(Markets • Macro • Commodities • Policy • Global • Strategy • Finin2min)

📊 WEEKLY MARKET PERFORMANCE — INDIA

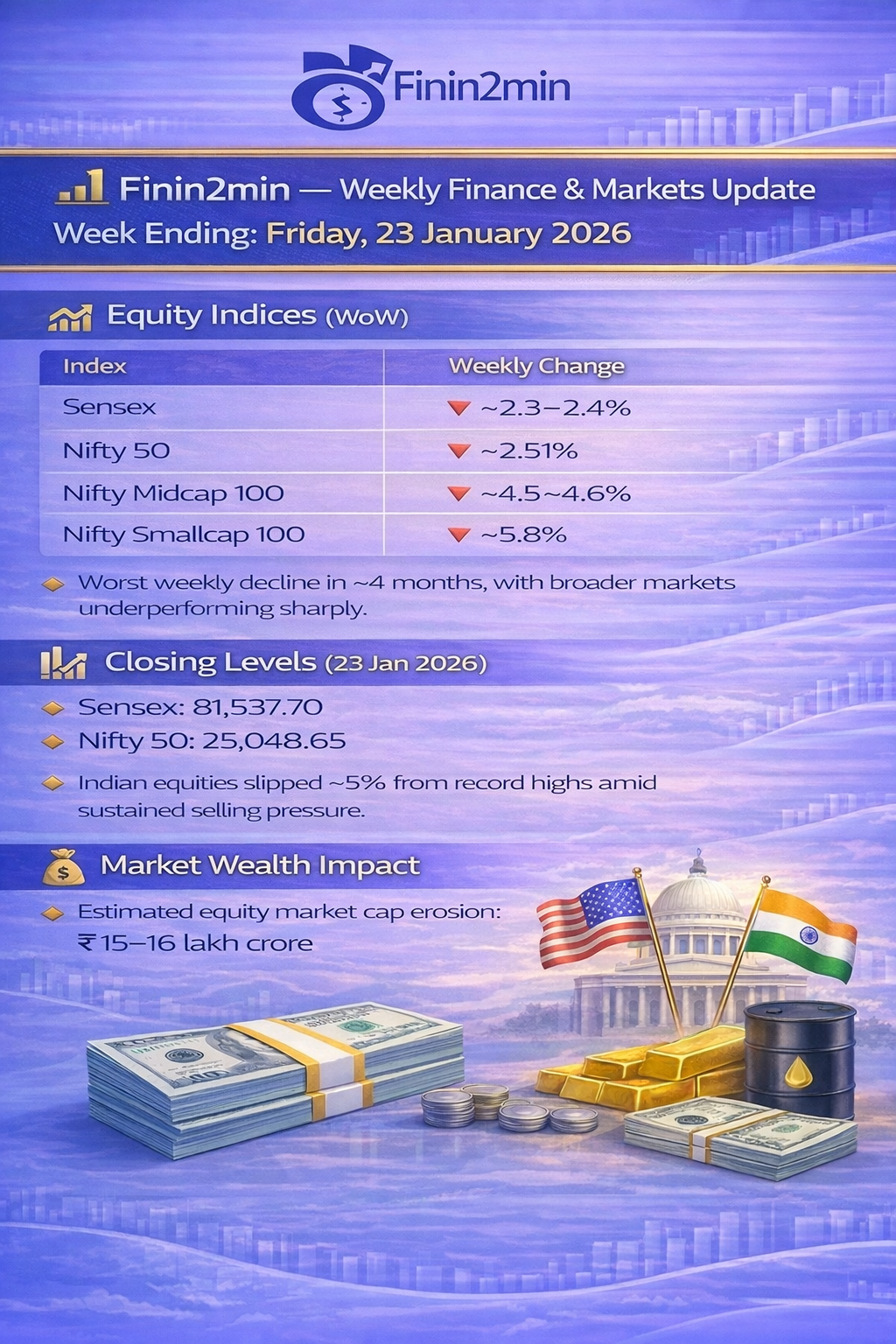

🇮🇳 Equity Indices (WoW)

| Index | Weekly Change |

|---|---|

| Sensex | ▼ ~2.3–2.4% |

| Nifty 50 | ▼ ~2.51% |

| Nifty Midcap 100 | ▼ ~4.5–4.6% |

| Nifty Smallcap 100 | ▼ ~5.8% |

👉 Worst weekly decline in ~4 months, with broader markets underperforming sharply.

📉 Closing Levels (23 Jan 2026)

- Sensex: 81,537.70

- Nifty 50: 25,048.65

👉 Indian equities slipped ~5% from record highs amid sustained selling pressure.

💸 Market Wealth Impact

- Estimated equity market cap erosion: ₹15–16 lakh crore

💱 FX & FLOWS — KEY MACRO SIGNAL

INR

- INR closed the week around ₹91.95–91.96/USD, marking a record low zone.

- Weekly depreciation: ~110 paise.

👉 INR weakness materially amplified equity risk sentiment and FPI outflows.

Flows

- Persistent FPI selling across equities.

- DIIs provided partial offset.

- Global flows tilted toward bonds and safe-haven assets.

🌍 GLOBAL MARKETS — WEEKLY TONE

Equities

- 🇺🇸 US: Mixed but relatively resilient amid earnings and Fed expectations.

- 🌏 Asia: Stable; Japan supported by policy continuity and weaker yen.

- 🇪🇺 Europe: Cautious amid trade and policy uncertainty.

👉 Global markets oscillated between relief rallies and macro risk repricing.

📉 SECTORAL TRENDS — INDIA

🔴 Underperformers

- Midcaps & Smallcaps (deepest correction)

- Cyclicals: Banks, Realty, Infra

- High-beta sectors

🟢 Relative Resilience

- Defensives: FMCG, Pharma

- Select IT & export-oriented stocks

👉 Rotation pattern: Growth → Safety

🏢 KEY CORPORATE & MARKET DEVELOPMENTS

🔥 Adani Group Shock

- Adani group stocks lost ~$12.5 bn market cap after the US SEC sought court approval to serve summons in a civil fraud case.

- Impact:

- Dragged benchmark indices

- Revived governance risk premium

- Intensified FPI selling

👉 Corporate risk re-entered India’s macro narrative.

🪙 COMMODITIES — WEEKLY SIGNALS

Precious Metals

| Asset | Weekly Close / Range | Signal |

|---|---|---|

| Gold (Global) | ~$4,983/oz | Record highs |

| Silver (Global) | ~$103/oz | Strong breakout |

| Gold (India, 24K) | ₹1.56–1.58 lakh/10g | Elevated |

| Silver (India) | ₹3.2–3.3 lakh/kg | Surge |

👉 Interpretation:

Gold + Silver breakout = elevated macro & geopolitical risk hedging.

Crude Oil

- Brent crude: low-to-mid $60/bbl

- OPEC+ confirmed no production increases for Feb–Mar 2026.

👉 Macro signal:

Gold up + oil capped = uncertainty regime, not inflation shock.

🌐 GLOBAL MACRO & POLICY THEMES

1) Trade & Geopolitics

- Tariff risks and geopolitical tensions weighed on risk assets.

- EM risk premium widened.

2) Monetary Policy Divergence

- Fed: higher-for-longer vs gradual easing expectations.

- RBI: easing cycle constrained by FX volatility.

3) Growth vs Policy Narrative

- US growth remains relatively resilient.

- India fundamentals strong, but flows dominated price action.

👉 Global regime:

Fragmented growth + policy uncertainty + asset-class divergence.

🧭 RBI & POLICY —

🇮🇳 RBI — Monetary & Liquidity Context

- Repo rate: 5.25% (cut by 25 bps in Dec 2025)

- 2025 easing cycle: ~125 bps cumulative cuts

- CRR reduced in phases (4% → 3%)

- Liquidity supported via OMOs and FX operations.

Policy stance

➡️ Neutral, constrained by FX volatility and inflation risks.

Market impact

- Bonds: supported by liquidity

- Equities: rate-positive but offset by INR weakness

- INR: fragile despite intervention

🛢 OPEC+ — Supply Discipline

- Production increases paused for Feb–Mar 2026

- Demand outlook weak; geopolitics supportive

👉 Result: Oil range-bound despite tensions.

🇮🇳 SEBI — Structural Reform Signal

- Proposed easing of FPI settlement and cash market norms (consultation stage)

- Aim: deepen capital markets and attract global capital

👉 Long-term bullish structural signal amid short-term volatility.

🧠 FININ2MIN — WEEKLY KEY THEMES

1️⃣ India underperformed global markets

Domestic shocks amplified global volatility.

2️⃣ Broad-market correction

Midcaps & smallcaps suffered disproportionate damage.

3️⃣ Corporate risk resurfaced

Adani episode revived governance risk premium.

4️⃣ Macro hedges strengthened

Gold & silver rally confirmed risk-off positioning.

🔮 FININ2MIN OUTLOOK — NEXT WEEK

Key Catalysts

- Union Budget expectations (India)

- FPI flows & INR trajectory

- US Fed signals & earnings

- Geopolitical headlines

- Nifty technical zone: ~25,000

Market Bias

- Base case: Volatile, range-bound

- Risk case: Deeper correction if flows worsen

- Bull case: Tactical bounce on global relief rally

🧭 FININ2MIN BOTTOM LINE

India: Worst week in months driven by flows, currency weakness, and corporate risk.

Global: Relief rallies exist, but macro uncertainty dominates.

Commodities: Gold and silver breakout confirms elevated risk hedging, while oil remains capped.

👉 Finin2min verdict:

This was not a routine correction — it marked a shift from growth optimism to risk pricing.

Strategy Signal

- ✅ Selectivity > beta

- ✅ Defensives > cyclicals

- ✅ Liquidity > narratives

Market data and developments are based on live updates, news coverage, and financial sources as of the end of today’s session. Finin2min content is for market insight and discussion only. Not investment advice.