Markets • Macro • Commodities • Policy • Corporates • Global Indices Close (08 Jan 2026)

- Sensex ended sharply lower, down ~780 pts, finishing near 84,181 — its worst session in a month and the fourth consecutive decline.

- Nifty 50 closed below 25,900, extending the recent downtrend with broad selling across sectors.

- Volatility (India VIX) spiked, reflecting rising investor nervousness.

🔥 Sectoral Leaders & Laggards

Laggards

- IT & large‑caps such as Tech Mahindra, TCS underperformed amid risk-off flows.

- Oil & Gas/Metals also lagged, pressured by commodity volatility and weaker risk appetite.

Relatively Resilient

- Financials: Bajaj Finserv outperformed peers modestly despite broader declines.

- Select cyclical names witnessed stock‑specific strength (e.g., Balaji Amines, Panacea Biotec).

🏢 Corporate & Policy Highlights

- Reliance Industries says it may consider buying Venezuelan oil if allowed for non‑US buyers — a key development in energy/raw material flows.

- Trade tensions dominated sentiment as fears over potential U.S. tariff hikes weighed on markets.

📊 Flows & Macro Trends

- Foreign institutional investors (FIIs) continued net selling pressure, exacerbating the index slide.

- FX & bond cues: Higher global bonds and a stronger dollar backdrop supported defensive positioning in fixed income.

🛢 Commodities

- Gold and silver saw mixed action; gold prices eased, while precious metals dynamics reflected broader risk repricing.

- Oil prices stabilized after recent weakness amid global geopolitical repositioning.

🌍 Global Cues

- U.S. Equity Markets: Recent rally momentum shows some resilience and technical buildup, especially in broader indices like Nasdaq (bullish consolidation signs).

- Europe: Shares softened after earnings misses, with retail and commodity pressure broadening caution.

- Macro Risks: Geopolitics (Venezuela/U.S. trade policies) and looming Fed leadership transition remain key market drivers.

🧭 Bottom Line – Finin2min Take

Market Mood: Risk‑off. Indian equities are sliding on trade policy fears, FII outflows, and global caution, extending a short‑term downtrend.

Key Drivers to Watch:

- US trade policy & tariff outcomes (sentiment trigger)

- FII flow patterns (continued selling could deepen corrections)

- Global macro prints (US labor data, inflation, Fed cues)

Tactical Lens: In this environment, defensive and quality sectors may outperform, while broad index exposure faces near‑term pressure. Technical levels around 25,800–25,950 on the Nifty will be key supports to monitor.

This wrap combines live market closes, macro drivers, corporate cues, and global sentiment for a concise daily view.

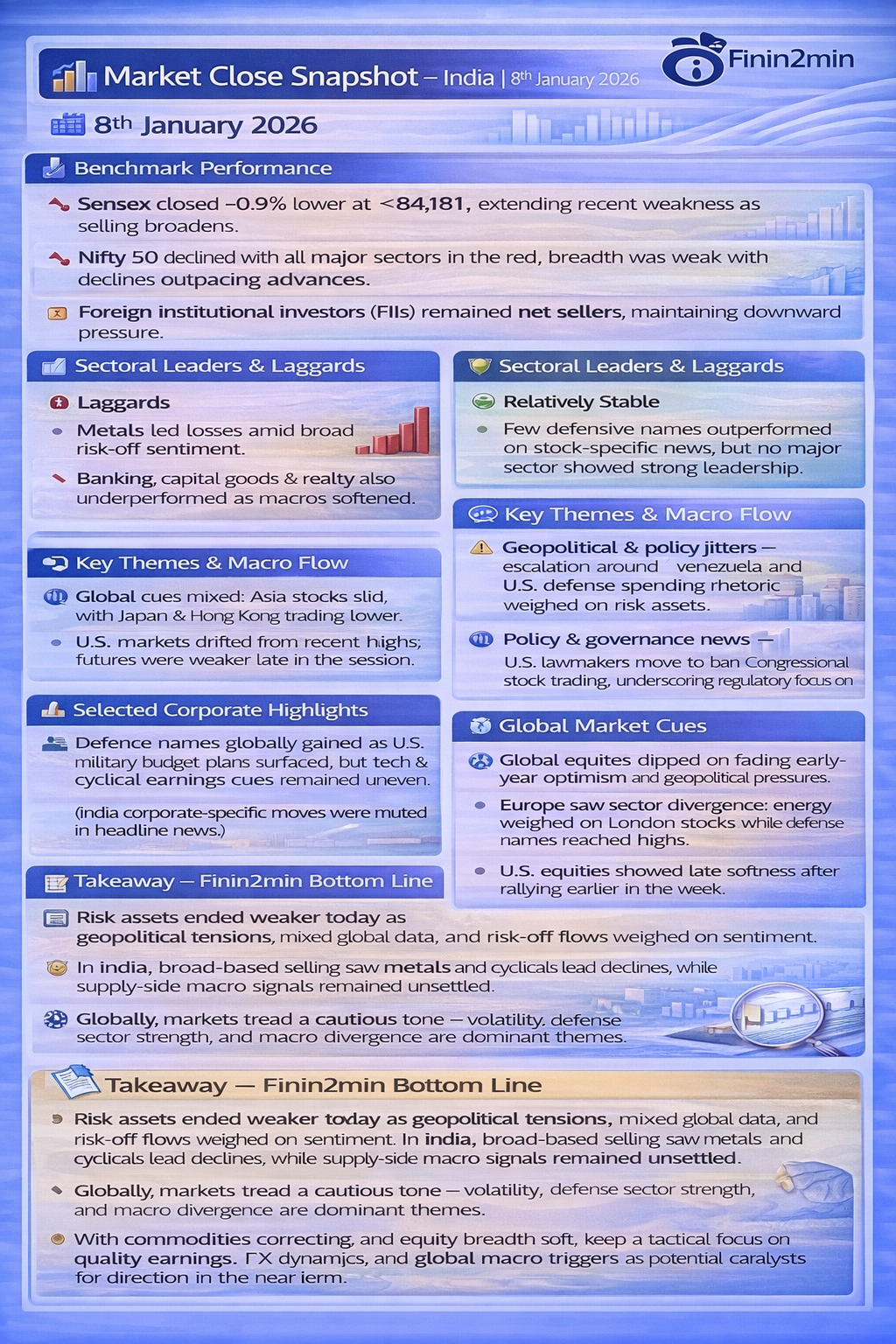

📊 Market Close Snapshot – India

- 📉 Sensex closed ~0.9% lower at ~84,181, extending recent weakness as selling broadens.

- 📉 Nifty 50 declined with all major sectors in the red; breadth was weak with declines outpacing advances.

- Foreign institutional investors (FIIs) remained net sellers, maintaining downward pressure.

📈 Sectoral Leaders & Laggards

Laggards

- Metals led losses amid broad risk‑off sentiment.

- Banking, capital goods & realty also underperformed as macros softened.

Relatively Stable

- Few defensive names outperformed on stock‑specific news, but no major sector showed strong leadership.

🧠 Key Themes & Macro Flow

- Geopolitical & policy jitters — escalation around Venezuela and U.S. defense spending rhetoric weighed on risk assets.

- Global cues mixed: Asia stocks slid, with Japan & Hong Kong trading lower.

- U.S. markets drifted from recent highs; futures were weaker late in the session.

- Policy & governance news — U.S. lawmakers move to ban Congressional stock trading, underscoring regulatory focus on markets.

🏢 Selected Corporate Highlights

- Defence names globally gained as U.S. military budget plans surfaced, but tech & cyclical earnings cues remained uneven.

(India corporate specific moves were muted in headline news.)

🛢 Commodities & Currencies

- Gold softened on index rebalance selling and a firmer dollar backdrop, reducing safe‑haven demand.

- Oil markets steadied after earlier swings tied to geopolitical developments.

- Commodities reflected mixed sentiment — profit‑booking in precious metals amid broader risk repricing.

🌍 Global Market Cues

- Global equities dipped on fading early‑year optimism and geopolitical pressures.

- Europe saw sector divergence: energy weighed on London stocks while defence names reached highs.

- U.S. equities showed late softness after rallying earlier in the week.

🧾 Takeaway — Finin2min Bottom Line

Risk assets ended weaker today as geopolitical tensions, mixed global data, and risk‑off flows weighed on sentiment. In India, broad‑based selling saw metals and cyclicals lead declines, while supply‑side macro signals remained unsettled. Globally, markets tread a cautious tone — volatility, defense sector strength, and macro divergence are dominant themes. With commodities correcting and equity breadth soft, keep a tactical focus on quality earnings, FX dynamics, and global macro triggers as potential catalysts for direction in the near term.

Disclaimer: Finin2min content is for market insight and discussion only. Not investment advice.