Cost of Acquisition, Perquisite Tax & Capital Gains Explained

Law • Tax • Startups • Employees • Wealth Creation

2-minute read | Practical | Liquidity-aware | Compliance-first

1️⃣ WHAT IS AN ESOP (IN LAW & PRACTICE)

Employee Stock Option Plan (ESOP) gives employees the right (not obligation) to buy company shares at a fixed price after a vesting period.

📜 Legal basis

- Companies Act, 2013 – Section 62(1)(b)

- Companies (Share Capital & Debentures) Rules, 2014 – Rule 12

📌 Requires:

- Shareholder special resolution

- Defined vesting, exercise price, valuation

- Non-transferable till exercise

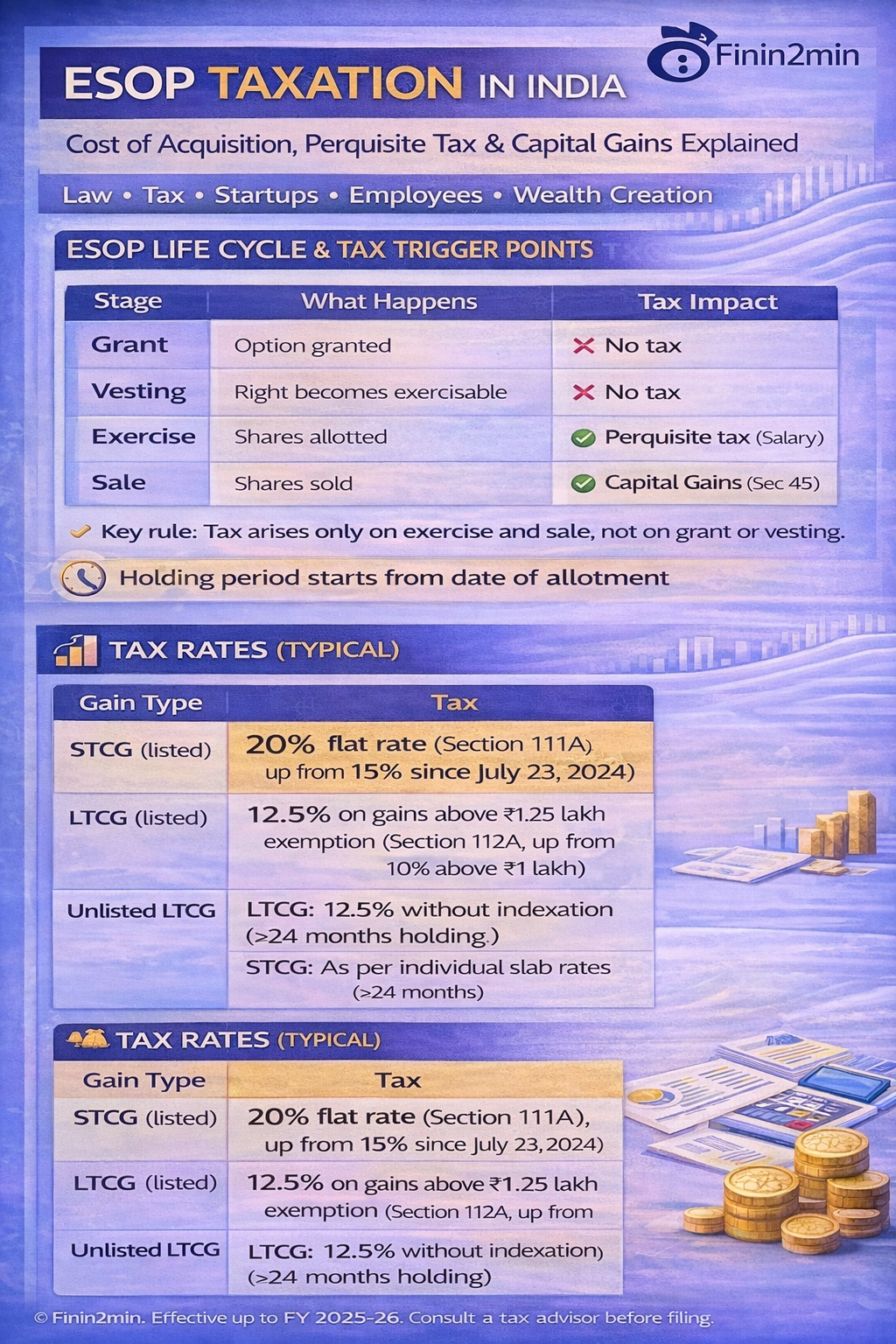

2️⃣ ESOP LIFE CYCLE & TAX TRIGGER POINTS

| Stage | What Happens | Tax Impact |

|---|---|---|

| Grant | Option granted | ❌ No tax |

| Vesting | Right becomes exercisable | ❌ No tax |

| Exercise | Shares allotted | ✅ Perquisite tax (Salary) |

| Sale | Shares sold | ✅ Capital Gains (Sec 45) |

📌 Key rule: Tax arises only on exercise and sale, not on grant or vesting.

3️⃣ TAX AT EXERCISE — PERQUISITE (SALARY INCOME)

📜 Section 17(2)(vi), Income-tax Act

Taxable Perquisite = FMV on exercise date – Exercise price

| Particulars | Amount |

|---|---|

| FMV on exercise | ₹300 |

| Exercise price | ₹50 |

| Perquisite taxable | ₹250 per share |

✔ Taxed under Salary

✔ Employer deducts TDS u/s 192

✔ Applies to listed & unlisted shares

📌 FMV rules

- Listed shares → Market price (Rule 3)

- Unlisted shares → Merchant Banker valuation (Rule 3(8))

4️⃣ STARTUP RELIEF — DEFERRAL OF PERQUISITE TAX

📜 Section 192(1C) — Finance Act, 2020

Applicable only to eligible DPIIT-recognised startups

⏳ Perquisite tax deferred to earliest of:

- Sale of shares

- Exit from company

- 48 months from end of AY of exercise

📌 Not an exemption — only timing relief

📌 TDS liability still exists (timing deferred)

5️⃣ CAPITAL GAINS ON SALE — SECTION 45

Once shares are sold:

📜 Section 45 + Section 49(2AA)

Cost of acquisition = FMV already taxed as perquisite

| Particulars | Amount |

|---|---|

| Sale price | ₹500 |

| Cost (FMV at exercise) | ₹300 |

| Capital Gain | ₹200 |

✔ Prevents double taxation

✔ Statutorily settled under Section 49(2AA)

6️⃣ HOLDING PERIOD & TAX RATES (VALIDATED)

⏱ Holding period starts from date of allotment

| Share Type | LTCG Threshold |

|---|---|

| Listed equity | > 12 months |

| Unlisted shares | > 24 months |

💰 Tax Rates (Typical)

| Gain Type | Tax |

|---|---|

| STCG (listed) | 20% flat rate (Section 111A, up from 15% since July 23, 2024) |

| LTCG (listed) | 12.5% on gains above ₹1.25 lakh exemption (Section 112A, up from 10% above ₹1 lakh) |

| Unlisted LTCG | LTCG: 12.5% without indexation (>24 months holding). STCG: As per individual slab rates (≤24 months) |

7️⃣ SPECIAL CASES — RSU, SAR, PHANTOM STOCKS

| Instrument | Shares issued? | Tax Treatment |

|---|---|---|

| RSU | Yes | Perquisite + Capital Gains |

| SAR (cash-settled) | ❌ No | Salary income |

| Phantom stock | ❌ No | Salary income |

📌 No capital gains if no shares allotted.

8️⃣ KEY JUDICIAL PRINCIPLES (SETTLED LAW)

⚖️ Landmark Cases

- CIT v. Infosys Technologies Ltd. (SC)

→ Tax arises on exercise, not grant - Ramamoorthy Sridharan (ITAT)

→ FMV taxed as perquisite = cost for CG - Conflicting HC views exist only for cash compensation on unexercised ESOPs

📌 Core ESOP taxation framework is largely settled.

9️⃣ FOREIGN ESOPS — ADDITIONAL COMPLIANCE

🧾 FEMA / Income-tax

- FA Schedule mandatory for ROR residents

- LRS applies on exercise price paid abroad

- TCS applicable on remittance (claimable as credit)

🔟 COMMON MISTAKES (AND HOW TO AVOID)

❌ Expecting capital gains without perquisite tax

❌ Ignoring valuation report for unlisted shares

❌ Not planning cash for exercise-stage tax

❌ Missing FA Schedule disclosure

❌ Assuming startup deferral = exemption

✔ Plan exercise timing + liquidity event together

✔ Track FMV reports & TDS certificates

📌 FININ2MIN SUMMARY TABLE

| Event | Tax Head | Section |

|---|---|---|

| Exercise | Salary (Perquisite) | 17(2)(vi) |

| Sale | Capital Gains | 45 |

| Cost rule | FMV = cost | 49(2AA) |

| Startup deferral | Timing relief | 192(1C) |

🎯 FININ2MIN TAKEAWAY

ESOPs are taxed twice — but on two different value layers.

- Exercise → Salary tax on benefit

- Sale → Capital gains on appreciation

📌 The real risk is liquidity mismatch, not tax rate.

📌 Smart planning = timing exercise near exit or liquidity.

⚠️ DISCLAIMER

This article reflects Indian tax and corporate law as applicable up to FY 2025-26. ESOP taxation depends on share type, valuation, residency and employer status. Always validate with company documents and tax advisors.

Article related to –

ESOP taxation in India

ESOP perquisite tax calculation

Capital gains on ESOP shares

Cost of acquisition for ESOP

ESOP tax after exercise and sale

ESOP tax rates FY 2025-26

Listed vs unlisted ESOP capital gains

Startup ESOP tax explained

ESOP liquidity and tax planning