pricing power remain the safest alpha.

Market data and developments are based on live updates, news coverage, and financial sources as of the end of today’s session. Finin2min content is for market insight and discussion only. Not investment advice.