🗓️ Period: 16 Feb’26 → 22 Feb’26

(Markets • Macro • Commodities • Policy • Global • Strategy • Finin2min)

🧭 FININ2MIN MARKET REGIME SNAPSHOT

Market Regime: Stability with positioning bias

FMRS™: 6.0 / 10

👉 Weekly takeaway

Markets absorbed uncertainty without correcting.

Stronger domestic growth + softer global yields shifted positioning from hedging → accumulation.

This was a confidence-building week before a directional move.

📊 FININ2MIN QUANT SCORECARD

Risk Sentiment: 6.2 / 10 ↑

Liquidity: 5.8 / 10 →

Trend Strength — India: 6.0 / 10 ↑

Trend Strength — Global: 6.4 / 10 ↑

Macro Stress: 4.3 / 10 ↓

Interpretation: Early trend formation phase.

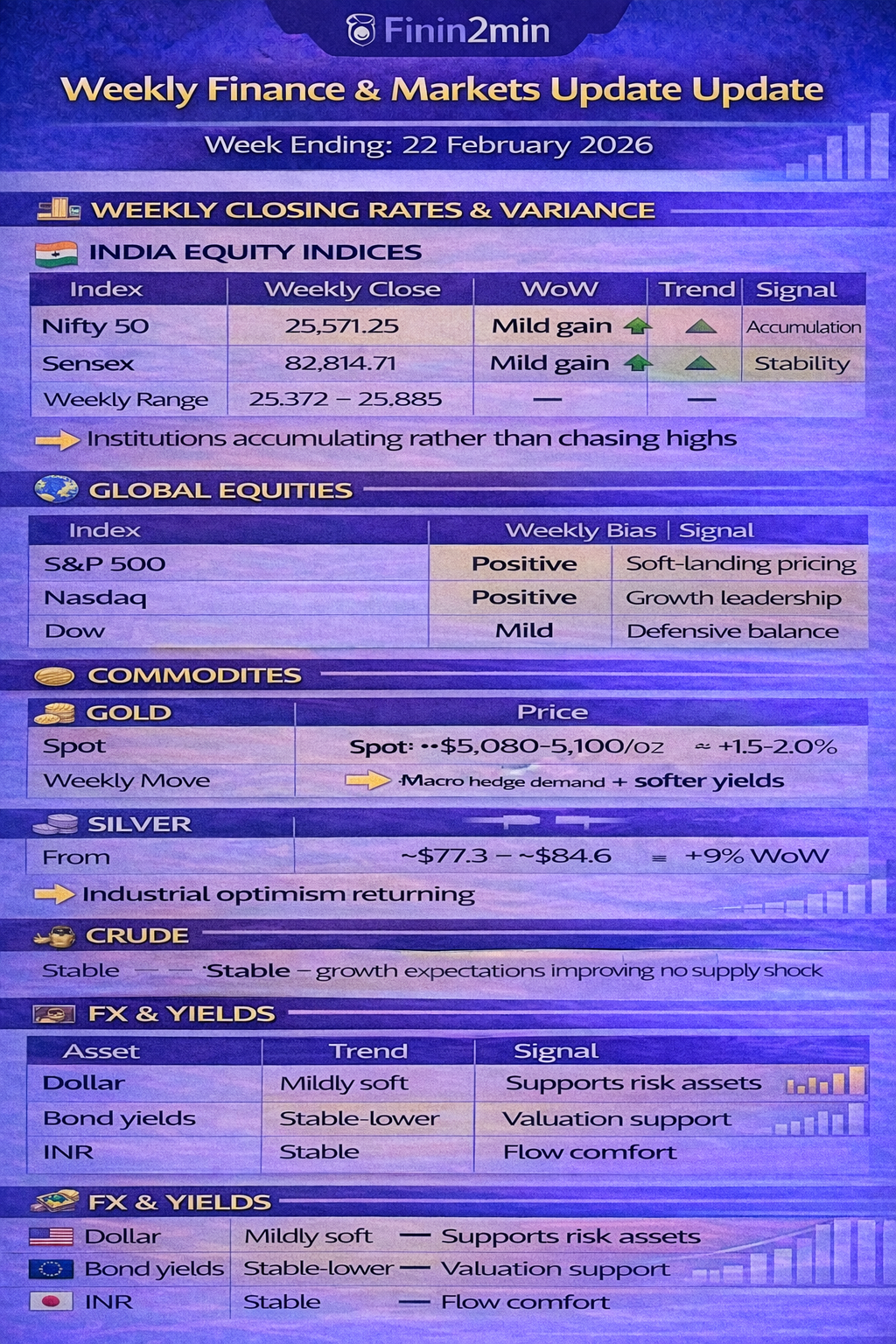

📊 WEEKLY CLOSING RATES & VARIANCE

🇮🇳 INDIA EQUITY INDICES

| Index | Weekly Close | WoW | Trend | Signal |

|---|---|---|---|---|

| Nifty 50 | 25,571.25 | Mild gain | 🔼 | Accumulation |

| Sensex | 82,814.71 | Mild gain | 🔼 | Stability |

| Weekly Range | 25,372 – 25,885 | — | ➖ | Consolidation |

👉 Institutions accumulating rather than chasing highs

🌍 GLOBAL EQUITIES

| Index | Weekly Bias | Signal |

|---|---|---|

| S&P 500 | Positive | Soft-landing pricing |

| Nasdaq | Positive | Growth leadership |

| Dow | Mild | Defensive balance |

🪙 COMMODITIES

🟡 GOLD

| Level | Price |

|---|---|

| Spot | ~$5,080–5,100/oz |

| Weekly Move | ≈ +1.5–2.0% |

Macro hedge demand + softer yields

⚪ SILVER

| From | To | Move |

|---|---|---|

| ~$77.3 | ~$84.6 | ≈ +9% WoW |

Industrial optimism returning

🛢️ CRUDE

Stable — growth expectations improving, no supply shock

💱 FX & YIELDS

| Asset | Trend | Signal |

|---|---|---|

| Dollar | Mildly soft | Supports risk assets |

| Bond yields | Stable-lower | Valuation support |

| INR | Stable | Flow comfort |

🧠 MACRO & POLICY — WHAT MOVED MARKETS

🇮🇳 India — Growth & Policy Anchors

RBI minutes confirmed steady stance:

- Repo unchanged (~5.25%)

- FY26 growth ~7.4%

- Inflation gradually toward 4%

- 10Y G-Sec ~6.67% (no bond stress)

Domestic data and flows this week reconfirmed India as the fastest-growing major economy with supportive policy.

High-Frequency Data Strength

- HSBC Composite PMI ~59+ → strong expansion

- Broad-based manufacturing + services growth

🇮🇳 India — Flows Confirm the Story

- FPIs ~₹33,000+ crore early Feb inflow

- Largest since Apr 2025

- Concentrated in financials, capital goods, oil & gas

👉 Confirms accumulation in cyclicals, not speculative rally

🌏 Global Growth & Trade Policy

Trade policy discussions remained an overhang but without escalation.

Global growth outlook modestly improved → recession fears fading.

Earlier-Feb US CPI downside surprise reinforced disinflation narrative and helped anchor yields.

🇺🇸 US Rates & Fed Path

- Economy slowing but healthy

- Rate cuts delayed, not cancelled

- Yields stable → valuation support

This explains:

- Gold above $5,000

- Stable equities

- No risk-off shock

🇪🇺 Europe

Manufacturing stabilising → supportive global backdrop

🇮🇳 Policy — External Borrowing Framework

RBI eased external borrowing norms

Impact:

- Easier corporate funding

- Supports capex cycle

- Reinforces industrial leadership

📉 FLOWS & POSITIONING

- FIIs selective buyers

- DIIs steady support

- Volatility compression

Sector leadership:

🟢 Financials, Industrials, Capex

🟡 IT selective

🔴 Momentum cooling

🔮 FININ2MIN OUTLOOK

Base (55%): Sideways → upward bias

Bull (30%): Liquidity breakout

Risk (15%): Yield spike / trade escalation

🧠 FININ2MIN STRATEGY SIGNAL

➡️ Accumulate on dips

➡️ Financials & industrials leadership

➡️ Avoid crowded trades

➡️ Gold hedge, not chase

🧭 FININ2MIN BOTTOM LINE

The market didn’t rally because it was uncertain.

It didn’t fall because macro was strong.

Positioning phase precedes trend — and we are in that phase now.

Finin2min — market insight only, not investment advice.