Markets • Macro • Commodities • Policy • Corporates • Global

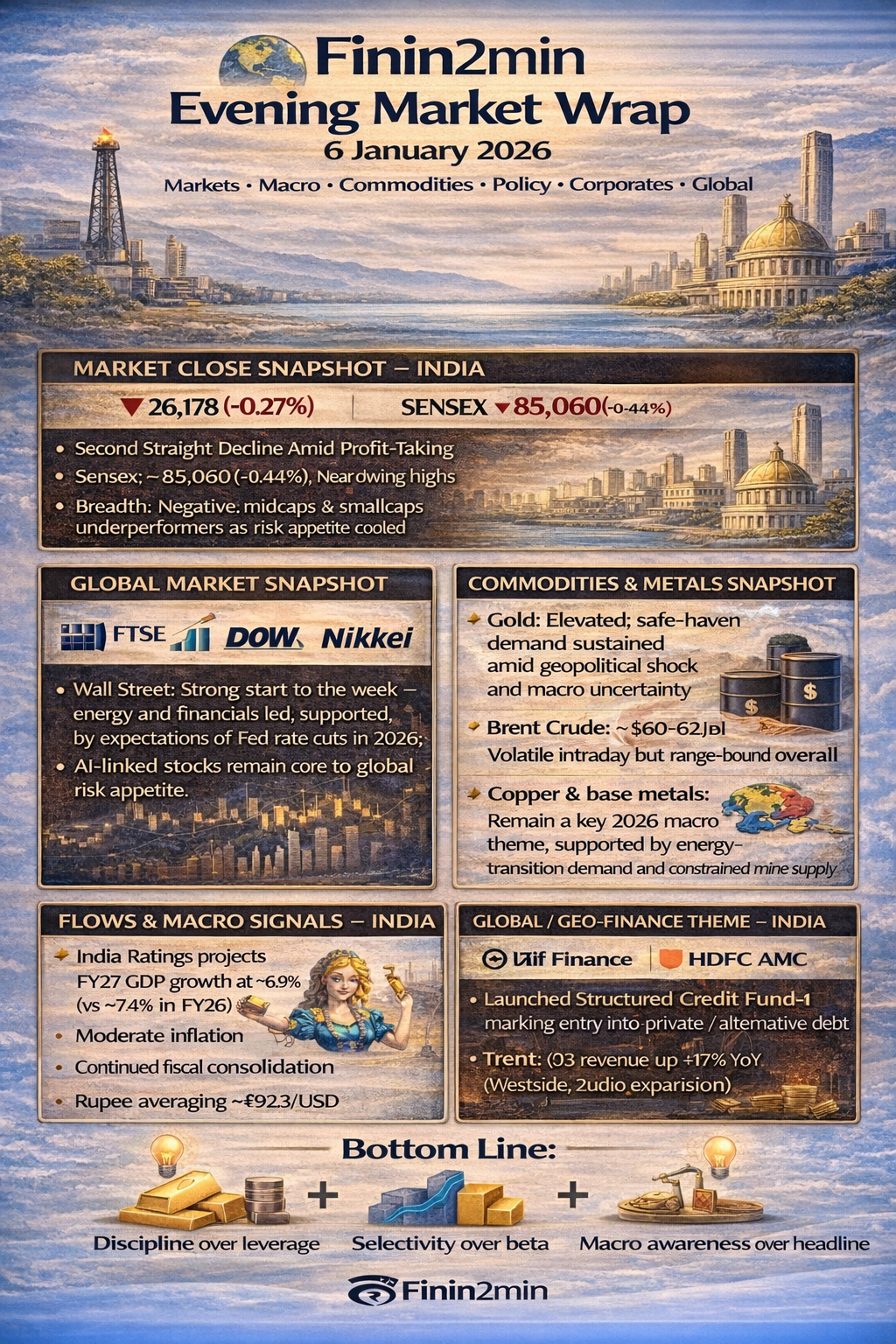

📉 Market Close Snapshot — India

- Nifty 50: ~26,178 (–0.27%) — second consecutive down day as profit-booking emerged near record highs.

- Sensex: ~85,060 (–0.44%), dragged by heavyweight pressure (banks, energy).

- Breadth: Negative; midcaps and smallcaps underperformed as risk appetite cooled.

Sectoral trends

- Outperformance: Select private banks, pharma, defensives

- Underperformance: Oil & Gas, IT, large consumer names

🌍 Global Market Snapshot

- Wall Street: Strong start to the week — energy and financials led, supported by expectations of Fed rate cuts later in 2026; AI-linked stocks remain core to global risk appetite.

- Europe: Equities firm; FTSE and peers near multi-year highs.

- Asia: Mixed, balancing global optimism with geopolitical uncertainty.

- FTSE 100: ~10,122 (+1.18%) — showing strength in UK equities

🪙 Commodities & Metals Snapshot

- Gold: ~$4,427 – $4,495/Oz, Elevated; safe-haven demand sustained amid geopolitical shock and macro uncertainty.

- Silver: ~$75.9-$81.48/Oz, Firm, tracking gold with added industrial tailwinds.

- Brent Crude: ~$60–62/bbl — volatile intraday but range-bound overall.

- Copper & base metals: Remain a key 2026 macro theme, supported by energy-transition demand and constrained mine supply.

💱 Flows & Macro Signals — India

Growth & fiscal outlook

- India Ratings projects FY27 GDP growth at ~6.9% (vs ~7.4% in FY26), describing the phase as “Goldilocks”:

- Moderate inflation

- Continued fiscal consolidation

- Rupee averaging ~₹92.3/USD

- Central fiscal deficit seen near ~4.1% of GDP; debt-to-GDP easing toward ~55–56%.

- Current-account deficit expected to widen modestly to ~1.5% of GDP.

Market implication:

India’s macro stability remains intact, but return expectations normalize, reinforcing the need for selectivity rather than broad-based risk-on trades.

🌐 Global / Geo-Finance Theme — US–Venezuela Shock

- A US special-forces operation captured Venezuelan President Nicolás Maduro on 3 Jan 2026 (Operation “Absolute Resolve”), triggering diplomatic backlash from Russia, China and others.

Oil & finance linkage

- Short term: Heightened oil volatility and geopolitical risk premium.

- Medium term: Possibility of higher Venezuelan oil output, which could:

- Be bearish for crude later in 2026

- Reshape EM debt flows, sanctions regimes, and BRICS-aligned financing dynamics

This explains why gold rallied sharply, while oil failed to sustain a geopolitical spike.

🏢 Corporate & Sector Highlights — India

- L&T Finance

- Strong YoY growth in retail disbursements and loan book

- Q3 profit dipped modestly, keeping NBFC asset-quality and funding costs in focus

- HDFC Asset Management Company

- Launched Structured Credit Fund-I, marking entry into private credit / alternative debt

- Signals growing institutional appetite for non-bank credit amid tightening regulation

- Trent

- Q3 revenue up ~17% YoY (Westside, Zudio expansion)

- Stock corrected ~8–10% as valuations looked stretched post-rally

🧠 Key Themes Emerging

- India: Stable macro, slower but sustainable growth → valuation discipline matters

- Global: Fed-cut narrative intact, but geopolitics now a first-order variable

- Commodities: Precious metals bid; base metals structurally strong; oil capped by supply math

- Equities: Rotation over momentum; earnings and balance-sheet strength back in focus

✅ Bottom Line

Markets ended weaker but orderly in India as profit-taking met strong global cues.

The Venezuela shock reinforced gold’s safe-haven role, but oil remains capped by medium-term surplus risks.

India’s “Goldilocks” macro phase supports stability, not exuberance.

2026 is shaping up as a year of:

- Discipline over leverage

- Selectivity over beta

- Macro awareness over headline trading

— Finin2min