Markets • Macro • Commodities • Policy • Corporates • Global Indices Close

Sensex & Nifty:

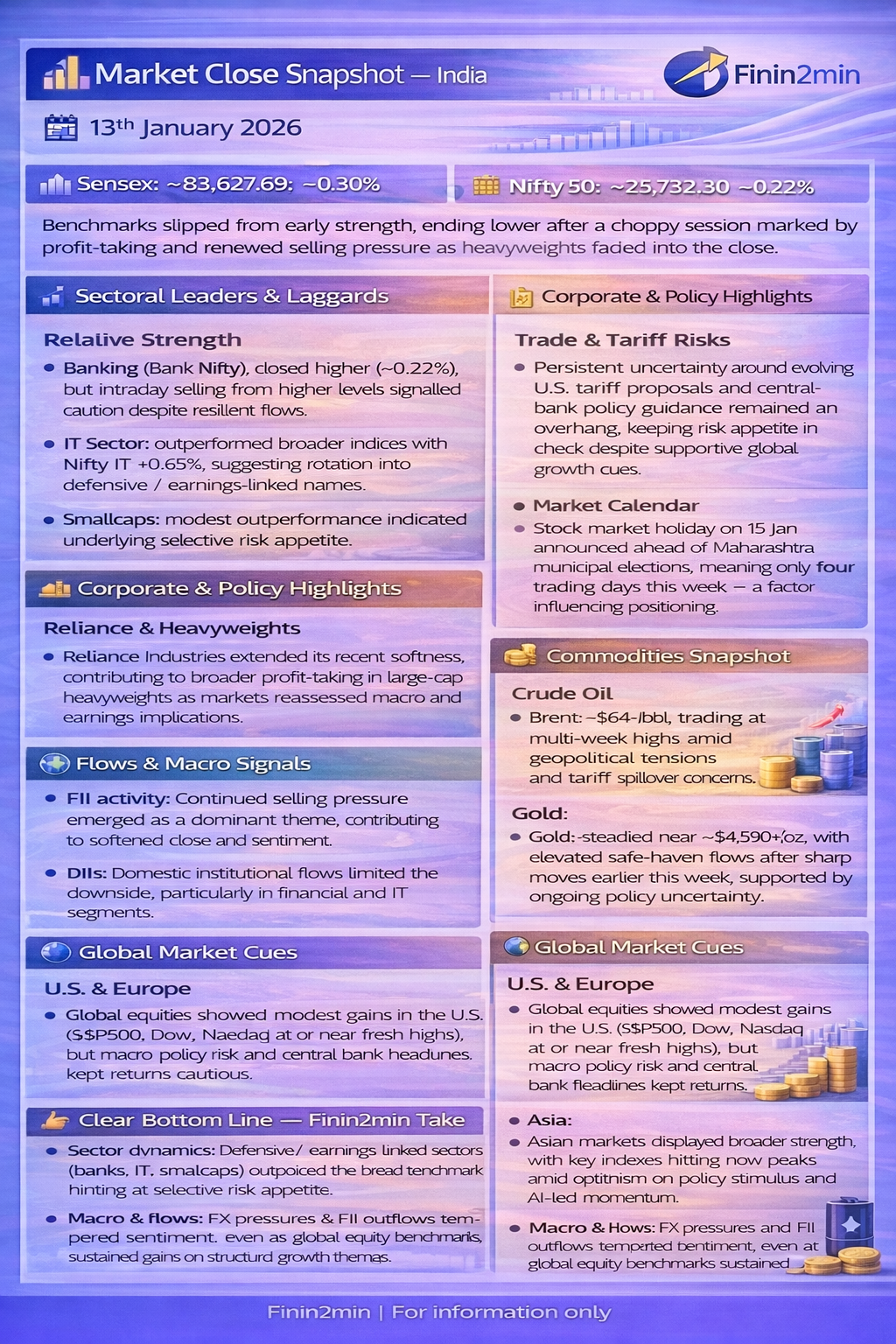

- Sensex: ~83,627.69, –0.30%

- Nifty 50: ~25,732.30, –0.22%

Benchmarks slipped from early strength, ending lower after a choppy session marked by profit-taking and renewed selling pressure as heavyweights faded into the close.

📈 Sectoral Leaders & Laggards

Relative Strength

- Banking (Bank Nifty): closed higher (~+0.22%), but intraday selling from higher levels signalled caution despite resilient flows.

- IT Sector: outperformed broader indices with Nifty IT +0.65%, suggesting rotation into defensive / earnings-linked names.

- Smallcaps: modest outperformance indicated underlying selective risk appetite.

Underperformance

- Heavyweights / large caps: continued profit booking weighed on overall index momentum.

🏢 Corporate & Policy Highlights

Reliance & Heavyweights

- Reliance Industries extended its recent softness, contributing to broader profit‑taking in large‑cap heavyweights as markets reassessed macro and earnings implications.

Trade & Tariff Risks

- Persistent uncertainty around evolving U.S. tariff proposals and central‑bank policy guidance remained an overhang, keeping risk appetite in check despite supportive global growth cues.

Market Calendar

- Stock market holiday on 15 Jan announced ahead of Maharashtra municipal elections, meaning only four trading days this week — a factor influencing positioning.

💱 Flows & Macro Signals

- FII activity: Continued selling pressure emerged as a dominant theme, contributing to the softened close and sentiment.

- DIIs: Domestic institutional flows limited the downside, particularly in financial and IT segments.

FX

- INR drifted weaker intraday (near ~90+ vs USD), echoing broader EM currency pressures and risk aversion.

🪙 Commodities Snapshot

Crude Oil

- Brent: ~$64+/bbl, trading at multi-week highs amid geopolitical tensions and tariff spillover concerns.

Gold

- Gold: steadied near ~$4,590+/oz, with elevated safe-haven flows after sharp moves earlier this week, supported by ongoing policy uncertainty.

Base Metals

- Copper and industrial metals saw mixed action — softer on commodity supply fundamentals but supported by risk hedging flows.

🌍 Global Market Cues

U.S. & Europe

- Global equities showed modest gains in the U.S. (S&P500, Dow, Nasdaq at or near fresh highs), but macro policy risk and central bank headlines kept returns cautious.

Asia

- Asian markets displayed broader strength, with key indexes hitting new peaks amid optimism on policy stimulus and AI-led momentum.

Macro Risks

- Policy ambiguity — especially surrounding central bank independence and tariffs — continued to fuel volatility expectations across rates, FX and commodity markets.

📌 Clear Bottom Line — Finin2min Take

Domestic markets closed lower today, reflecting renewed profit booking in heavyweight stocks, persistent FII selling, and risk aversion tied to trade and tariff uncertainty.

- Sector dynamics: Defensive / earnings-linked sectors (banks, IT, smallcaps) outpaced the broad benchmark — hinting at selective risk appetite.

- Commodities: Oil remained elevated on geopolitical risk; gold steadied amid safe-haven flows.

- Macro & flows: FX pressures and FII outflows tempered sentiment, even as global equity benchmarks sustained gains on structural growth themes.

👉 Near-term outlook: A volatile mix of tariff policy noise, earnings catalysts, and macro data will likely define trading ranges. Being overweight select value and defensive sectors, while managing cyclical exposure carefully, continues to align with current market dynamics.

Market data and developments are based on live updates, news coverage, and financial sources as of the end of today’s session. Finin2min content is for market insight and discussion only. Not investment advice.